Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

The #1 AI Investment

Elon + Nvidia =

Dear Reader,

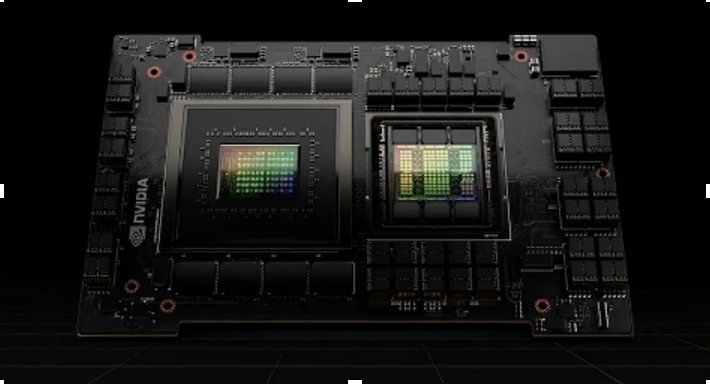

Do you see this weird looking device?

This is Nvidia’s holy grail.

It contains over 3 terabytes of memory…

80 billion transistors…

And can perform over 60 trillion calculations… per second.

This single computer chip goes for $25,000 a pop.

And now…

Elon Musk…

The world’s richest man…

Alongside Nvidia’s CEO Jensen Huang…

Are about to crank it up to 1 million.

At a remote facility in Memphis Tennessee…

You two of them have teamed up with an emerging tech titan…

To build the most advanced AI machine on the planet…

Powered by 1 million of these advanced AI chips.

This Will Unlock the TRUE Power of Artificial Intelligence!

But before you rush out to buy shares of Tesla or Nvidia…

There’s another investment you must consider.

You see, there is ONE company…

That Elon … and Nvidia…

And 98% of the Fortune 500…

Are ALL working with…

To prepare for AI 2.0.

Nvidia’s CEO has even said – this company is ESSENTIAL to their ongoing expansion.

>>>See how you can invest in this revolutionary company today.

Elon is expanding this project RAPIDLY…

And just announced a second AI computer…

That will need this company in order to build.

This may be the single greatest way to build wealth from the AI bull market.

But you must take action immediately.

AI is quickly becoming one of the MAIN focuses in Trump’s new administration…

And once Wall Street sees what this AI can really do — it will be too late.

>>>Go here to learn how to invest in Elon new AI venture.

Regards,

James Altucher

Editor, Paradigm Press

Exclusive News

Dell Just Hit a Record in AI Orders—But the Real Test Starts Now

Author: Leo Miller. Article Published: 12/2/2025.

In Brief

- Dell Technologies experienced a notable increase in value following the company’s latest earnings release.

- AI server orders broke records, and profitability in this part of the business returned to expected levels.

- Dell will need to execute strongly on its AI server demand in the long term and improve margins to be a true AI winner.

For many investors, Dell Technologies (NYSE: DELL)has become a divisive artificial intelligence (AI) stock. The company is seeing a large uptick in demand due to AI. Dell just reported its latest financial results, and AI orders hit a record high. If the company meets guidance next quarter, annual sales growth would be between 16% and 17% — a level Dell hasn’t reached in nearly four years.

Still, investors remain uncertain about Dell’s position in the AI ecosystem and whether it can emerge as a long-term winner. Dell’s latest results offer useful context for how the stock should be evaluated going forward.

Dell Raises Guidance as AI Orders Soar

Former Trump Advisor Shares Warning At Mar-A-Lago (Ad)

Trump’s Next Real Estate Deal Could Pay YOU President Trump’s real estate deals have returned as much as 4,800%. That’s enough to turn every $1,000 into $49,000. But his next “real estate deal” is different – and much bigger. It involves federal assets worth an estimated $5.1 trillion. And any American citizen can stake their claim. The mainstream media is largely ignoring this, but a former Trump advisor just went on the record.[GET THE FULL DETAILS HERE]

In Q3 fiscal year 2026 (FY2026), Dell reported revenue of $27.01 billion, an increase of 10.8%. (Note that Dell’s fiscal reporting period is one year ahead of the calendar year.) The result missed Wall Street estimates of $27.26 billion, which implied 11.8% growth. However, adjusted earnings per share (EPS) of $2.59 beat the $2.47 analysts anticipated.

Offsetting the sales miss, Dell raised its full FY2026 guidance for both revenue and adjusted EPS. It now expects sales of $111.7 billion at the midpoint (up from $107 billion previously) and adjusted EPS of $9.92 (up from $9.55). Management said the revenue shortfall was a timing issue rather than a demand problem: many sales expected in Q3 shifted into Q4, and there was enough additional demand next quarter to lift the full-year outlook.

Notably, Dell reported record AI server orders of $12.4 billion, and its AI server backlog rose to $18.4 billion from $11.7 billion in Q2 FY2026 — a clear sign demand exceeded supply. Markets reacted favorably: shares rose 5.8% on Nov. 26, and are up nearly 17% in 2025.

DELL’s AI Demand vs. Profitability: The Market’s Tug-of-War

Dell is clearly playing a significant role in AI, with strong server demand materially improving its outlook. A key question for investors, however, is how profitable those AI sales will be. When Dell builds AI servers it assembles components sourced from other companies.

That includes advanced parts such as NVIDIA (NASDAQ: NVDA) processing chips, high-bandwidth memory (HBM) and NAND memory. With industry concerns about NAND and HBM shortages, component costs can rise and squeeze Dell’s AI server margins.

Dell emphasized that AI server margins returned to its expected “mid-single-digit” range in Q3 after one-time pressures pushed them below target in Q2. That return is encouraging, but mid-single-digit margins remain thin; sustainable margin expansion will be critical for Dell’s long-term profitability.

One path to better margins is broadening the customer mix, a process that appears to be underway. Much current demand comes from large, low-margin neo-cloud customers, while smaller enterprise customers typically provide higher margins. As Dell wins more of those customers, overall AI server margins should improve. Dell says it has over 6,700 unique customers in its pipeline, which supports the idea of a more diverse customer base. Over time the company also hopes to sell more higher-margin hardware, software and services as it becomes more embedded in customers’ AI infrastructure — a credible strategy if it can execute.

Analysts Are Moderately Bullish on DELL

The MarketBeat-tracked consensus price target for Dell sits at just over $161, implying roughly 22% upside. The average price target among analysts who updated estimates after the earnings release is nearly identical.

Analysts see meaningful upside if Dell can demonstrate margin expansion on AI servers. That outcome would likely push price targets higher. Near-term risks include pressure from component pricing and supply constraints, but on balance Dell’s long-term risk-reward profile appears moderately tilted to the upside.

Investors will, however, want to see AI server margins stabilize and then improve over time to continue validating that thesis.

This email message is a sponsored message sent on behalf of Paradigm Press, a third-party advertiser of MarketBeat. Why did I receive this email message?.

If you have questions about your account, please contact MarketBeat’s South Dakota based support team at contact@marketbeat.com.

If you would no longer like to receive promotional emails from MarketBeat advertisers, you can unsubscribe or manage your mailing preferences here.

© 2006-2025 MarketBeat Media, LLC. All rights reserved.

345 North Reid Place #620, Sioux Falls, S.D. 57103. USA..

From Our Partners: 5 Stocks That Could Double in 2026 (Click to Opt-In)