I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

You are receiving this email because you signed up for Monument Traders Live. To stop receiving special invitations and offers from Monument Traders Live, please click here. Please note: This will not impact the fulfillment of your subscription in any way.

Please do not reply to this email as it goes to an unmonitored inbox.

Nothing published by Monument Traders Alliance should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed personalized investment advice. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after publication before trading on a recommendation.

Any investments recommended by Monument Traders Alliance should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Protected by copyright laws of the United States and international treaties. The information found on this website may only be used pursuant to the membership or subscription agreement and any reproduction, copying or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of Monument Traders Alliance, LLC, 14 West Mount Vernon Place, Baltimore, MD 21201.

Step #2: Join me at 2 p.m. ET this coming Wednesday, April 8.

That’s it.

I’ll send you your report after our strategy session.

Inside, I’ll tell you about an AI winner that I believe is perfectly positioned to cash in on $700 billion investments in AI data centers and other AI infrastructure.

And I’ll tell you about one AI loser to avoid.

This company is losing money… sales are declining… and insiders are dumping shares.

I wouldn’t be surprised if shares go to $0.

You’ll find the names, ticker symbols and all the details inside this report.

Again, you won’t have to pay a penny to claim this report.

All you need to do is follow those two steps.

Click here to get started, and when you upgrade, I’ll also send you complimentary text alerts about this event.

This is hands-down the best way to ensure you don’t accidentally miss our event.

And that’s super important because Elon Musk is planning to soon release a new game-changing AI model that I believe will trigger even more disruption and crashes.

If you accidentally forget about this event…

You could miss out on a rare chance to double, triple your money or more… in 30 days or less during this coming wave of disruption.Claim Your Free Bonus

And I’ll talk to you this coming Wednesday, April 8, at 2 p.m. ET.

The market keeps rallying… but we’re still “on the wrong side of the tracks”… Luke Lango’s bull case for tech… a black swan lurking in the Middle East… and a dark question about AI’s future we’ll be tackling soon

As I write on Wednesday, stocks are continuing yesterday’s rally, spurred on by positive geopolitical headlines.

This morning, President Trump posted on Truth Social that Iran’s president has requested a ceasefire – adding that the U.S. would only consider the proposal once the Strait of Hormuz was “open, free, and clear.”

Meanwhile, the United Arab Emirates is reportedly preparing to help open the Strait by clearing it of mines, while also encouraging neighboring Gulf states to join the effort.

Here’s The Wall Street Journal:

Emirati diplomats have urged the U.S. and military powers in Europe and Asia to form a coalition to open the strait by force…

Saudi Arabia and other Gulf states are now turning against Iran’s regime and want the war to continue until it is disabled or toppled.

Altogether, it’s enough to keep optimism high and market gains coming. The S&P 500 is up about 3.5% over the past two sessions as oil prices fall – it’s a welcome exhale after one of the roughest stretches of the year.

Let’s pull back and get some perspective

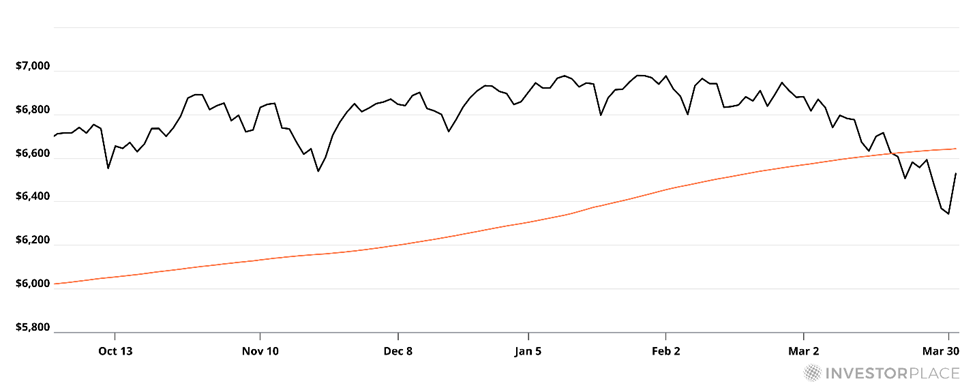

Even with this two-day bounce, as I write, the S&P remains roughly 6% below its January peak. The Nasdaq and the Dow – which both temporarily crossed into official correction territory – are still down about 9% and 7%, respectively, from their highs.

