Good day,

Our research team is preparing to release our next stock idea tomorrow morning, just before 12:00 PM Eastern.

As a reminder, we send this pick first to investors who subscribe to receive The Early Bird Stock of the Day via text message. Then, it goes out the following morning to our email newsletter subscribers.

If you’d like to see the idea before it reaches the broader audience, now is the time to join. Many subscribers told us they appreciated getting early access, and our most recent pick drew a strong response.

The Early Bird Stock of the Day is a free service from The Early Bird and MarketBeat. To add yourself to the SMS distribution list and make sure you’re included in tomorrow’s release, simply click the link below:

Get The Early Bird Stock of the Day

Best regards,

The Early Bird Team

Today’s Exclusive Article

3 Stocks With the Most to Gain From Tariff Relief

By Dan Schmidt. Article Published: 3/2/2026.

Key Points

- The Supreme Court struck down President Trump’s sprawling tariff regime under the IEEPA.

- While other tariffs remain and Trump quickly enacted new ones, the decision provides significant relief and newfound policy predictability for many U.S. firms.

- Five Below, Ross Stores, and FedEx Corp are three of the companies that stand to benefit most from tariff reductions (and potential refunds).

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Tariff drama is again dominating market headlines after the Supreme Court struck down the strictest rates. While the news is broadly bullish for many retailers, the muted market reaction may have left investors puzzled. Here’s why the market responded the way it did, and why the ruling still creates opportunities for several stocks that are no longer in the trade-war crosshairs.

Where the Tariff Situation Currently Stands

On Feb. 20, the Supreme Court ruled againstPresident Trump’s use of the International Emergency Economic Powers Act (IEEPA) to impose sweeping tariffs without Congressional consent. In a 6-3 decision, the Court found that the President exceeded his authority under IEEPA and ordered that all tariffs imposed under that law be vacated immediately.

The rise of the “Useless Class” (Ad)

Famed historian Yuval Noah Harari recently issued a warning that should send a shiver down the spine of every American. He predicts the emergence of a massive new useless class. These aren’t just people who are temporarily unemployed. These are people who have become economically irrelevant. As Luke Lango and I just exposed in our recent interview, we have reached the singularity. For the first time in 250 years, intelligence has been decoupled from labor. During America’s first 1776 moment, the steam engine replaced muscle. In this new 1776 moment, AI is replacing the human mind.

This is why you see the Magnificent 7 tech giants adding trillions in value while the real economy feels like it’s in a death spiral. The divide is widening. On one side: the useless class who cling to old-world skills. On the other: the new aristocracy who own the assets of the technological republic. Luke and I have identified the three specific money moves our research indicates you must make to ensure you stay on the winning side of this divide.See the three moves to stay on the winning side of AI

Following the ruling, the administration enacted new 10% tariffs under Section 122 and said the existing tariffs under Section 232 would remain in place. According to a Penn Wharton analysis, the new effective tariff rate is 9.1%, down from the roughly 9.8% rate that applied for much of 2025. Companies facing tariffs will welcome relief, but that relatively small decline helps explain why markets barely reacted.

The Section 122 tariffs have important limitationsthat the IEEPA ones did not. Section 122 tariffs cannot be targeted to specific countries, the rate cannot exceed 15%, and they do not stack on top of other tariffs (such as Section 232). Most importantly, they are temporary: after 150 days the President must request an extension from Congress, which is unlikely to be approved with midterm elections only weeks after the expiration.

Another wild card is the prospect of refunds. IEEPA tariffs collected an estimated $175 billion, and companies seeking refunds must file suit in the Court of International Trade. Refunds would be a windfall for many firms that had baked higher import costs into their 2026 plans. Refunds, combined with further rate reductions after the 150-day window under Section 122, would represent a double tailwind for the stocks that faced the most tariff pressure.

3 Stocks That Benefit From Tariff Cancellations (and Potential Refunds)

The market’s recovery in the final eight months of 2025 likely reflected expectations that the Supreme Court would limit the administration’s tariff authority. Regardless, tariffs materially affected the following three companies, and any rollback of those measures — along with possible refunds — could have meaningful implications.

