I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

You are receiving this email because you subscribed to Liberty Through Wealth. Liberty Through Wealth is published by The Oxford Club.

To stop receiving special invitations and offers from Liberty Through Wealth, please click here. Please note: This will not impact the fulfillment of your subscription in any way.

Questions? Check out our FAQs. Trying to reach us?Contact us here. Please do not reply to this email as it goes to an unmonitored inbox.

Nothing published by The Oxford Club should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed personalized investment advice. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after publication before trading on a recommendation.

Any investments recommended by The Oxford Club should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Protected by copyright laws of the United States and international treaties. The information found on this website may only be used pursuant to the membership or subscription agreement and any reproduction, copying or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of The Oxford Club, LLC, 105 West Monument Street, Baltimore, MD 21201.

In mid-2022, Eric added Liberty Energy Inc. (LBRT) to Fry’s Investment Report, his flagship stock-picking service. It’s what people will now call “a totally obvious investment.” And it is… at least in hindsight.

Eric wrote to his readers…

Liberty offers an innovative suite of completion services and technologies to onshore oil and gas exploration and production companies… including next-generation all-electric fracking fleets.

Within two years, shares of the fracking company had surged 70% – even as oil prices dropped below $80 per barrel, down from $90.

That’s because companies like Liberty don’t rely on sky-high oil prices to make money. The Colorado-based firm earns money from completing new wells, regardless of energy prices.

In addition, many of America’s top shale producers are now so low-cost (in part from Liberty’s technologies) that they can remain profitable even if oil falls below $50 per barrel.

These are the types of bets we like making: one-sided “heads-I-win, tails-I-don’t-lose” wagers.

Markets are once again learning the importance of one-sided bets as the war in Iran turn oil markets into a guessing game.

On Tuesday, oil prices continued their double-digit decline after the White House said that “the war is very complete, pretty much.” The Pentagon soon painted an entirely different picture by stating, “We will not relent until the enemy is totally and decisively defeated.” Crude futures soon jumped double digits again.

Most speculators are playing the volatility the obvious way. They’re piling into oil ETFs and large-cap energy names… watching the WTI price ticker like it’s a scoreboard and hoping for the best.

But oil prices are unpredictable. Speculators win if prices go up… and lose equally if they go down. They might as well make money from guessing coin flips.

That’s why I want to look at companies with far better odds. These are investments that should do well, no matter where oil prices go.

So, to help protect your portfolios during this Middle East conflict, I’d like to highlight a Fry’s Investment Reportholding that should do well, regardless of whether oil surges to $120 or falls back to Earth.

The company is dealing with a fertilizer crisis that has barely registered on Wall Street’s radar, even as the signals are already flashing.

Then, I’ll share where you can find two additional plays that are benefiting from high oil prices.

“I predict OpenAI will go public this year… and I’ve found a little-known way for you to get in BEFORE its shares go public—with as little as $10.” That’s the prediction of Silicon Valley insider Luke Lango. He says this single investment is your best chance to achieve the biggest gains this year… and set yourself up for even bigger gains in the years to come. Best of all, he’s sharing a ticker symbol which you can use to claim a stake right now – for FREE. Click here to learn more.

Winning Wager Buy No. 1

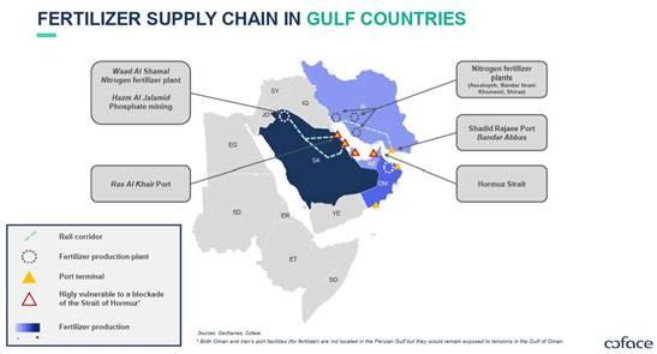

The Middle East isn’t just an oil and gas hub. It’s also a critical supplier of nitrogen-based fertilizers. Since 2020, six countries in the Persian Gulf have exported $50 billion of these crucial agricultural inputs. That means roughly 25% to 30% of global fertilizer exports pass through the Hormuz Strait.

Put another way, the Gulf states have a bigger share of the fertilizer market than they do of the oil and gas market.

The most direct beneficiaries have already seen the news reflected in share prices. CF Industries Holdings Inc. (CF) has surged over 45% since the start of the year, while Nutrien Ltd. (NTR) is up 20%. These companies are major nitrogen-based fertilizer makers and compete most directly with Middle Eastern imports.

