April 05, 2026

MARKET TELL – WEEKLY INTELLIGENCE

Powered by the TQ Intelligence System

Institutional tools, refinement, and analysis for traders who refuse to stay reactive.

Transcripts, filings, insider clusters, and options flow, distilled into a single weekly signal map. This is what it looks like to treat your portfolio like a responsibility, not a hobby.

Welcome to Market Tell.

This letter maps institutional capital behavior, CEO sentiment, and options market positioning into a single weekly signal framework, the kind of information that usually requires multiple paid tools and hours of synthesis to assemble. No recommendations. No predictions. Just the data, distilled.

Read in sequence. Leadership intent sets context. Capital behavior confirms conviction. Options markets reveal where expectations are concentrating. The Alpha Engine narrows focus. The Weekly Signal aligns your posture for the week ahead.

S&P LEADERSHIP SIGNALS

Q4 2025 EARNINGS SEASON RECAP

The clearest throughline across the completed season was transition. Management teams that spent recent periods in heavy investment cycles, particularly around AI infrastructure and digital transformation, began signaling that those cycles are converting into results. The language shifted from describing opportunity to reporting outcomes: improved efficiencies, new revenue streams, and measurable market share gains.

Capital allocation behavior reinforced the split. Companies with AI and infrastructure tailwinds accelerated spending, framing it as commitment against contracted, visible demand. Companies in stronger financial positions used the quarter to return capital through buybacks and dividends. Both behaviors reflect enough visibility to act decisively.

Demand signals were the most polarized element of the season. AI infrastructure, data center expansion, and power generation described conditions that leadership teams characterized as generational in scale. Residential construction, select consumer discretionary segments, and certain industrial niches described the opposite. The risks being cited differ in kind. Infrastructure companies described operational constraints where demand exceeds capacity to deliver. Consumer-facing companies described demand problems affecting whether delivery is needed at all.

PREMIER FEATURE

A Memecoin With Institutional Backing? Yes, Really.

For years, memecoins were ignored by serious investors.

Now one is breaking the rules—drawing attention from institutional wallets for reasons that go beyond hype.

Strong momentum. Real utility. Early positioning.

Still under the radar… for now.

Discover the #1 memecoin gaining serious traction.

© 2026 Boardwalk Flock LLC. All Rights Reserved. 2382 Camino Vida Roble, Suite I Carlsbad, CA 92011, United States. The advice and strategies contained herein may not be suitable for your situation. You should consult with a professional where appropriate. Readers acknowledge that the authors are not engaging in the rendering of legal, financial, medical, or professional advice. The reader agrees that under no circumstances Boardwalk Flock, LLC is responsible for any losses, direct or indirect, which are incurred as a result of the use of the information contained within this, including, but not limited to, errors, omissions, or inaccuracies. Results may not be typical and may vary from person to person. Making money trading digital currencies takes time and hard work. There are inherent risks involved with investing, including the loss of your investment. Past performance in the market is not indicative of future results. Any investment is at your own risk.

🟢 GREEN LIGHTS

Where Executive Confidence Is Accelerating

- ORCL (Oracle): Sustained bullish tone built on competitive wins in AI infrastructure and multicloud. Deferred revenue growth outpacing reported revenue provides forward visibility.

- ADI (Analog Devices): CEO framed fiscal 2026 as a potential “banner year,” grounded in backlog strength and AI-driven demand.

- AEP (American Electric Power):Contracted load pipeline doubled to 56 GW. Capital plan expanded to over $72 billion. Management beat 2025 guidance and reaffirmed premium long-term EPS growth.

- DTE (DTE Energy): A confirmed 1.4 GW data center contract with another large deal described as imminent. A 3 GW pipeline provides the visible foundation for 6 to 8 percent EPS growth guidance.

- GIS (General Mills): Management signaled the conclusion of its reinvestment phase and reaffirmed full-year fiscal 2026 guidance based on expected Q4 acceleration.

- WSM (Williams-Sonoma): Language shifted from returning to growth to accelerating growth. Operational discipline and AI integration cited as structural contributors.

🚩 RED FLAGS

Where Leadership Tone Diverges From Consensus

- CPB (Campbell Soup): Significant margin erosion, self-described operational failures, and a defensive shift in capital allocation toward debt reduction. Management halted buybacks and froze dividend growth.

- NCLH (Norwegian Cruise Line): New leadership explicitly acknowledged past failures and reset expectations, reflecting recognition of fundamental execution risk.