As you can see from the chart below, even after our two-day bounce, the S&P 500 is still trading below its 200-day moving average (MA).

Here’s how Brian Hunt, editor of the free e-letter Money & Megatrends, described the significance of being below the 200-day MA in last Friday’s issue:

Stocks, ETFs, and indexes below their 200-day moving average are “on the wrong side of the tracks.” It’s the ugly part of town.

All the really bad things — crashes, panics, horrible bear markets — happen below the 200-day moving average.

But look back at the chart, and you’ll see that the S&P is looking to retake that key technical level.

Will the market break through and continue to strengthen? Or will the S&P get rejected and begin a deeper leg lower?

Brian points out that today’s fundamentals, valuations, and interest rates aren’t driving the recent price action in the broad market. The volatility is nearly exclusively due to Operation Epic Fury and President Trump’s social media posts.

So, he sees a simple binary that could influence this 200-day MA test:

If the war ends soon, the S&P is very likely to pop higher and get back on the right side of town.

If the war does not end soon, its constriction of critical resource supplies will seriously damage the global economy and stocks will trade lower.

Bottom line: The last two days are encouraging. But the resolution remains unclear – and as we noted in yesterday’s Digest, even a ceasefire doesn’t automatically reopen the Strait, which will have the greatest influence over oil prices and, by extension, inflation, interest rates and the rest of the tipping dominoes.

Brian publishes his free e-letter every day the market is open. If you’re interested in learning more about the megatrends that are driving the market today, sign up for Money & Megatrends right here.

Now, even amid this uncertainty, our hypergrowth expert Luke Lango, editor of Innovation Investor, is betting on a bullish outcome.

Elon Musk recently held an all-hands meeting at his closely guarded AI lab. He told employees… “We’re moving faster than any other company. No one’s even close.”Why? Because Elon built an AI breakthroughthat would take most tech CEOs four years to set up. He brought it online this year… and as early as today, April 1… Elon’s going to crank it to full blast. And potentially make ChatGPT, Claude, Gemini, and DeepSeek obsolete… While unleashing a brand-new 7,000% growth market. But here’s the twist. Neither Tesla nor SpaceX is the best way to play this opportunity. Instead, you’ll want to own the firm that controls over 38,000 patents on the technology (not semiconductors) that will power Elon’s career-defining vision. Click here for its name and ticker symbol.

Luke’s bull case: why he thinks this rally could have real legs

Even with the market below its 200-day MA, Luke sees a compelling setup building beneath the surface – particularly for tech and AI investors.

He notes a few converging signals. First, market breadth has deteriorated to levels historically associated with correction bottoms – the kind of readings that, in past cycles, marked the zone of maximum dislocation between price and fundamental value.

Meanwhile, fear indicators are compressing from their peaks, suggesting the worst of the uncertainty may already be priced in.

And the correction math itself is encouraging. Luke’s research found that every market pullback since 1950 that was constrained to 10%-20% went on to post an average six-month return from the trough of roughly 24%.

But the most bullish piece of Luke’s argument is the valuation reset in tech specifically. Here’s Luke from his most recent Innovation Investor Daily Notes:

Tech stock valuations have reset to levels that are genuinely compelling relative to the confirmed earnings growth trajectory.

The S&P 500 tech sector’s forward earnings multiple has compressed to 20.5X — essentially a post-COVID low, and just above where tech stocks bottomed in the 2022 bear market.