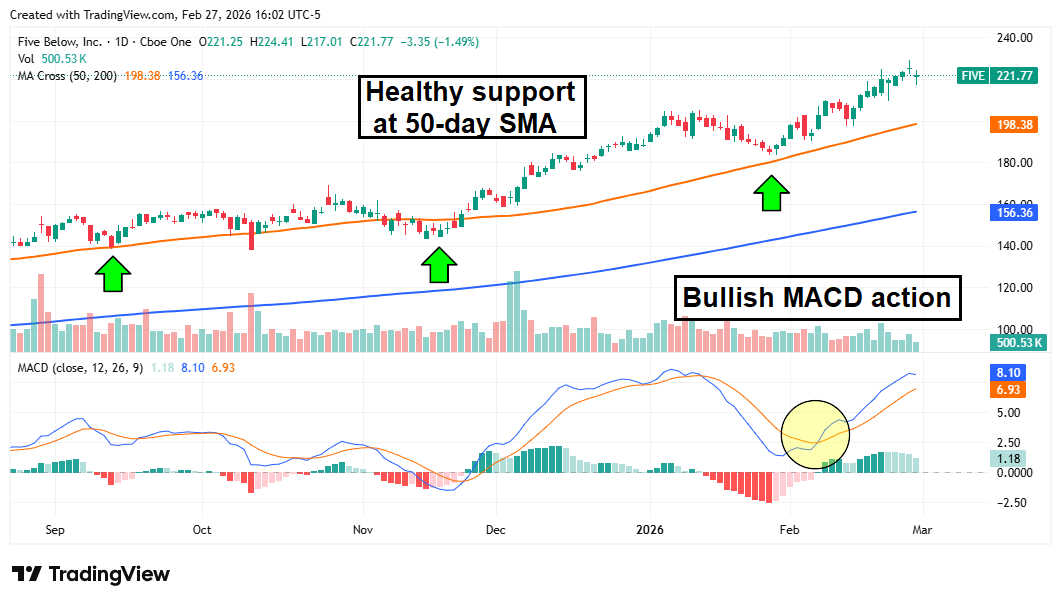

Five Below: Immediate Relief on China Imports

Five Below Inc. (NASDAQ: FIVE) faced serious margin pressure from tariffs because most of its products are imported from China and its low-price strategy prevents it from passing costs on to customers.

The chain targets young, highly price-sensitive shoppers, so every tariff increase directly hit Five Below’s margins. Revoking the harshest rates on China therefore provides immediate relief.

Equally important, the Supreme Court’s decision restores some predictability and reduces the threat of escalating duties, such as last spring’s Liberation Day tariffs.

Five Below reported fiscal Q3 2026 results in December that were strong, but management warned of a potential 240-basis-point decline in operating margin due to tariff costs. The company will release fiscal Q4 results on March 18; while the tariff relief is unlikely to affect those numbers, fiscal 2027 projections should look better than they did last quarter. Reflecting that view, JPMorgan raised its price target to a Street-high $259 — roughly 15% above current levels.

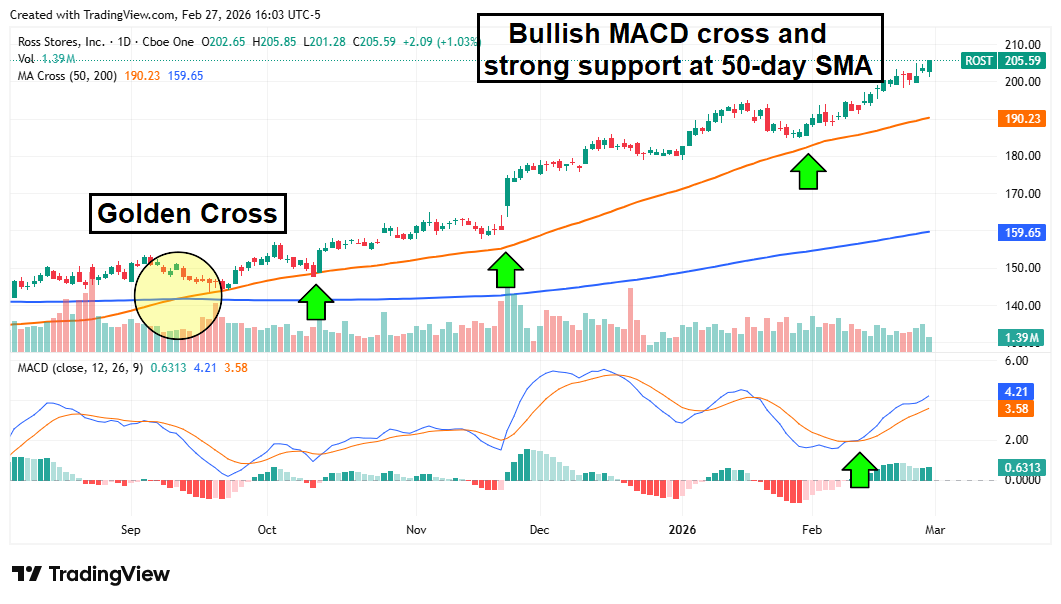

Ross Stores: Margin and Inventory Benefits

Ross Stores Inc. (NASDAQ: ROST) also benefits from the tariff decision, though more indirectly than Five Below. While over half of Ross’s merchandise originates in China, Ross itself does little direct importing; it buys overstocks from other U.S. brands that have already paid duties.