- KR (Kroger): Market share gains achieved through price investment, compressing margins. Growth and profitability pulling in opposite directions with no clear near-term resolution.

- ULTA (Ulta Beauty): Performance improvement attributed to sustained marketing and digital investment rather than organic demand recovery. Maintaining momentum requires continued spending, which limits margin expansion.

THE LEADERSHIP INDEX

The CEO Sentiment Trend

Season Summary

The season’s aggregate signal is a bifurcated market. Companies tied to AI infrastructure, power generation, and enterprise software reported the strongest demand environments, with capital allocation following conviction. Companies exposed to consumer spending patterns and residential construction reported conditions ranging from soft to deteriorating. Execution quality remained the primary differentiator within both groups.

Q1 2026 EARNINGS SEASON PREVIEW

Analysts are entering Q1 reporting season with above-average optimism. Aggregate S&P 500 earnings estimates have moved higher since January 1, with positive guidance issuers outnumbering negative by 59 to 51 among companies that have reported, above both the five-year average of 44 and the ten-year average of 40. Per FactSet, the blended year-over-year earnings growth rate for Q1 now stands at 13.2 percent, which would mark the sixth consecutive quarter of double-digit growth for the index.

The concentration of those revisions matters. Information Technology and Energy account for the large majority of upward estimate movement since December 31. Outside of those two sectors and a marginal gain in Financials, no other sector has seen aggregate earnings estimates improve. The revenue picture is broader, all eleven sectors are projected to report year-over-year revenue growth, but the earnings story entering this season is narrower than the headline number implies.

The macro backdrop introduces friction that the earnings estimates do not yet fully reflect. Morningstar’s economic research flags tariff-driven inflation as a near-term headwind that is likely to suppress GDP growth in 2026 before monetary easing provides relief in 2028 and 2029. Consumer prices are expected to absorb more tariff impact through this year, which creates pressure on margin assumptions for companies with exposed supply chains. Morningstar also notes that US stocks entered this earnings season carrying valuations above their ten-year average valuation-implied return of roughly 2.6 percent annually, a level that historically implies limited multiple expansion from current prices.

The tension entering Q1 reporting is therefore between an analyst consensus that is more constructive than normal and a macro and valuation environment that has become more complex since those estimates were set. Three S&P 500 companies are scheduled to report Q1 results this week. The full season begins in earnest the week of April 13.

FROM OUR SPONSORS

This AI Stat Will Shock You

But one little-known statistic suggests the entire sector could be on the verge of a massive collapse.

Warren Buffett once called it “the best single measure of valuations.”

Today, that indicator is flashing far above where it stood before the Dot-Com crash.

If this signal proves right, many AI favorites could fall hard.

See the warning sign and what investors should consider doing now.

Leadership intent sets the tone. Capital behavior confirms whether conviction follows.

SMART MONEY BRIEF

How Institutions and Insiders Are Positioning

This week’s activity reflects selective accumulation in growth-oriented technology and financial services names, alongside notable distribution in one large-cap technology position. The split within technology is the defining feature of the week.

ACCUMULATION & DISTRIBUTION

Where Smart Money Is Buying

- DDOG – (Datadog) The highest reported hedge fund accumulation of the week, alongside significant insider buying. The combination of institutional and insider conviction in the same name is the cleanest accumulation signal in this week’s data.

- NVDA – (NVIDIA) Strong hedge fund accumulation continues. Institutional interest in NVIDIA has been a recurring feature of recent weeks.

- HOOD – (Robinhood Markets) Substantial hedge fund accumulation supported by a cluster of insider buying. Internal and external conviction are aligned.

- KDP – (Keurig Dr Pepper), KHC – (Kraft Heinz) Both Consumer Defensive names saw notable hedge fund accumulation, consistent with rotation toward defensive exposures within a tape where Consumer Staples is one of the few sectors holding positive returns across multiple timeframes.

- ERIE – (Erie Indemnity)A cluster of insider buying events from multiple executives in financial services.

- WDAY – (Workday) A large individual insider transaction flagged as activist activity.

Where Smart Money Is Selling

- AAPL – (Apple) Pronounced hedge fund distribution. In a week where other technology names are being accumulated, the concentration of selling in a single large-cap name is notable.

CAPITAL REGIME CHECK

How Capital Behavior Aligns with the Broader Market

The one-month sector picture represents a meaningful shift from the trend established across longer timeframes.