However, one company has barely risen 7% since January:

The Florida-based firm is North America’s largest producer of potash and phosphate. In fact, it produces roughly 12% and 10% of the global output of these two nutrients.

Now, these two fertilizers are slightly different from the nitrogen-based types that the Gulf states export. So, the stock has barely risen since January.

Think of fertilizers like a three-legged stool. Each type represents a different leg, and you need all three to produce a stable crop. It’s why you’ll often see the “N-P-K” acronym on fertilizer bottles, and why fertilizing a lawn without soil testing first is a recipe for disaster.

In theory, these three nutrients are notinterchangeable.

However, different crops need different amounts of N-P-K. Corn requires more nitrogen, while soybeans rely on far less. So, high prices in one type of nutrient can often cause shifts in what farmers plant.

That’s why shares of Mosaic should soon rally. Farmers are very sensitive to price inputs, and rising nitrogen fertilizer prices will trigger a stampede into crops like soybeans. One researcher at the University of Arkansas’ System Division of Agriculture is already predicting 3.5 million acres of soybeans this year – a level not seen since 2017.

We’re also fast approaching the start of the U.S. planting season. So, even if nitrogen-based fertilizers are allowed past the Hormuz Strait within the next several weeks, many American farmers will have already locked in their potash and phosphate demand for the whole year.

In addition, MOS shares are relatively cheap. The stock trades at just half of long-term, midcycle valuations, and so even a return to normalcy gives shares a 2X upside. A windfall from higher fertilizer prices will only add to that.

In other words, even if Middle East conflict suddenly ends and we see a deluge of Gulf region products back on world markets, it would be too late for farmers in the Northern Hemisphere to switch back to nitrogen-based crops. MOS remains a top pick in Fry’s Investment Report, and you can get more ideas like this by clicking here.

2 Oil Stocks in the Wings

The global energy crisis is real. The oil trade is obvious. And obvious trades are usually already priced in.

This week’s wild reversals prove that point.

Many speculators piled into oil futures at $120 per barrel… only to see prices fall below $80 within days. They’re now sitting back near $90, as if calling for traders to try again.

But there are far better ways to invest in this market. Eric has two key picks in oil and gas in his Fry’s Investment Reportportfolio. The first company is at the forefront of America’s shale revolution, and the recent jump in global oil prices now gives it another leg of growth.

Here’s the fundamental case.

Eric’s first energy pick is one of America’s largest shale oil producers. The firm completed a merger in early 2026 and now produces 1.6 million barrels of oil equivalent per day – enough to fill up 4.5 million cars with gasoline.

It is also a relatively efficient producer, especially compared to global averages. The company’s breakeven oil price sits at just $44 per barrel and could reach the low-$40 range on post-merger cost savings. Even with oil prices pulling back, this means the company is stillprinting money and can still lock in $70-plus prices in the futures market.

It’s a guaranteed profit either way.

His second pick is in natural gas… and a company that’s quietly dominating the European landscape. Last week, Qatar was forced to shut liquefied natural gas (LNG) production after missile attacks from Iran began targeting energy infrastructure. The country makes up 20% of global LNG exports, and prices in East Asia and Europe have already spiked.

What’s worse, sources say it would take at least a month to return to normal production volumes… which might not happen for a while. After all, LNG tankers are essentially floating bombs.

That has had an immediate impact on European gas prices, which must compete with Asian buyers for supply. Dutch TTF Natural Gas Futures have spiked from $30 before the conflict to roughly $50… and could rise further as remaining winter stocks are depleted.

Meanwhile, Eric’s top European gas pick sits at a valuation that doesn’t reflect its situation. Prices continue to trade almost 20% below their 2022 peaks.

That gives it a solid double-digit upside from here.

I must also note that the company is astonishingly well run. Production grew 3.4% to record levels in 2025, and management expects another 3% increase in 2026 with breakeven levels of $40/barrel equivalent. This represents a 25% rate of return at $65/barrel of oil.

The company has a long history of managing windfall profits, and I expect shares to have double-digit upside from here.

The Bottom Line

No one can seem to agree where oil prices will go.

Betting markets expect oil to retest the $110 level by June, while futures markets expect a steady decline to around $80.

But Eric and I are not interested in making these kinds of 50-50 bets. Instead, we’re looking for investments with a greater guarantee of success, or those with such lopsided upside that the risks are worth taking.

