I’ve traded for over 30+ years… 200k+ follow me online to see how I trade… plus, regularly on CNBC and Fox Business…

This market is almost impossible to swing trade or trade options in.

Day trading is the only strategy to be in at the moment if you plan to stay afloat until the next leg up (or down).

Right now, my open positions is at a multi-year low… normally I have 25+ positions open. Not right now.

Keep your sizing small…

I’ll know… and you will too know when to size up when my #1 indicator shows it.

I’ve used this indicator for decades, including calling the crash of 2008 live on CNBC.

Grab the free gift from me sharing my top indicator… plus, it’ll get you access to my weekly watchlists as we navigate this choppy market.

Add this indicator to know when you can size up your positions,

Scott Redler

Co-Founder of T3 Live & Editor of Power Plays

Disclosures

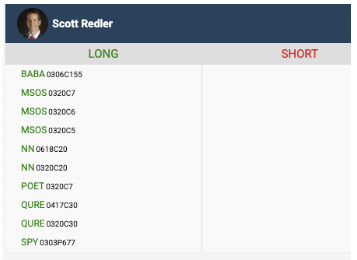

Scott Redler Positions Disclosure as of 2026-03-03 at 10.14.38 AM

Wednesday’s Featured Content

Amprius Stock Price Gets Amped by Hyper Growth Outlook

Written by Thomas Hughes. Published: 3/5/2026.

Key Points

- Amprius Technologies is on track for hypergrowth and outperformance in 2026 as manufacturing and demand trends collide.

- Ramping production and full-NDAA compliance unlock the door to accelerating government demand.

- AMPX batteries can disrupt the battery market, offering superior performance and energy density, enabling larger payloads and longer ranges.

- Special Report: [Sponsorship-Ad-6-Format3]

It has taken time, but Amprius Technologies’ (NYSE: AMPX) strategy execution is starting to pay off, amplifying its hypergrowth outlook. Among the key takeaways from its Q4 2025 earnings report was better-than-expected guidance pointing to another year of solid gains.

Management expects revenue growth to slow, but still remain above a 70% year-over-year pace; the guidance also appears conservative.

Skip Headlines Straight to Original Research (Ad)

Our investment research analysts are going to be releasing their next investment idea tomorrow morning, around 10:00 AM Eastern time.Add yourself to the distribution list here.

Follow-on contracts, new customers, improved execution, an expanding manufacturing footprint, and full compliance with the National Defense Authorization Act (NDAA) position the company well.

Other details included a one-time charge related to the discontinued lease of a Colorado facility. Originally intended to serve as Amprius’ manufacturing base, the company has since shifted to a contract manufacturing model for its advancedbatteries, relying on third-party manufacturers.

The one-time charge clarifies the company’s obligations and improves cash-flow visibility as it strengthens its outsourced manufacturing base. Three South Korean battery manufacturers and one U.S.-based manufacturer were recently added to the network, putting the company on track for full NDAA compliance and accelerating government business this year.

Amprius Accelerates its Profitability Outlook in 2026

Amprius Technologies reported an electrifying quarter: revenue rose more than 137% year-over-year (YOY), beating consensus by over 1,000 basis points (bps). Growth was driven by new and existing customers and strong execution, with client and contract wins pointing to continued momentum in 2026.

Another catalyst was margin improvement. Gross margin widened by 4,500 bps to 24% (positive), driving a 365% YOY increase in gross profit (also positive) and the company’s first quarter of positive adjusted EBITDA.

The company is still burning cash, but losses contracted sharply and are expected to improve in coming quarters. Analysts currently forecast an inflection to adjusted profits in Q1 2027, though it could occur by the end of 2026; management is guiding toward positive adjusted EBITDA.

Analysts Point to 60% Upside Potential and Long-Term Highs

Analysts have been slow to update estimates after Amprius’ Q4 results, but the bullish trends leading into the report are likely to strengthen in its wake.

Data show coverage increasing to nine analysts on a trailing-twelve-month (TTM) basis, sentiment firming to Moderate Buy with an 88% buy-side bias, and price targets rising.

The consensus price target implies more than 30% upside from the pre-release closing price, while the high-end range — set by Northland Securities last year and reaffirmed by Needham in January — suggests an additional ~25% upside is possible.

Institutional ownership offers another catalyst. Institutional interest remains light at roughly 5% as of early March, but the trend is strengthening. Institutional buying spiked in Q4 2025 and remained strong in Q1 2026, providing a tailwind for the stock.

This increase in ownership is noteworthy given the spike in short interest in late 2025 and early 2026, which set the market up for potential short-covering rallies or a short squeeze.

No Red Flags in AMPX’s Balance Sheet: Green Flags in Its Price Action

Amprius’ balance sheet shows no red flags. The company is well-capitalized, reports net cash relative to total liabilities, and increased shareholders’ equity in 2025. Equity grew by nearly 50%, leaving leverage at ultra-low levels and positioning the company to continue executing its strategy.

Looking ahead, the cash balance may decline in coming quarters, but additional capital raises appear unlikely at this point. Without the need to build its own manufacturing capacity, management can focus on development, marketing, and sales — another factor suggesting potential outperformance in the year ahead.

The stock’s price action also shows positive signals. Monthly, weekly, and daily charts converged with bullish indicators following the release. While periodic pullbacks are possible, those dips may present buying opportunities.

Long term, the stock may sustain upward momentum for many quarters — potentially several years — with technical projections suggesting a baseline target of $30.

This Month’s Bonus Content

Qualcomm’s Robotics Push Could Be Bigger Than the Market Thinks

Authored by Sam Quirke. First Published: 3/5/2026.