Energy, which has led every horizon examined in recent weeks, is the only sector with a negative one-month return, declining 5.29 percent over the past month. At the same time, Technology is positive over one month at plus 4.67 percent, Communication Services is up 4.35 percent, and Real Estate has gained 4.00 percent. Financials have returned to positive territory over one month at plus 3.60 percent.

The longer-term picture has not changed. Energy remains dominant year to date at plus 32.52 percent. Technology, Communication Services, Financials, Consumer Discretionary, and Health Care all remain negative year to date. The one-month reversal in relative performance is a data point worth tracking but has not yet altered the established regime.

Utilities, Consumer Staples, Materials, and Industrials continue to hold positive returns across both short and long horizons. Real Estate has returned to modestly positive year to date territory.

FROM OUR SPONSORS

WARNING: A Major Market Shift Could Hit Stocks in 2026

If you have any money in the stock market, you may want to pay attention.

New research points to a massive market-moving event that could send hundreds of popular stocks into a sudden free fall.

Holding the wrong stocks when this hits could erase years of gains.

That’s why analysts have now identified a list of stocks investors may want to avoid as this event unfolds.

If you want to see what’s coming — and which stocks could be most at risk —

Click here to get the full details before it’s too late.

With positioning established, the next question is how the market is pricing uncertainty.