Over the next three years, tech earnings are projected to grow at a 25% CAGR. So, at current levels, investors are paying 20X forward earnings for ~25% compounded earnings growth.

That’s a very attractive setup.

Luke’s takeaway is that while we may not be at the exact low, waiting for a perfect all-clear signal could mean missing the opportunity. In his words, we’re “bottom enough.”

Now, shifting from the obvious impact of the Iran war on Wall Street, there’s a new related issue that could be a black swan lurking ahead…

The new brewing risk to the AI trade

While all eyes are on oil and the Strait of Hormuz, a quieter supply chain story is developing that AI and tech investors should closely track.

Helium.

The same invisible gas that keeps party balloons aloft is also essential for cooling the machines that manufacture AI chips – and right now, roughly a third of the world’s supply is offline.

Iran’s strikes on Qatar’s Ras Laffan LNG facility earlier this month didn’t just disrupt natural gas. They disrupted helium production lines that could take up to five years to repair.

Qatar supplies about a third of global helium, and virtually all of it travels through the Strait of Hormuz – which, despite Wall Street’s two-day party, remains paralyzed.

Here’s Entrepreneur on Monday:

Without helium, leading chip makers including TSMC, Samsung and SK Hynix could struggle to keep production running.

Helium cools superconducting magnets during chip manufacturing and flushes toxic residue after wafers are washed.

The gas is irreplaceable for making chips that power iPhones and Nvidia’s AI servers.

There is no easy substitute here. Helium’s unique combination of thermal conductivity, chemical inertness and atomic size makes it irreplaceable in chip fabrication.

The Semiconductor Industry Association acknowledged this in a 2023 filing to the U.S. Geological Survey, warning that a supply disruption “would likely cause shocks to the global semiconductor manufacturing industry.”

And though some headlines cite “months” of helium reserves, the inventory picture is more precarious than it sounds. The gas is notoriously difficult to contain. As Lita Shon-Roy, president and CEO of semiconductor materials advisory firm TECHCET, told Scientific American:

Helium can leak out about 0.1 to 1 percent per month, depending on how good the gaskets are. There’s never a good gasket or fitting. It just leaks over time.

Meanwhile, roughly 200 specialized cryogenic containers used to transport liquid helium – each worth about $1 million – were stranded near the Strait when the war began.

Industry consultant Phil Kornbluth told The Wall Street Journal that repositioning, refilling, and delivering those containers alone could take months.

Here’s his overall assessment:

There is a tsunami coming, but it’s still a thousand miles offshore.

So, where might that tsunami hit?

Of the major chipmakers, Samsung and SK Hynix appear most exposed. Both are heavily dependent on Qatari supply and are critical producers of the high-bandwidth memory (HBM) inside Nvidia’s AI servers.

Taiwan Semiconductor Manufacturing Company (TSMC) carries its own exposure as the foundry behind chips for Nvidia (NVDA). Meanwhile, Micron (MU), with more diversified sourcing, looks better positioned in the near term, but still has exposure.

But the helium story also has an unexpected winner hiding in plain sight: ExxonMobil (XOM).

Its Shute Creek facility in Wyoming accounts for roughly 20% of global helium production capacity and has an 80-year reserve runway. As 24/7 Wall St.noted, the shortage “hands Exxon a low-effort margin expander at a time when chip demand for AI keeps climbing.”

For investors already holding XOM for its oil-and-gas core, the helium angle makes it even more interesting. For new money, it’s worth putting on your radar.

The key variable, as with everything right now, is time. A swift ceasefire resolves this before it becomes critical. But a prolonged conflict turns a distant tsunami into a very close wave.

We’ll keep you updated.

Finally, another round of layoffs – and a darker question for AI investors

By now, most investors are familiar with AI’s threat to jobs. It’s the story everyone is watching.

But there’s a less-discussed question starting to surface – one I’ll tackle in a deep-dive Digest soon. It goes something like this…

What if AI will eventually be just as destructive to most AI companies as it is to the workers they’re replacing?

