March 18, 2026

The Resolution Copper Deal Makes Supply Real Again

A decade long land fight just unlocked a deposit that could cover a quarter of U.S. copper demand.

Happy Wednesday, everyone!

Every AI data center, every EV charger, every mile of new grid needs one thing before a single electron flows.

Copper.

Not tokens. Not apps. Not hype. Real copper — dug from the earth, refined, and drawn into wire. Last week, two events showed that the world’s biggest miners are done waiting. They’re moving now.

The Land Deal a Decade in the Making

On March 16, Resolution Copper closed a historic land swap with the U.S. Forest Service. The venture — Rio Tinto (55%) and BHP (45%) — gained over 2,400 acres next to the old Magma copper mine in Superior, Arizona. In return, more than 5,400 acres of sensitive land went into lasting protection.

This was no press stunt. The law behind the swap passed with both parties’ support in 2014. It survived ten years of court fights. On March 13, the Ninth Circuit ruled in favor of the deal, denying requests to stop the exchange.

The deposit under that Arizona dirt is one of the largest untapped copper sources on Earth. Rio Tinto’s Copper Chief Katie Jackson said it plainly: the project “has the potential to satisfy up to 25% of America’s copper demand for decades to come.”

Twenty-five percent. One project. Read More

$500 Million Says This Isn’t Guesswork

Resolution Copper also announced roughly $500 million in early spending over two years. That money will fund surface drilling for more data, upgrades to current sites, early underground work, and about 100 new jobs.

This is not hope-stage cash. This is real capital from two of the biggest miners on the planet. Rio Tinto trades on the LSE at 6,754 pence — 10.63% below its 52-week high of 7,557 set on Feb 25, 2026. That dip tells you the market hasn’t yet priced in what domestic copper means in a world starved for the metal.

BHP just named a new CEO. The timing is no accident. A leadership shift at the world’s largest miner lines up with a clear pivot.

The pivot is toward copper.

The money is going into the ground. Literally.

The Global Squeeze Is Here

Rio Tinto grew copper output by 11% last year. That sounds strong — until you weigh it against demand. AI data center builds alone may need millions of extra metric tons of copper over the next decade. Grid upgrades, EV networks, defense systems, and autonomous platforms all chase the same tight supply.

And supply faces pressure from the other side, too. Mongolia wants Rio Tinto to redo the terms of its $18 billion Oyu Tolgoi copper mine, calling the current deal “unfair.” This is resource grab in real time — governments rewriting deals on deposits that cost billions to build.