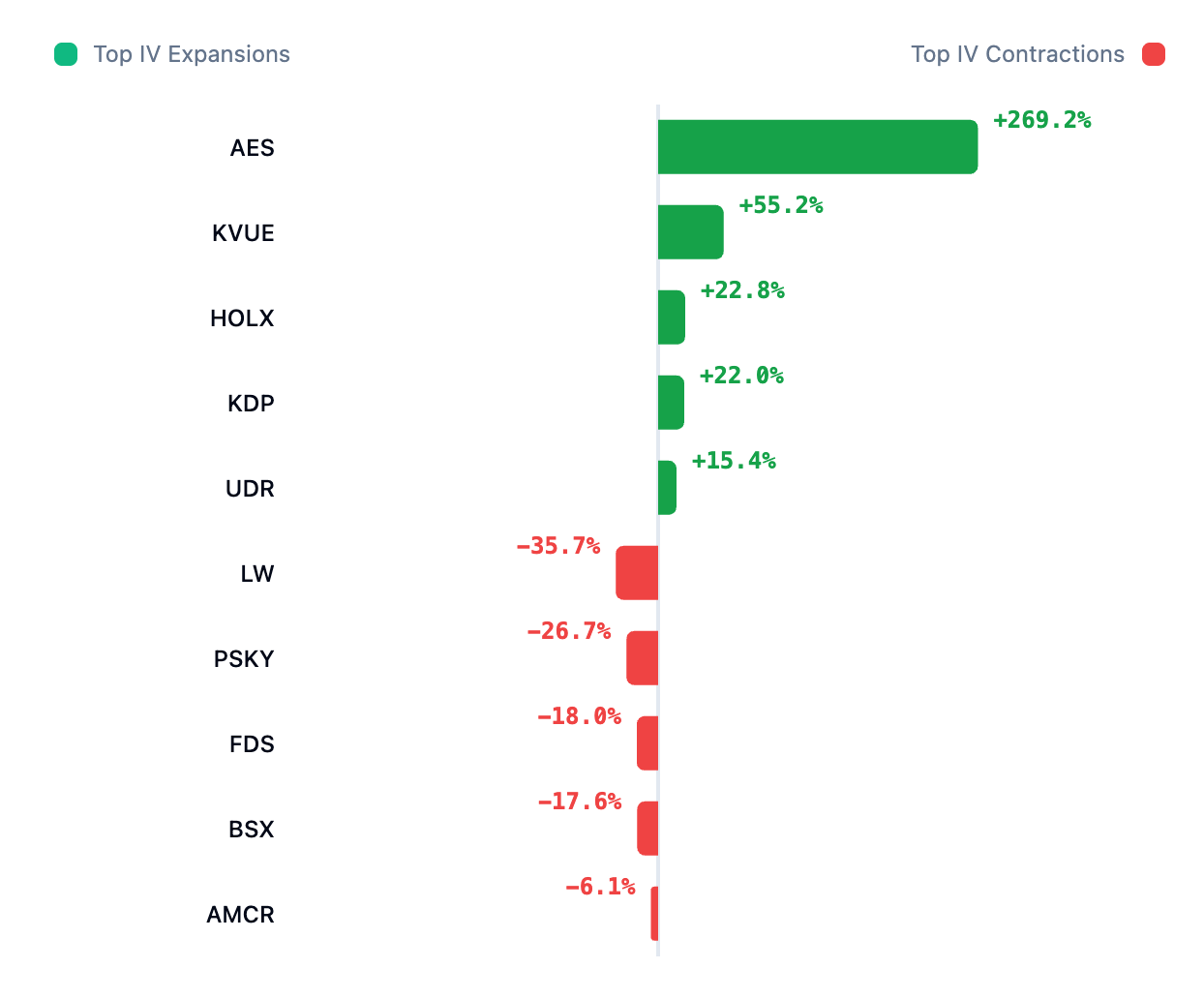

VOLATILITY SIGNALS

How Risk Is Being Priced

What Options Markets Imply About Future Movement

Cheap volatility this week: KMI at the 1st composite percentile, TT at 2nd, HOLX at 3rd, SNA at 3rd, and AMCR at 4th. Multiple names here are appearing on the cheap volatility screen for the second or third consecutive week.

Expensive volatility: GDDY, FDS, CSGP, ACN, and INTU all at or near the 100th percentile of their historical ranges across multiple horizons. GDDY and CSGP have now appeared at the top of the expensive volatility screen in consecutive weeks.