Consider Oracle (ORCL)…

Yesterday, the software giant announced a new round of layoffs – TD Cowen estimates between 20,000 and 30,000 workers – even as it simultaneously ramps AI infrastructure spending aggressively. Oracle has committed to a jaw-dropping $455 billion in remaining performance obligations following its OpenAI agreement, all while reshaping the company around the AI buildout.

And yet ORCL is down 25% this year. Part of that reflects investor concern about cash flow amid surging capital expenditures. But another part reflects something more unsettling…

The market is beginning to ask whether generative AI threatens not just Oracle’s employees – but its core business.

This question extends well beyond Oracle

It cuts to the heart of the entire AI investment thesis…

If AI commoditizes intelligence, who actually wins?

The companies building it?

The companies deploying it?

Or, maybe, nobody?

And – perhaps most unsettling – what about the investors currently holding the companies that appear to be winning right now?

The recent answer – own the infrastructure layer, the picks-and-shovels, the Nvidias of the world – has served investors well. And it will likely continue to… for at least a while.

But that thesis rests on one assumption: that demand for AI compute will keep compounding indefinitely. However, what happens if the economics of AI start working against that assumption?

What if we’ve started a race to the bottom that eventually circles back to the infrastructure layer, too?

That’s a bigger conversation than we have room for today. But it’s coming.

For now, here’s our takeaway

Oracle slashing potentially tens of thousands of jobs while simultaneously betting $455 billion on AI infrastructure isn’t a contradiction. It’s what the AI structural reset looks like in real time.

The technology is reordering how companies are built, staffed and financed – and that process is still in its early chapters.

Yes, short-term headwinds are real…

There are potential supply shocks like helium… unresolved geopolitics… and an S&P still on the wrong side of the 200-day MA. These are meaningful speed bumps.

But as Luke reminds us, investors are currently paying 20X forward earnings for roughly 25% compounded earnings growth in tech. Whatever the road ahead looks like, that’s an attractive set-up.

Have a good evening,

Jeff Remsburg

(Disclaimer: I own MU.)

Manage your account We hope this timely investment research is valuable to you. As you know the markets move fast and conditions change frequently. So please check the current issue for the most recent advice. Please note that we cannot be liable for any missed bulletins caused by overzealous filters. To ensure that you continue to receive this valuable part of your service please take a moment to add services@exct.investorplace.comto your address book.

But I’m here to tell you there’s no reason to panic.

You see, this coming Wednesday, at 2 p.m. ET… I’m having a strategy session called AI Doomsday to show you how to turn all this volatility into big gains.

Click here to automatically save your seatbecause I already shared this “crash to cash” strategy with some of my readers… (When you click the link, your email address will automatically be added to my guest list.)

And they had a chance to turn…

A 49% crash in Wolfspeed into a $22,500 payout… A 13% quick drop in Amer Sports into almost $25,000 in just five days… And a 21% drop in Valaris into $30,000 in just about three weeks.

Those are the kinds of opportunities I will be targeting in the coming days.

You see, I believe all the volatility we’ve seen so far in 2026 is just the beginning of a period of extreme disruption I’m calling “AI Doomsday.“

Do nothing, and you could lose a big chunk of your savings.

Because Elon Musk is planning to release a new AI model in April… And I believe it will accelerate this tech disruption in ways most people can’t even imagine.

Sure, some AI winners will skyrocket overnight… A lot of people will get rich. But several other companies will collapse just as quickly.

I believe fortunes will be made and lost at record speed in the coming months… And I’d like YOU to be on the winning side of this massive disruption that I’m calling AI Doomsday.

We may be getting closer and closer to the death of the dollar…

But it won’t look like what most people expect.

It won’t have anything to do with inflation or a government collapse…

What’s actually happening is much more dangerous for you than that.

Right now, the wealthiest people in America — Musk, Zuckerberg, Ellison — are systematically moving their money out of dollars and into a completely different type of currency. One that you’ve likely never been taught about.

