From our partners at SmallCaps Daily

As Gold and Silver Rally into an Enforcement Era, SMX Is Quietly Building the Backbone of Material Verification

Gold’s record surge above $5,500 and silver’s continued strength reflect more than macro uncertainty — they highlight a growing problem across global supply chains: trust no longer scales.

Precious metals operate under increasing ESG mandates, regulatory oversight, and geopolitical scrutiny, exposing the limits of documentation-based systems. Markets are shifting from “trust me” to “prove it,” and that shift is reshaping how value is assigned.

Unlike most companies reacting to rising scrutiny, SMX was built specifically for materials like gold and silver, where provenance, custody, and verification are non-negotiable.

SMX (NASDAQ: SMX) was built for exactly this environment. Its molecular identity technology embeds proof directly into the material itself, creating a tamper-resistant digital twin that travels with gold, silver, and other materials throughout their lifecycle.

Proven at national scale and designed for regulated conditions, SMX is expanding horizontally across industries — positioning verification not as a cost of compliance, but as durable infrastructure markets are beginning to require.

Further Reading from MarketBeat

3 Low P/E Stocks: Separating Multibaggers From a Value Trap

Written by Thomas Hughes. Publication Date: 1/16/2026.

Summary

- Low P/E stocks offer value, limited downside, and potential for outsized gains if fundamentals improve, but they can also signal deeper problems.

- Comcast and HP Inc. stand out with high yields, oversold conditions, and analyst support pointing to meaningful upside in 2026.

- Rogers Communications trades at a discount but lacks near-term growth catalysts, with inconsistent dividend payments and muted institutional interest.

P/E — the price-to-earnings multiple — measures a stock’s value relative to its earnings and is a cornerstone of value investing. Stocks with lower P/E ratios are cheaper relative to earnings, can indicate value for investors, and have the potential for significant gains over time.

Low P/E stocks often have much of their bad news already priced in, offer limited downside versus higher-valued names, provide higher-than-average yields, and occasionally produce multibagger returns. The combination of improving fundamentals and earnings growth creates a powerful tailwind that can amplify price action as stocks are revalued and premiums expand. The risk, of course, is that some stocks are cheap for a reason—if fundamentals don’t recover, there may be little hope for price gains. Below are five low P/E stocks and whether they look like opportunities for 2026.

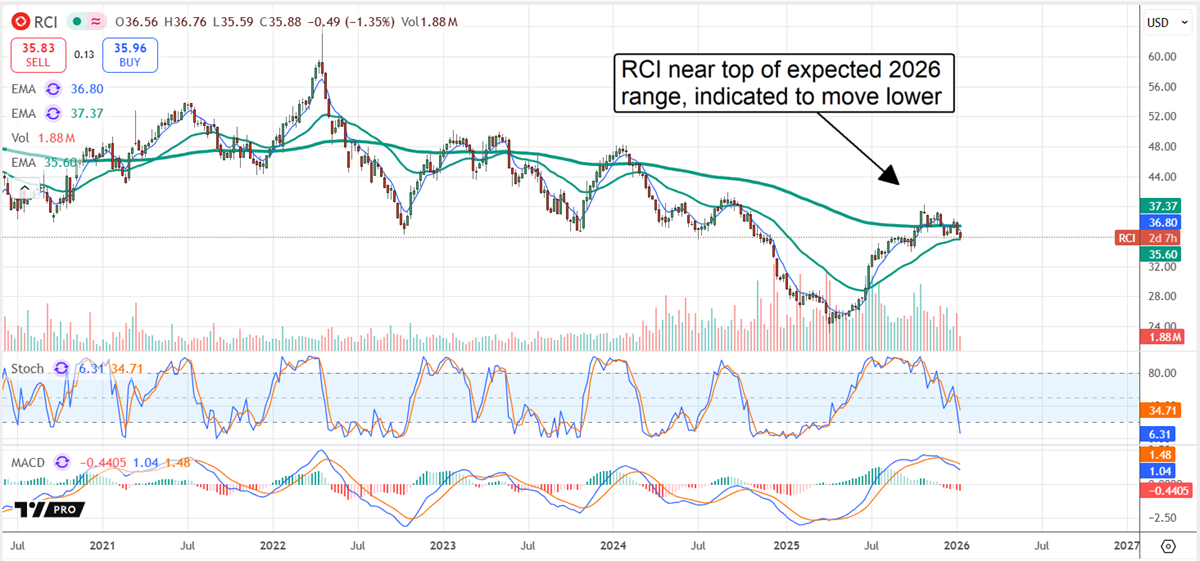

Why Rogers’ High Yield Comes With Limited Upside

End of America update (Ad)