ASYMMETRIC BETS

Unusual Options Activity Worth Watching

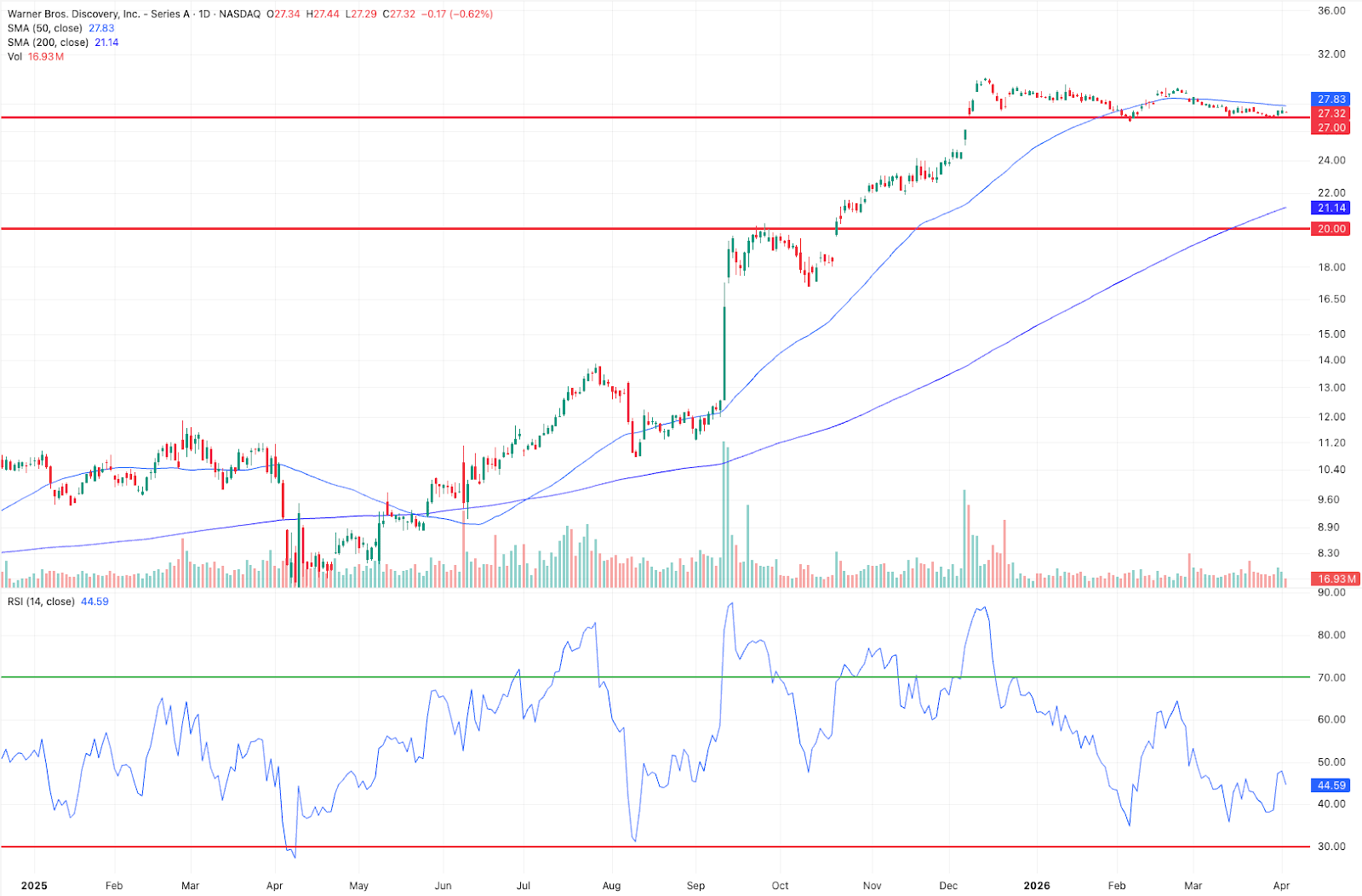

WBD – (Warner Bros. Discovery)

Paramount agreed to acquire WBD at $31 per share in February 2026, with the transaction expected to close in Q3 2026 pending regulatory clearance and a shareholder vote scheduled for April 23. The DOJ’s acting antitrust chief has stated the deal will not be on a fast track for approval.

Read against that backdrop, the put positioning is more interpretable as deal-break hedging than directional bearish conviction on the underlying business. Both the $20 and $27 strikes sit below the $31 acquisition price. If the deal closes, the positions expire worthless. If regulatory review blocks the transaction or introduces material delay, WBD reverts toward pre-deal levels.

The October 2026 expiration covers the window beyond the expected close date. A third consecutive week of large put positioning, now at a higher strike and with active volume of 6,171 contracts, is consistent with a participant continuing to build or add to a structured deal-risk hedge rather than a single speculative entry.

When intent, capital, and pricing align, the signal quality improves materially.

HIGH-CONVICTION SIGNALS

Outputs from the TQ Alpha Engine

KDP – (Keurig Dr Pepper)

Hedge fund accumulation alongside an implied volatility shift in the options market. Consumer Defensive accumulation in a name with active options repricing is a multi-channel signal.

AMCR – (Amcor)

Institutional accumulation converging with historically cheap implied volatility. AMCR has been a recurring presence on the cheap volatility screen.