It’s not bitcoin or any other crypto.

But after nearly five decades on Wall Street, I’ve never seen a new trend accelerate this quickly.

As I’ve been telling others: “The wealth transfer already underway will make the Gilded Age look like a warm-up act.”

What exactly is going on? And what does it mean for every dollar you’re currently holding?

I’ve put together an urgent briefing with everything you need to know.

Editor’s Note: Silicon Valley legend Jeff Brown is forecasting that Elon Musk’s “Kardashev Project” is about to trigger the greatest wealth creation event in history.

While everyone is talking about the SpaceX IPO, Elon Musk has moved on to bigger and better things…

With the potential to be much more lucrative for folks who make the right moves today.

Everything is coming together quickly.

Tesla and xAI’s newly announced “Macrohard” project could disrupt the entire software industry.

But it’s just one small part of Elon’s next move… one more blurring of the lines between his companies.

Once his plan is complete everything about the way we look at Elon Musk and his companies like SpaceX and Tesla will change.

Elon believes it will even trigger a quadrillion dollar wealth creation event…

And give folks a shot at up to 500%+ gains in the near term and far more in the years to come as Elon Musk makes the world’s first $10 trillion company.

Silicon Valley insider, Jeff Brown, put together a brief video explaining Elon’s masterplan…

The drastic move he could make as soon as the end of this month…

And exactly where investors should position themselves today.

You are receiving this email because you subscribed to Wealthy Retirement. Wealthy Retirement is published by The Oxford Club.

To stop receiving special invitations and offers from Wealthy Retirement, please click here. Please note: This will not impact the fulfillment of your subscription in any way.

Questions? Check out our FAQs. Trying to reach us? Contact us here. Please do not reply to this email as it goes to an unmonitored inbox.

Nothing published by The Oxford Club should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed personalized investment advice. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after publication before trading on a recommendation.

Any investments recommended by The Oxford Club should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Protected by copyright laws of the United States and international treaties. The information found on this website may only be used pursuant to the membership or subscription agreement and any reproduction, copying or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of The Oxford Club, LLC, 105 West Monument Street, Baltimore, MD 21201.

In 1564, the teenaged King Charles IX moved New Year’s Day from the spring equinox to January 1. What followed was basically a 16th-century communication disaster.

Those who didn’t get the news, or were slow to adapt, were labeled “April fools”.

One royal decree began centuries of pranks.

This calendar confusion is just one working theory for the origins of today’s mischief-filled holiday. But it serves as a timely reminder: Change is messy, and it is easy to fall behind.

We see this playing out with the U.S.-Iran conflict.

Oil prices are hovering around $100 per barrel and are expected to remain high, driven by intense volatility, geopolitical risks, and fears of a prolonged supply shock. The Strait of Hormuz, a key oil shipping route, remains closed to most shipping traffic. And analysts at Wood MacKenzie are warning oil could rocket to more than $200 a barrel.

This is the new normal. Oil prices are not merely high, they are thrashing around wildly from day-to-day. But even though oil is grabbing most of the headlines, it is not the only commodity under the thumb of the Iran conflict.

It turns out that when a butterfly flaps its wings in the Straight of Hormuz, a tsunami of chaos sweeps over nearly every commodity industry in the world.

Today, I’d like to focus on another major global commodity – aluminum – and how to position your portfolio before this growing ripple effect turns into a full-blown supply shock.

Elon Musk recently held an all-hands meeting at his closely guarded AI lab. He told employees… “We’re moving faster than any other company. No one’s even close.”Why? Because Elon built an AI breakthroughthat would take most tech CEOs four years to set up. He brought it online this year… and as early as today, April 1… Elon’s going to crank it to full blast. And potentially make ChatGPT, Claude, Gemini, and DeepSeek obsolete… While unleashing a brand-new 7,000% growth market. But here’s the twist. Neither Tesla nor SpaceX is the best way to play this opportunity. Instead, you’ll want to own the firm that controls over 38,000 patents on the technology (not semiconductors) that will power Elon’s career-defining vision. Click here for its name and ticker symbol.