Key Points

- Qualcomm’s CEO flagged robotics as a major growth opportunity, projecting the segment will “start to get scale within the next two years.”

- Analysts at Wells Fargo and Loop Capital recently upgraded the stock and raised price targets to $185, citing easing pressures and emerging growth drivers.

- The chipmaker’s push into automotive, IoT, and edge AI is starting to show traction—robotics could become the next pillar of its diversification strategy.

- Special Report: [Sponsorship-Ad-6-Format3]

Shares of Qualcomm Inc. (NASDAQ: QCOM) were trading just below $140 early in the week, down approximately 25% from their January high. While they had been under pressure since before Christmas, much of the recent decline followed weak forward guidance in the company’s latest earnings report.

The tech giant has posted modest gains since its early-February low, but the move looks more like consolidation than the start of a major comeback. For many investors, Qualcomm still carries the perception of being overly dependent on smartphones at a time when the broader semiconductor industry is being defined by data-center artificial intelligence demand.

Elon Musk already made me a “wealthy man” (Ad)

I Met Elon Musk “Face-to-Face”

During a private gathering of Wall Street elites, I was one of two people selected to speak with Elon personally.

As a result, my research now leads me to believe Elon will announce the SpaceX IPO on this date:

March 26, 2026. Circle it on your calendar.

I’m sharing an “access code” that lets anyone grab a pre-IPO stake before it happens. This is your invitation to the biggest wealth-building event of the decade.Click Here to See how to Get Your “SpaceX Access Code”

Yet a new narrative may be quietly forming that challenges that assumption.

Qualcomm’s New Growth Story Beyond Smartphones

In comments earlier this week, Qualcomm’s CEO Cristiano Amon pointed to robotics as a major opportunity for the company’s next phase of growth. Speaking about the evolution of AI-enabled devices, Amon said he expects robotics to “start to get scale within the next two years.”

That remark may not seem revolutionary on its own, but it fits into a broader shift in Qualcomm’s strategy. The company has spent the past several years diversifying beyond smartphones, building new revenue streams in automotive chips, Internet of Things (IoT) devices, and edge AI computing. Robotics could become the next extension of that push.

Qualcomm has already introduced specialized processors designed for robotics systems, applying the same architecture principles that made its Snapdragon chips dominant in mobile devices. The idea is simple: robots, industrial machines, and autonomous systems require the low-power, high-performance computing Qualcomm provides. If robotics adoption accelerates over the next decade, that positioning could prove extremely valuable.

Why the Market Has Been Skeptical on QCOM

Despite the long-term opportunity, the market has remained cautious on Qualcomm—and for good reason. The company’s fortunes have historically been tied closely to smartphone demand, and the global handset market has struggled to regain momentum in recent years.

Weak guidance last month did Qualcomm no favors, reinforcing the perception that the company remains vulnerable to cyclical slowdowns in mobile devices. That narrative has weighed heavily on the stock, especially as investors pour capital into companies seen as clearer beneficiaries of the generative AI boom. The result has been persistent underperformance relative to many of its tech and semiconductor peers.

Analysts Are Starting to Shift Tone

The overall analyst consensus on Qualcomm remains a Hold, but recent commentary has become slightly more constructive. Wells Fargo lifted its rating from Underweight to Equal Weight last week, and Loop Capital went one step further by re-rating the stock to Buy. Both groups also raised their price targets to $185, implying more than 30% upside from current levels.

The view is that several of the pressures that weighed on Qualcomm in recent quarters are beginning to ease just as new growth opportunities are emerging. The company’s expanding data-center ambitions and its potential role in the AI inference market are additional reasons some analysts are more bullish heading into the rest of the year.

Those shifts may seem modest, but they matter because Qualcomm has spent much of the past year fighting a narrative that it’s been left behind in the AI race. If robotics, alongside automotive chips and edge AI platforms, begin contributing meaningfully to revenue growth, that narrative could change quickly.

A Diversification Strategy Taking Shape

Part of the reason analysts are becoming more constructive is that Qualcomm’s diversification strategy is starting to show tangible progress. The company expects its reliance on Apple Inc. (NASDAQ: AAPL) to decline over time while its other segments expand steadily.

At the same time, Qualcomm has been investing heavily in AI-related technologies, including acquisitions aimed at strengthening its presence in data centers and high-performance computing.

These initiatives point to a common objective: reducing Qualcomm’s dependence on smartphones and building a broader semiconductor platform story. Robotics, if Amon’s timeline proves accurate, could become the next pillar of that strategy.

Qualcomm Robotics Traction Could Shift Investor Sentiment

If Qualcomm begins demonstrating real traction in robotics over the coming quarters, investors may reassess the company’s long-term growth profile. For now, the stock’s behavior suggests the market is still waiting for proof. Qualcomm’s shares have stabilized since early February but have yet to mount a decisive recovery. That cautious price action reflects the tension between a weak near-term outlook and what could be a compelling long-term opportunity.

Investors should watch for the stock to consolidate around the $140 level or higher as confirmation that bulls are regaining control. A steady run of higher lows in the weeks ahead would go a long way toward confirming that the market is willing to back Qualcomm’s evolving growth story.

Thank you for subscribing to Earnings360, a morning newsletter that summarizes quarterly earnings for public companies that trade on U.S. markets.

This email communication is a paid advertisement for T3 Live, a third-party advertiser of Earnings360 and MarketBeat.

If you need assistance with your account, please feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

© 2006-2026 MarketBeat Media, LLC. All rights protected.

345 N Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. USA..

Featured Link: An AI just scored 357 stocks. Here’s what it found. (Click to Opt-In)