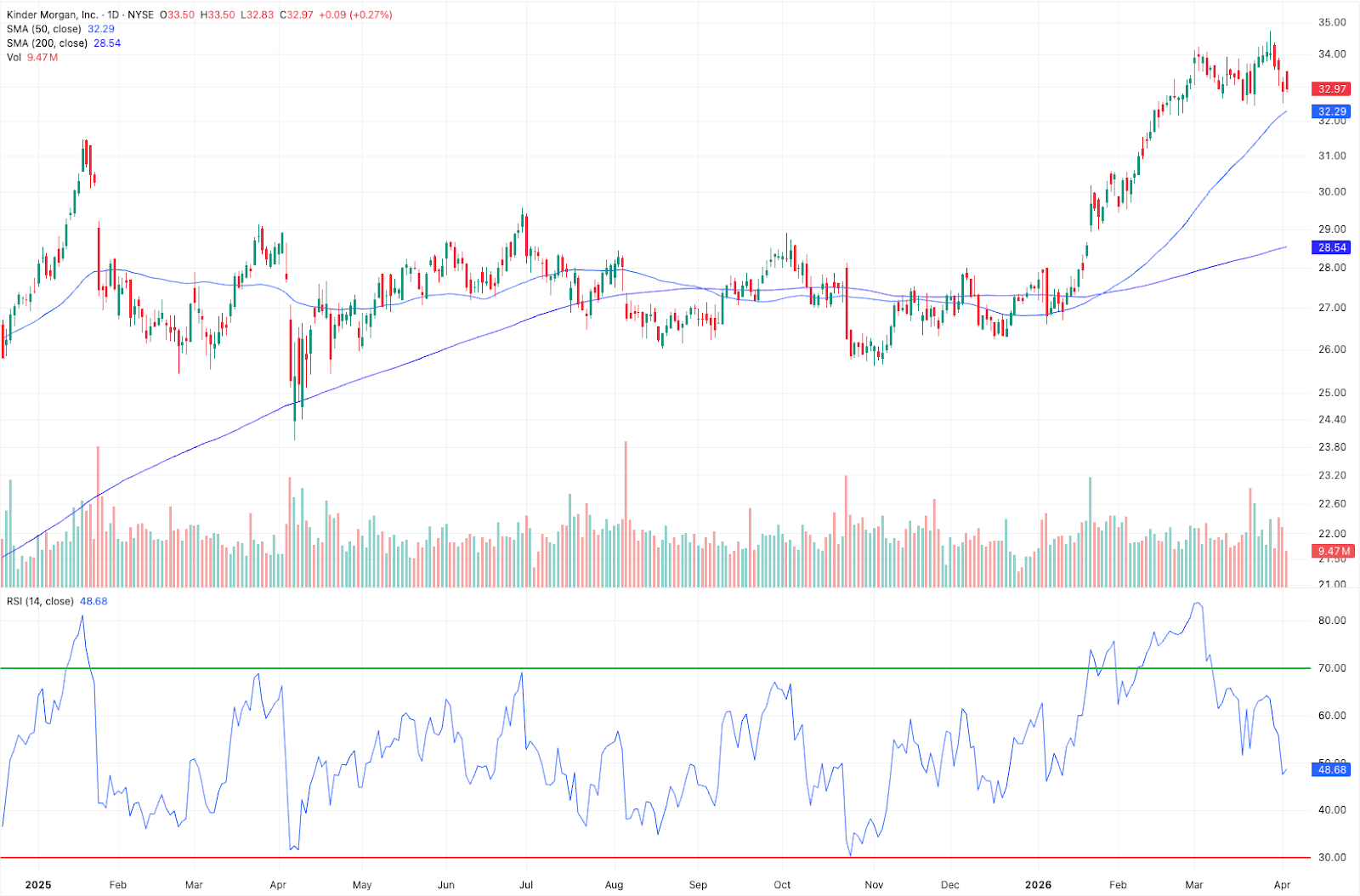

KMI – (Kinder Morgan)

Institutional accumulation alongside implied volatility at the low end of its historical range. The energy infrastructure name sits inside a sector that remains the tape’s dominant year-to-date leader despite a one-month pullback.