There are five truths reshaping America’s financial future — and ignoring them could be costly. From an overextended government and vanishing savings to AI-driven job displacement and a widening wealth divide, the warning signs are clear. But according to Porter Stansberry, these same forces are also driving one of the largest wealth transfers in history. His new exposé, The Final Displacement, reveals the economic blueprint behind these shifts — and the final step he believes every American must take to protect and grow their wealth before it’s too late.Click here to watch The Final Displacement for free

Rogers Communications (NYSE: RCI) is a Canadian communications and media company trading at about 10x current-year earnings, which—if re-rated to broader market multiples—could imply roughly 100% upside. The problem is the outlook: the company, whose dividend yields more than 4% as of early 2026, trades in line with media peers and faces a tepid near-term outlook. Both earnings growth and dividend growth are questionable; the payout record has been uneven, with irregular distributions and recent declines.

Analyst and institutional signals offer little reason to expect a strong rebound in 2026. Analysts rate it a Hold but have sharply reduced price targets over the past year, leaving the stock trading below consensus fair value. Consensus valuations as of mid-January point to potential downside. Institutional ownership is modest—about 45%—and institutions were net sellers at the start of the year.

Comcast Combines High Yield With Rebound Potential in 2026

Comcast Corporation (NASDAQ: CMCSA) is another communications and media company trading at a low P/E. It trades at roughly 7x current-year earnings and yields about 4.5%. While revenue and earnings will decline because of divestitures, Comcast’s core operations are expected to grow and market expectations are modest—conditions that can set the stock up to outperform and trigger a bullish analyst revision cycle. Analysts are already relatively optimistic on the name.

An analyst reset depressed CMCSA in 2025, but two factors support a rebound in 2026. First, the stock became oversold and recent targets line up with the consensus forecastfor roughly 20% upside. Second, institutional activity is favorable: institutions own more than 65% of the stock and were net buyers early in the year, purchasing about $3 for every $1 sold in the first two weeks of January.

HP Inc. Looks Positioned for a Powerful Rebound in 2026

HP Inc.’s (NYSE: HPQ) share price is influenced by AI-related dynamics and by DRAM supply constraints that have limited production. Those factors prompted analysts to reset price targets, but like Comcast, HPQ appears oversold and may be setting up for a rebound. The company is expected to deliver modest growth over the next few years and generate enough earnings to support capital returns. Its dividend yielded more than 5.5% annualized as of early January, and management is expected to grow distributions: HPQ pays under 40% of earnings, has increased its dividend for 15 consecutive years and has roughly a 10% compound annual growth rate in dividends.

Analysts are optimistic. A consensus reset lowered expectations in 2025, but late-2025 and early-2026 updates have reaffirmed the outlook. Consensus implies at least ~20% upside, and reaching that level could trigger an additional 20%–30% move. Technically, HPQ sits near long-term lows while the MACD is diverging from price—an indicator that the downtrend may be weakening and bulls could be poised to regain control.

This message is a sponsored message sent on behalf of SmallCaps Daily, a third-party advertiser of MarketBeat. Why was I sent this email content?.

This message is a paid advertisement for SMX (NASDAQ: SMX) from SmallCaps Daily and Interactive Offers. MarketBeat Media, LLC receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $25,500. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either SmallCaps Daily or Interactive Offers. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding SMX (NASDAQ: SMX) on Interactive Offers’ website for additional information about the relationship between Interactive Offers and SMX (NASDAQ: SMX).

If you have questions or concerns about your account, please don’t hesitate to email our South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2026 MarketBeat Media, LLC.

345 N Reid Place #620, Sioux Falls, South Dakota 57103-7078. USA..

Today’s Featured Link: Punch these codes into your ordinary brokerage account (From Brownstone Research)