(With those sorts of speculations, Eric has made 41 stock recommendationsthat went on to gain 1,000%+… 14 that gained 2,000%+… seven that gained 5,000%+… and two that gained 10,000%+. It’s why he’s often been called “Mr. 1,000%.”)

And in the meantime, be sure to keep checking your email. We’ll be sure to think outside the box when it comes to oil stocks. All of Wall Street’s attention is now fixated on crude oil prices and every word the White House is saying about them.

Take that opportunity to hedge with companies beyond their focus.

Manage your account We hope this timely investment research is valuable to you. As you know the markets move fast and conditions change frequently. So please check the current issue for the most recent advice. Please note that we cannot be liable for any missed bulletins caused by overzealous filters. To ensure that you continue to receive this valuable part of your service please take a moment to add services@exct.investorplace.comto your address book.

Tiny Biotech Firm NNVC Stands Out in a World Facing a Viral Epidemic Wave — Broad-Spectrum NV-387 Targets Viruses Killing Children and Adults Alike!

Viruses are wreaking havoc across the globe—this flu season has already caused millions of infections, RSV is killing children, and measles cases are forcing public health warnings.

Amid this mounting crisis, NanoViricides (NYSE: NNVC) is quietly developing NV-387, a broad-spectrum antiviral that has proven in animal studies to cure RSV, outperform Tamiflu and Xofluza against influenza, and target coronaviruses, smallpox, and MPox.

NV-387 completed Phase I with no adverse events and is now cleared to start a Phase II Mpox trial in the Democratic Republic of Congo, a major milestone that puts NNVC in the spotlight!

Investors should be paying attention now: NNVC isn’t just another biotech—it’s a potential game-changer in antiviral therapy,creating the first truly broad-spectrum treatment that viruses cannot escape.

With regulatory approvals in place and a platform that could target over 90% of human pathogenic viruses, NNVC represents a rare opportunity in the highly watched biotech space.

The Aging of America Could Make HCA Healthcare a Long-Term Winner

Submitted by Nathan Reiff. Published: 3/8/2026.

Key Points

HCA Healthcare has strong earnings growth, volume gains, and adjusted EBITDA gains, among other metrics, revealing strong fundamentals despite coming up short of analyst revenue estimates last quarter.

The company’s 2026 guidance suggests room to grow in several areas, though threats remain.

HCA’s recent rally may leave little room for short-term growth, but the stock could appeal to investors with longer-term healthcare demand trends in mind.

Shifting demographics in the United States mean that adults of retirement age or older will outnumber minors sometime in the coming decade. That growing population will require substantial spending on healthcare — a long-term structural tailwind that could create opportunities for investors who can take a multiyear view.

HCA Healthcare (NYSE: HCA) stands to be a primary beneficiary of this trend due to its large network of hospitals, surgery centers, urgent care locations and other facilities. The company is already seeing strong demand and utilization trends, and investors focused on the sector’s longer-term transformation may increasingly view HCA as an attractive buy.

A Mixed Earnings Report Masks Fundamental Strengths

HCA’s latest earnings report for Q4 2025, like those from many other healthcare firms, was mixed. The company comfortably beat analyst expectations for earnings per share (EPS), reporting $8.01 — an improvement of nearly 29% versus the $7.37 consensus.

That said, revenue growth of 6.7% year-over-year (YOY) was more modest than anticipated. Analysts had forecast quarterly revenue of $19.7 billion; the company missed that target by about $158 million.

Although revenue momentum was slower than some expected — reflecting policy headwinds, the expiration of premium tax credits and changes in uninsured rates, among other factors — the quarter still revealed several underlying strengths. HCA reported its 19th consecutive quarter of volume growth, adjusted EBITDA rose 11% YOY, and adjusted EBITDA margin improved by 80 basis points.

Patients are using HCA facilities at record rates, with roughly 47 million patient encounters in 2025 helping drive a 20% improvement in operating cash flow for the year.

Signs of Potential From HCA’s Guidance

One factor that may appeal to investors is HCA’s forward guidance. For 2026, management expects revenue of $76.5 billion to $80 billion and adjusted EBITDA of $15.55 billion to $16.45 billion. Diluted EPS is projected at $29.10 to $31.50.

HCA has also increased its capital plans, raising expected capital expenditures (CapEx) to as much as $5.5 billion and announcing a $10 billion share repurchase program. Current shareholders received a dividend increase as well: HCA raised its quarterly payout by 8.3% to $0.78, a yield of about 0.54% and a payout ratio near 10.15%.

Management’s outlook is supported by improving admissions trends. The company reported a 2.4% YOY improvement in same-facility admissions in the quarter and a 2.9% increase in same-facility revenue per equivalent admission. For 2026, HCA expects equivalent admissions to rise another 2% to 3%.