When Oil Moves, Aluminum Follows

Like oil, aluminum prices have swung wildly since the U.S. launched its first attacks on Iran in February. That’s because the war is causing a double-whammy for the aluminum market.

First, it is directly eliminating most of the Middle East supply, which accounts for about 10% of the world total. Second, it is driving the price of energy much higher. That’s bad news for aluminum production, which requires huge volumes of electricity.

By definition, therefore, an energy shock is an aluminum shock.

We saw this scenario play out in the 1970s, when oil prices surged due to geopolitical conflict and embargoes. Electricity costs jumped globally, and aluminum smelters become costly to run.

As a result, high-cost regions, like the U.S., Western Europe, and Japan curtailed aluminum production. Predictably, supply tightened… and prices rose.

Now, higher prices can be a tailwind for aluminum companies. When prices go up, producers sell aluminum at increased prices. In turn, their revenues and profits can climb.

But there’s a catch.

If aluminum prices rise because energy costs are also rising, then costs are going up at the same time as aluminum prices, and profit margins may not improve much.

That means that the real aluminum winners will be those with cost advantages – like access to cheap electricity or stable energy, especially hydro and nuclear power.

These companies will benefit from rising aluminum prices without much of their own costs rising.

Alcoa Corp. (AA) is better positioned than many other aluminum producers. The company has been preparing for this moment for decades, literally.

Alcoa’s Structural Advantage

Alcoa is not just the largest American aluminum producer; it is also among the world’s most environmentally progressive.

As I mentioned, producing aluminum requires immense amounts of electricity, and that energy intensity is reshaping the industry. Increasingly, companies such as Tesla Inc. (TSLA) are seeking to source their aluminum from clean-energy smelters powered by hydro, nuclear, or renewables. That shift is elevating low-carbon producers like Alcoa to the top tier of the aluminum world.

Today, renewable energy powers roughly 87% of Alcoa’s smelting operations. This alignment with the global push toward decarbonization gives the company a durable strategic advantage, and positions it not merely as a cleaner metal producer.

After suffering a tariff-induced selloff in early 2025, Alcoa’s shares have been trending higher. And since the butterfly flapped its wings in the Middle East, the company has soared on aluminum supply concerns.

This past weekend, Iran attacked two of the region’s producers. Emirates Global Aluminium, the area’s top aluminum supplier, said it sustained “significant damage” at its Abu Dhabi site. Aluminium Bahrain, the second target, is examining the damage at its own facility.

Meanwhile, Alcoa’s smelters continue humming along and churning out aluminum.

Beyond a conflict-related rally, I expect Alcoa’s uptrend to gain momentum – driven not only by firmer aluminum prices, but also by the company’s exceptional fundamentals. The company beat Wall Street’s expectations for the fourth quarter 2025, and is expected to release its next quarterly report on April 16.

Alcoa currently trades for less than 12 times estimated 2026 earnings – well below its historical forward multiple of roughly 20 times earnings. So, although the shares of this leading aluminum producer are climbing higher, they are still relatively “cheap” compared to estimated earnings… and I should point that Wall Street has been busily raising its estimates for this year.

Alcoa is one of the several commodity-related companies I recommend in Fry’s Investment Report.

As a member, you’ll get access to all of my latest research, reports, and trade alerts. (There is no chance of becoming an unsuspecting “April fool” here.)

The bottom line is that commodity markets, like aluminum, are excruciatingly capital intensive, requiring years, long or decades, long lead times, and do not often immediately reward those spectacular investments.

But inevitably, a shock of some kind arrives, either due to simple supply demand factors, tariffs, wars, or acts of God.

When those moments arrive, commodity-focused companies ring the register in a big way.