Many retailers front-loaded inventory last year to avoid tariff exposure and may now be willing to offload that inventory to resellers like Ross at deeper discounts. Ross has said tariffs reduced earnings by about 16 cents per share in fiscal 2025.

Investors will watch Ross’s March 3 earnings report for updated guidance now that the IEEPA tariffs have been struck down. Analysts were optimistic heading into the report: five firms raised price targets in February, including a Street-high $232 from JPMorgan on Feb. 23.

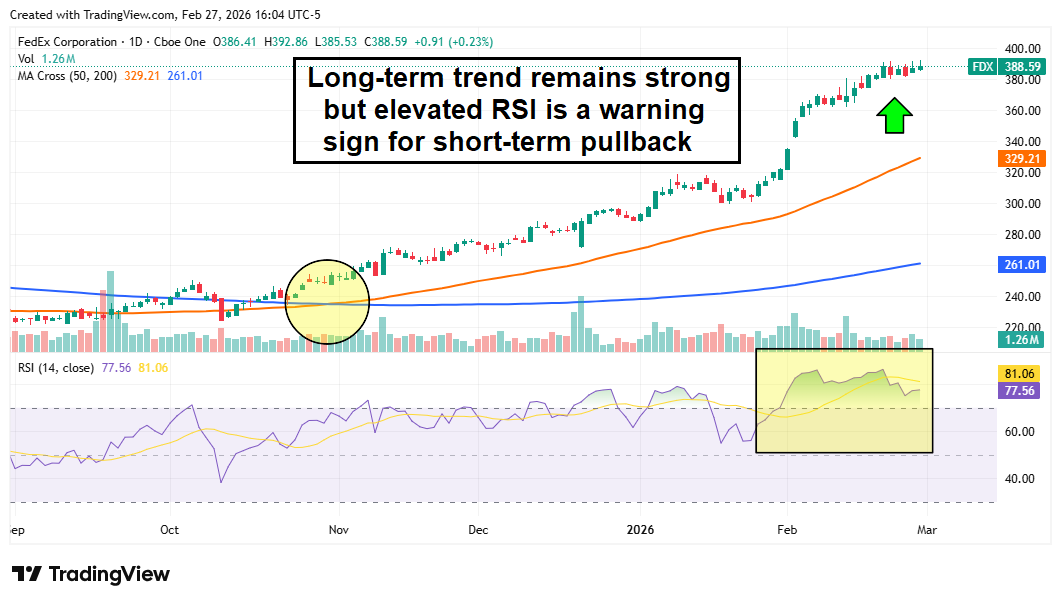

FedEx: Trade-Volume Recovery and First-Mover Advantage on Refunds

FedEx Corp. (NYSE: FDX) will not get the same margin relief that retailers might, but it stands to gain in other ways.

The biggest benefit is a likely normalization of operations on the lucrative China-to-U.S. route. FedEx executives estimated tariffs caused about a $1 billion revenue headwind during the 2025 fiscal year — a shortfall that should be easier to manage now that IEEPA tariffs are gone.

FedEx was also the first company to sue the U.S. government for a refund after the Supreme Court decision. If successful, the firm could be eligible for up to $1 billion in tariff relief and could earn goodwill by returning some of that windfall to shippers. One caution: FDX appears overbought on the Relative Strength Index (RSI), so a pullback to the 50-day moving average might offer a more stable entry point for new positions.

Special Report

The Real Reason Eli Lilly Is Pouring $3 Billion Into China

Reported by Jeffrey Neal Johnson. Article Posted: 3/13/2026.

Key Points

- Eli Lilly is committing $3 billion over a decade to expand manufacturing in China, targeting a GLP-1 market that some analysts estimate could reach $14 billion by 2030.

- The investment is designed to close a manufacturing gap with Novo Nordisk while building cost advantages against more than 60 domestic Chinese competitors developing rival GLP-1 drugs.

- Local production also hedges against supply chain risks tied to trade friction, a vulnerability that recent global GLP-1 shortages have already exposed.

- Special Report: Elon Musk: This Could Turn $100 into $100,000

Eli Lilly and Company (NYSE: LLY) is a titan of the pharmaceutical industry, a position reinforced by the monumental success of its GLP-1 diabetes and obesity drug franchise. With products like Mounjaro and Zepbound transforming patient care and generating blockbuster sales, Lilly’s stock has climbed into the top ranks of the S&P 500.

In a move that signals long-term ambition, Lilly has announced a $3 billion, decade-long commitment to expand manufacturing operations in China. That decision prompts a key question for shareholders: in a complex global landscape, why make such a substantial bet on China now? The answer reflects strategic foresight and outlines a clear blueprint for Lilly’s future growth.