Why Colombia Matters Now

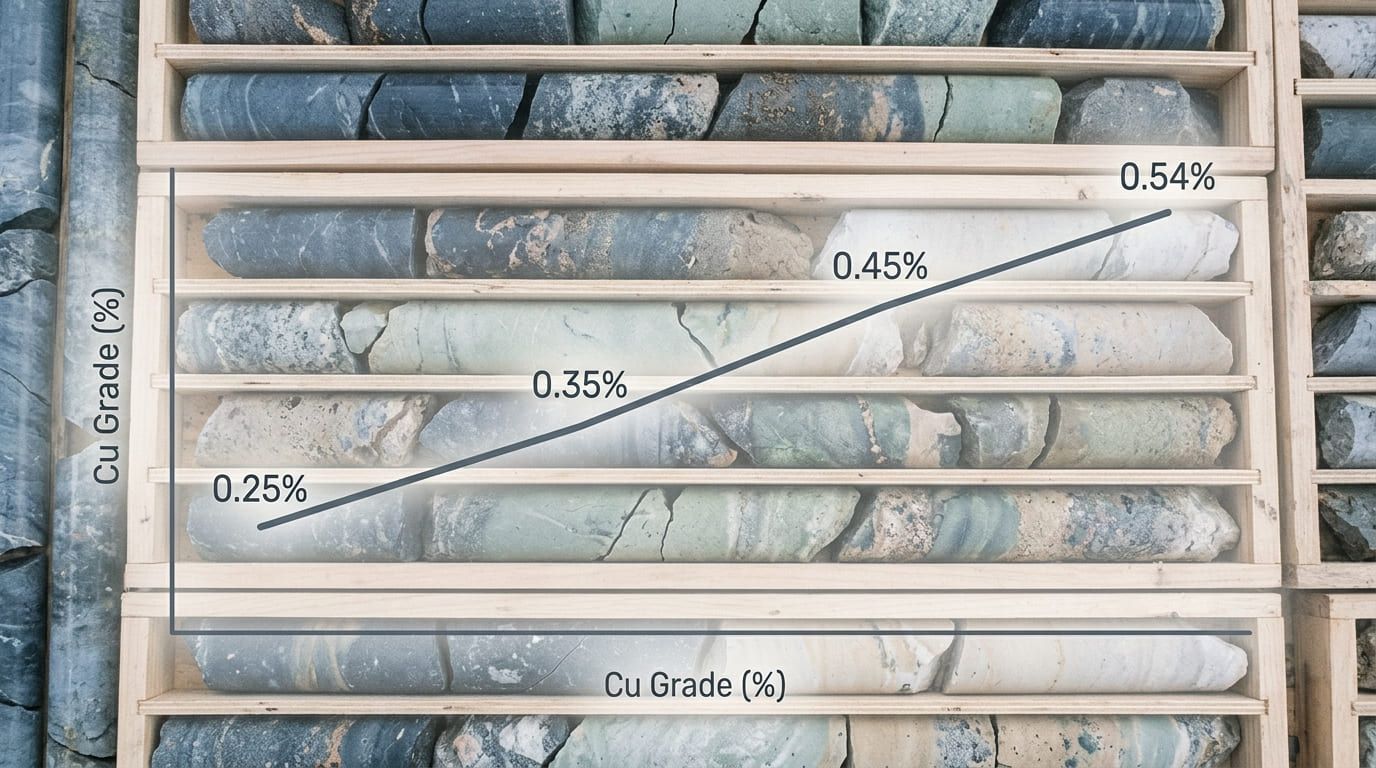

The Arizona story grabs the headlines. But a quieter signal came the same day. Copper Giant Resources Corp. shared drill results from its Mocoa project in southern Colombia. Hole MD-057 hit 532 metres at 0.25% copper — with a 191-metre stretch at 0.54%. Hole MD-056 found metal in a zone the old model had written off as waste.

That last point matters. It means the deposit is bigger than the model shows. Mocoa is already one of the largest untapped copper sources in the Americas. Two rigs run at full speed. Infill drilling aims to upgrade the resource class — the step needed before any formal study.

This is the early version of what Resolution Copper looked like fifteen years ago. Junior-stage, yes. But in a metal where every new pound of supply carries weight.

The Gap Smart Money Sees

The pattern is clear. The world needs far more copper. Old mines are aging. New ones take a decade or more to permit and build. Governments are clawing back supply from foreign sites. And U.S. output still covers only a fraction of what the country uses.

Rio Tinto and BHP aren’t spending $500 million on Arizona because a price chart looks nice. They’re spending it because the physical math doesn’t add up. Demand is built into the system. Supply is locked in the geology. The gap between those two facts is where big capital flows right now.

Bottom Line

The AI boom, the grid buildout, the push to electrify everything — none of it works without copper. And copper doesn’t come from code. It comes from holes in the ground, court rulings, land swaps, and billions in patient capital.

Smart money isn’t asking whether copper matters. It’s locking up the deposits.

The scramble is physical. The edge goes to those who saw it first.

We continually monitor these macroeconomic developments to ensure your capital remains protected. Please participate in our closing poll below.

How was this edition?

Exactly the kind of insight I come for Interesting, but I’d like to go deeper Not my topic

Warren Blake

Editor-in-Chief, Smart Trade Insights

Update your email preferences or unsubscribe here

© 2026 Smart Trade Insights

15 W 6th St

Tulsa, OK 74103, United StatesTerms of Service