Manage your account We hope this timely investment research is valuable to you. As you know the markets move fast and conditions change frequently. So please check the current issue for the most recent advice. Please note that we cannot be liable for any missed bulletins caused by overzealous filters. To ensure that you continue to receive this valuable part of your service please take a moment to add services@exct.investorplace.comto your address book.

Blake Young just exposed a major crack in the consumer discretionary rally. Tesla now accounts for 20% of the entire sector, and today’s 2.6% bounce is dragging XLY higher while the actual consumer stocks are falling apart.

Remove Tesla from XLY and the sector looks like Nike. Nike just dropped 14% after missing earnings by nearly 30%.

RH told the same story. It gapped down and fell 22%.

Blake dug into the XLY chart using his monkey bar levels for April. The ETF gapped up into the overbought zone with a ceiling at $111.13. His modified Chaikin money flow indicator still shows net liquidation underneath the surface.

The bounce has no volume behind it. Blake sees short covering, not accumulation.

Amazon faces the same problem. More than half of Amazon’s revenue comes from AWS. Calling it a consumer discretionary stock distorts what the sector is actually telling us about spending.

Blake walked through three bearish setups in tonight’s video that take advantage of the disconnect:

Tesla: Sell the call vertical above $395 for a $1.90 credit on a $5 wide spread. The probability of profit comes in at 64% against a required win rate of 62%, giving a 2% to 3% edge.

Starbucks: Sell the $93/$94 call vertical for $0.45 credit. The required win rate is just 55% against a 64% probability, creating a 9% edge.

Amazon: Sell the call vertical at $220 for $1.50 credit on a $5 wide spread. The setup is fairly priced, but a failure at the $215 target could accelerate the move lower.

Blake favors Tesla and Starbucks for the best reward to risk ratios. All three trades sell premium into a low volume bounce that his indicators say is running on fumes.

This is the perfect time to make sure you’re up to speed on your trading know-how. So I want to ensure you’ve read our free Rebel’s Guide to Trading Options – it covers all the basics of trading options. Like everything we do, the course is in plain English. It’s specially geared toward beginners but all traders will get something out of it. Yours absolutely free, of course – right here…

1. To open an account with tastytrade and enjoy an additional 6 months of TheoTRADE membership, start by clicking the button below..

2. Follow the directions on that page to open a new account.

3. Fund the account with a minimum of $2,000 in the next 30 days and keep open for at least 6 months.

4. IMPORTANT: After the new account is open AND funded email support@theotrade.com so we can verify your new account. Please note it may take us up to one week to verify your account from the time you email us.

5. TheoTrade will then provide you membership access for 6 months!

NEED HELP? LOOKING FOR MORE ADVANCED TRAINING? CALL OUR VIP CONCIERGE TEAM: (623) 244-5657

Warm regards,

Don Kaufman

Disclaimer: Neither TheoTrade or any of its officers, directors, employees, other personnel, representatives, agents or independent contractors is, in such capacities, a licensed financial adviser, registered investment adviser, registered broker-dealer or FINRA|SIPC|NFA-member firm. TheoTrade does not provide investment or financial advice or make investment recommendations. TheoTrade is not in the business of transacting trades, nor does TheoTrade agree to direct your brokerage accounts or give trading advice tailored to your particular situation. Nothing contained in our content constitutes a solicitation, recommendation, promotion, or endorsement of any particular security, other investment product, transaction or investment. Trading Futures, Options on Futures, and retail off-exchange foreign currency transactions involves substantial risk of loss and is not suitable for all investors. You should carefully consider whether trading is suitable for you in light of your circumstances, knowledge, and financial resources. You may lose all or more of your initial investment. Opinions, market data, and recommendations are subject to change at any time. Past Performance is not necessarily indicative of future results.