Why China? An Unprecedented Market Opportunity

The rise of the “Useless Class” (Ad)

Famed historian Yuval Noah Harari recently issued a warning that should send a shiver down the spine of every American. He predicts the emergence of a massive new useless class. These aren’t just people who are temporarily unemployed. These are people who have become economically irrelevant. As Luke Lango and I just exposed in our recent interview, we have reached the singularity. For the first time in 250 years, intelligence has been decoupled from labor. During America’s first 1776 moment, the steam engine replaced muscle. In this new 1776 moment, AI is replacing the human mind.

This is why you see the Magnificent 7 tech giants adding trillions in value while the real economy feels like it’s in a death spiral. The divide is widening. On one side: the useless class who cling to old-world skills. On the other: the new aristocracy who own the assets of the technological republic. Luke and I have identified the three specific money moves our research indicates you must make to ensure you stay on the winning side of this divide.See the three moves to stay on the winning side of AI

To understand Lilly’s strategy, investors must first appreciate the scale of the opportunity. This investment responds to a market too large to ignore. China faces a significant public health challenge, with an estimated 141 million people living with diabetes. The country also has more than 600 million adults who are classified as overweight or obese—the largest such population in the world. As the middle class expands and healthcare spending rises, demand for effective treatments is expected to increase substantially.

That creates a vast and largely untapped pool of potential patients for Lilly’s leading medications. The financial upside is immediate and significant: market forecasts project China’s GLP-1 market to surge, with some analysts estimating it could reach roughly $14 billion by 2030. This rapid expansion makes China a critical long-term growth engine for Lilly’s injectable products and for its next wave of innovation, including the oral candidate orforglipron. For a daily oral medication to succeed at scale, efficient, high-volume local manufacturing is not just advantageous—it is essential. Securing this market is vital to maintaining global leadership.

Lilly’s Great Wall: A Strategy for Supply and Supremacy

Lilly’s investment serves a dual strategic purpose: it builds a defensive shield against external risks while creating an offensive capability to secure market dominance. This proactive approach should reassure investors about management’s ability to navigate a complex global environment and protect future earnings.

The Geopolitical Shield

First, the move acts as a defensive shield by strengthening the supply chain. The U.S. pharmaceutical industry remains heavily dependent on China for Active Pharmaceutical Ingredients (APIs), the core components of many drugs. In an era of trade friction and potential export controls, that dependence is a vulnerability. By establishing a robust presence in China, Lilly reduces the risk of supply interruptions, mitigates exposure to trade disputes or logistics disruptions, and helps ensure a stable supply of medicines to Chinese patients—while supporting more predictable revenue streams for shareholders.

The Competitive Weapon

Second, the investment is an offensive tool in a fiercely competitive market. Lilly faces a two-front challenge in China. Its main global rival, Novo Nordisk (NYSE: NVO), already has an established manufacturing footprint in the country. Lilly’s investment is necessary to level the playing field and compete on supply, speed, and scale.

Equally important is the rise of local competitors: over 60 domestic Chinese pharmaceutical companies are developing their own GLP-1 therapies. That will exert downward pressure on prices in the years ahead. By manufacturing locally and partnering with domestic experts like Pharmaron, Lilly can achieve greater cost efficiencies and pricing flexibility—allowing it to defend market share against lower-cost alternatives, preserve long-term margins, and build a durable competitive moat.

Why This Move Secures Future Returns

Ultimately, this multi-billion-dollar strategy reinforces the bullish investment case for Eli Lilly. It is about more than expanding sales; it is about building a durable, defensible, and highly profitable business over the long term. Capturing a meaningful share of China’s GLP-1 market could translate into billions of dollars in annual revenue, providing a long runway for growth that supports Lilly’s premium valuation.

This kind of forward-looking capital deployment helps explain why Wall Street sentiment remains largely positive. The analyst consensus for Lilly’s stock is a Moderate Buy, with an average price target near $1,230. That optimism reflects the current success of Mounjaro and Zepbound and the expectation that management will continue to take strategic actions to secure future growth. The China investment is a tangible validation of that confidence.

By establishing a powerful third pillar of global growth alongside the U.S. and Europe, Lilly is not merely expanding—it’s diversifying and strengthening its enterprise. For investors, this $3 billion commitment is less a gamble than a calculated foundation for the company’s next decade of growth, further solidifying Eli Lilly’s position as a global pharmaceutical leader and making a compelling case for its long-term value.

Thank you for subscribing to MarketBeat!

We empower everyday investors to make better investment decisions by offering up-to-the-minute financial information and objective market research.

This email content is a sponsored email for The Early Bird, a third-party advertiser of MarketBeat. Why did I get this message?.

If you need assistance with your newsletter, please don’t hesitate to email MarketBeat’s U.S. based support team at contact@marketbeat.com.

If you would like to unsubscribe or change which emails you receive, you can manage your mailing preferences or unsubscribe from these emails.

© 2006-2026 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, South Dakota 57103. United States..

Just For You: ALERT: Drop these 5 stocks before the market opens tomorrow! (From Weiss Ratings)