The Risks Remaining For HCA

HCA’s momentum does not eliminate risk. Executives expect an adverse impact to adjusted EBITDA in 2026 of $600 million to $900 million tied to changes in health insurance exchanges. State supplemental payments could also be a drag, with an expected decline in supplemental net benefits of $250 million to $450 million for the year.

The company is taking steps to offset some of these pressures through a $400 million resiliency program focused on improving revenue integrity and capacity management while applying cost-discipline measures, including investments in AI and digital tools. How effective those initiatives will be remains to be seen.

Still, Wall Street appears reasonably optimistic about HCA’s ability to navigate a challenging external environment. Analysts expect earnings to increase by more than 12% next year, and roughly two-thirds of the 25 analysts covering HCA have assigned a Buy or equivalent rating. Several analysts have already raised price targets or reiterated bullish views in 2026.

With nearly 14% capital appreciation year-to-date in 2026, HCA’s near-term upside may be constrained. But given the anticipated long-term growth in healthcare demand, the company could be a compelling long-term investment for patient investors.

This email message is a sponsored message from Equiscreen, a third-party advertiser of MarketBeat. Why did I receive this email?.

This message is a paid advertisement for Nanoviricides (NNVC) from Equiscreen and Interactive Offers. MarketBeat Media, LLC receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $14,000. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either Equiscreen or Interactive Offers. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding Nanoviricides (NNVC) on Interactive Offers’ website for additional information about the relationship between Interactive Offers and Nanoviricides (NNVC).

If you need assistance with your account, please don’t hesitate to email MarketBeat’s South Dakota based support team at contact@marketbeat.com.

This morning, Chris rang the Nasdaq opening bell with Eagle Nuclear Energy (NUCL).

Chris helped Weiss Members get into an early pre-IPO funding round for this uranium & nuclear energy tech company (formerly called Eagle Energy Metals) …

That means these readers were able to get in at a much lower valuation … and they were already way up long before most investors had a chance to get in.

This comes fresh off the heels of the Starfighters Space IPO, where Weiss Members saw peak returns so far of 777% … more than 3.6x greater gains than IPO investors.

(Chris rang the opening bell with them too, on the NYSE).

If you missed those amazing pre-IPO deals, I have great news:

In a few days, a new pre-IPO opportunity is opening to Weiss Members … and we believe the rewards could far surpass anything we’ve seen, for three reasons:

First, this company is an emerging leader in disruptive mining technology. But it’s no ordinary miner … they can extract 30+ high demand metals, including gold, silver, copper, rare earths and more … 10x faster and 70x cheaper than any traditional company … without digging, drilling or blasting anything at all.

Second, they’re using this tech to unlock a new source of high-grade metals valued at up to $60 BILLION per year … just as prices for these assets are reaching all-time highs, and record demand is pushing prices even higher.

Third, this is not just any pre-IPO funding round … it’s an “Alpha Round” deal. This is one of the earliest and most lucrative private investment rounds. At Chris’ Weiss Member briefing, he shared the proof of how Alpha Round investors in one company could have seen returns as high as 552,322% … enough to turn a $1,000 investment into $5.5 MILLION.

This new deal opens in just a few days, but you’ve got to reserve a seat at the table now.

Because pre-IPO funding rounds are first-come, first-served. Once the legal funding limit is reached, the round is closed, and it’s no longer possible to get any shares.

This is not like regular stocks. You can’t just go back the next trading day and try again. If you miss it, you’ll be stuck on the outside looking in.

Shop Sale at DICK’S Sporting Goods. If you find a lower price on Sale somewhere else, we’ll match it with our Best Price Guarantee.

— Read on www.dickssportinggoods.com/f/

Every day offers a new chance to grow—so explore stories filled with real-life inspiration, practical wisdom, and ideas that fuel your next step forward. Discover uplifting content curated to support your personal growth, and join thousands of readers who visit our site daily for motivation, insight, and a positive boost.

“Renewal is not about becoming someone new—it’s about remembering who you’ve always been beneath the weight of the world.”

As nature renews itself this season, you can too. Reconnect with parts of yourself you’ve neglected. Revisit dreams you put on hold. Remember what brings you joy before life got so complicated. This is your invitation to come back home to yourself, to shed the layers that aren’t truly you, and to let your authentic self emerge once again.MORE INSPIRATION

You’re always one blessing away from a brighter day… and a bigger life. May these stories, affirmations, prayers, and insights lift your spirits and inspire you to lift others.