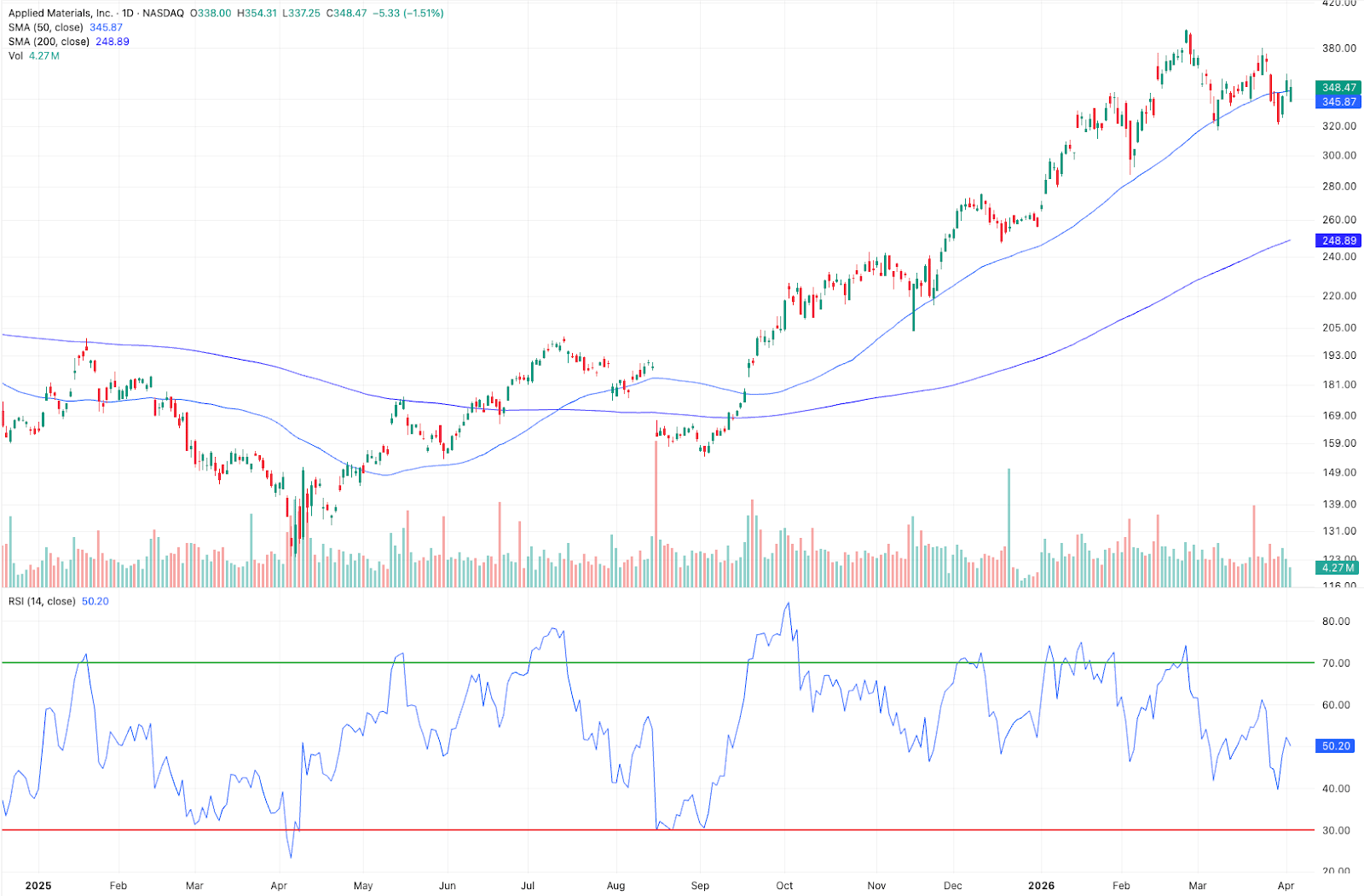

AMAT – (Applied Materials)

Institutional accumulation occurring while implied volatility is expensive. Buying into elevated options pricing reflects a different kind of conviction than accumulation in cheap volatility environments.

FROM OUR SPONSORS

The 2026 IPO calendar is taking shape – and it’s unusually concentrated

Instead of a scattershot list of early-stage hopefuls, the pipeline includes a handful of large private companies, each dominating a different segment of the economy.

At one end of the spectrum sits a global connectivity network. At another, the infrastructure powering enterprise AI.

There’s a digital finance platform generating margins that resemble software, not banking. And much more. And they all bring unique standout qualities to the table.

All detailed in this new report. Yours FREE.

BIG MOVE WATCHLIST

High-Probability Strike Zones

These equities screen with historically elevated probabilities of reaching a defined upside or downside target within the expected window. The edge is statistical resolution, not directional certainty.

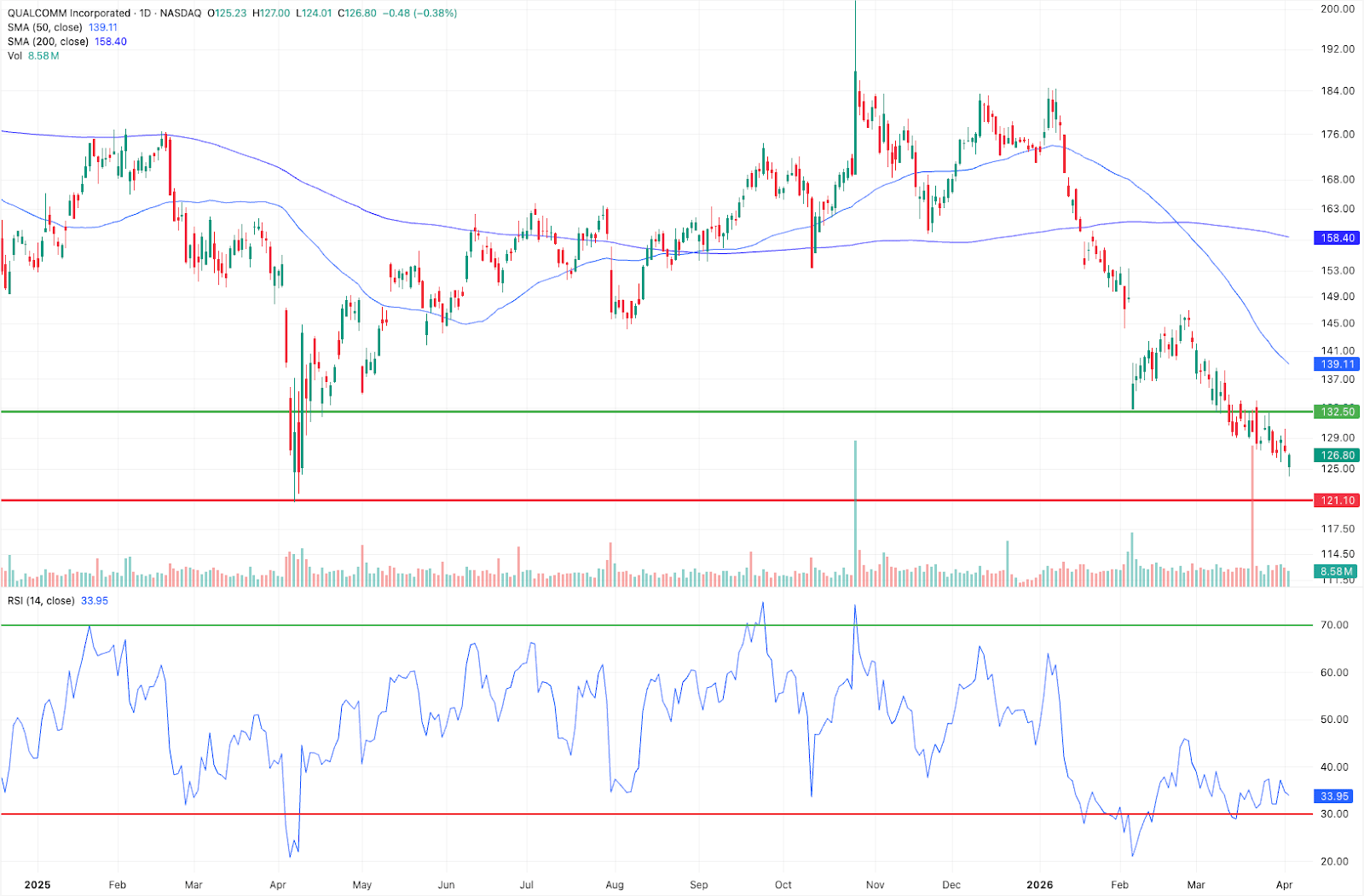

QCOM – (Qualcomm)

Overall Strike Rate: 82.1%

Upside Target: $132.50; Downside Target: $121.10

QCOM screens at a high resolution probability within a Technology sector that remains under pressure year to date but has shown a one-month reversal. The company enters the new earnings season with the memory shortage headwinds flagged in Q4 still present. The statistical setup reflects elevated odds of a decisive move in either direction rather than continued range-bound behavior. Catalysts to watch: Q1 earnings results due in the coming weeks, handset demand updates, AI-adjacent chip demand signals, and any commentary on memory supply normalization.

IBIT – (iShares Bitcoin Trust)

Overall Strike Rate: 82.1%

Upside Target: $40.40; Downside Target: $35.54

IBIT screens at the same strike rate as QCOM. Bitcoin ETF positioning reflects broader risk appetite conditions and is sensitive to macro shifts, rate expectations, and institutional allocation trends. The statistical configuration indicates elevated probability of range resolution from current levels. Catalysts to watch: Broader risk appetite signals, dollar strength or weakness, institutional crypto allocation flows, and any regulatory or macro developments affecting digital asset positioning.

THE WEEKLY SIGNAL

The April 5 signal map is defined by two features: the forward-looking setup for an earnings season that arrives with unusually high analyst expectations, and a set of capital behavior signals that reflect rotation rather than directional consensus.

The FactSet data establishes the baseline for Q1. Earnings estimates have moved higher since December 31. Positive guidance issuers outnumber negative. The projected 13.2 percent year-over-year growth rate would extend the double-digit streak to six quarters. The concentration of those upward revisions in Information Technology and Energy is worth carrying into the weeks ahead as company-level results begin to confirm or revise those expectations.

The one-month sector reversal is the most notable development in the capital regime data this week. Energy has pulled back while Technology, Communication Services, and Real Estate have gained over the past month. Whether this represents early rotation or a temporary consolidation within a sustained regime is not yet clear. The longer-term performance picture has not changed, and the one-month data point sits against a backdrop where the year-to-date and multi-month trends remain firmly in place.

Capital behavior this week was selective and internally consistent. Accumulation concentrated in specific growth technology names and defensive consumer positions. Distribution concentrated in one large-cap technology name. The alignment of hedge fund and insider conviction in DDOG and HOOD are the cleanest accumulation signals of the week.

Update your email preferences or unsubscribe here

© 2026 Traders & Quants, LLC

522 S. Hunt Club Blvd Suite 119

Apopka, FL 32703, United States Terms of Service