WARNING: If you UNSUBSCRIBE, you will be removed from ALL email lists, including any paid subscription emails. To opt out of this list only and keep other access, forward this email to support@theotrade.com and say “remove me from this particular email list.” Unsubscribe

TheoTrade 16427 N Scottsdale Rd Suite # 410 Scottsdale, Arizona 85254 United States 1 (800) 256-8876

BSEM Just Released Publication of Its Audited Financial Statements for Fiscal Years 2024 and 2025—Fast-Tracking a High-Profile Nasdaq Uplisting!

BioStem Technologies (OTCQB: BSEM) is rapidly evolving from a niche regenerative medicine innovator into a full-scale MedTech growth story.

The company’s recent acquisition of BioTissue Holdings’ surgical and wound care business for up to $40 million not only broadens its market from physician offices into hospitals and surgical centers but also immediately adds $29 million in revenue and a seasoned national sales team.

Coupled with the proven BioREtain® technology and breakthrough clinical results demonstrating superior wound closure rates, BSEM is now uniquely positioned to address a $300–$350 million total addressable market.

On the financial front, BSEM continues to impress. Q4 revenue topped $10 million with nearly best-in-class gross margins of 97%, and adjusted EBITDA remained solid at $3.4 million despite temporary headwinds. Importantly, the company has published its audited 2024–2025 financials, a key milestone toward its highly anticipated Nasdaq uplisting in 2026.

This move promises increased liquidity, institutional investor interest, and higher valuation potential. With analysts assigning a $25.50 price target, BSEM’s combination of earnings strength, strategic expansion, and regulatory readiness underscores a rare small-cap investment story with multiple growth levers.

Over the past few months, many investors have likely encountered the phenomenon known as the “SaaS Apocalypse.” The term describes a wave of software-as-a-service (SaaS) stocks seeing their share prices plunge amid the rise of new artificial intelligence (AI) tools.

To some extent, markets have been selling off nearly every stock with even a SaaS-adjacent business model. But the impact of AI disruption will not be uniform across every SaaS company.

One tech stock that may fit this description is Datadog (NASDAQ: DDOG). While shares have recovered from recent lows, the stock is still down roughly 10% year-to-date in 2026 and nearly 40% from its 52-week high.

Some investors believe the market may be misreading Datadog’s potential role in an AI-heavy enterprise environment.

Understanding the Drivers Behind the “SaaS Apocalypse”

One of AI’s big promises is that AI agents will be able to act autonomously within enterprise workflows.

The theory: agents will perform tasks that once required expensive SaaS products, allowing companies to significantly cut costs. That prospect is a key reason many incumbent SaaS companies have seen their shares drop sharply.

Some proponents even argue that a single highly capable employee using AI agents could replace the work of several people, reducing headcount and payroll expenses. That is the pitch from AI developers such as OpenAI, Anthropic, and Alphabet (NASDAQ: GOOGL): pay us to deploy your AI agents, and you’ll save money because you’ll need fewer employees.

But AI is still imperfect and can make mistakes, a fact visible even in consumer-facing chatbots and one that can erode trust in AI models. Inside organizations, errors can have bigger consequences—customer impact, revenue leakage, and operational disruption. As a result, businesses are unlikely to adopt AI agents at scale without first building trust and having fast ways to diagnose and fix failures. That’s one area where observability vendors argue they can help.

Outsourcing Thinking: AI Agents Increase the Need for Observability

Datadog sells observability software that collects data from companies’ applications—both internal and customer-facing—so teams can detect problems, identify root causes, and resolve incidents.

Part of the bullish case for Datadog is that while AI agents might reduce labor costs, they also introduce complexity and generate far more data.

A video on Datadog’s AI Agent Monitoring tool illustrates this. The presenter describes a fictional personal finance app called Budget Guru, where a user asks the AI agents to perform a simple task: buy $500 of a stock and remind them of their overdraft fee.

A human could complete that task in a few clicks and do the internal thinking required to execute it. Budget Guru, by contrast, coordinates five separate AI agents to carry out the request—essentially outsourcing the thinking a human would have performed. That orchestration creates a mountain of observable data about how the agents reached their decision.

AI agents produce additional logs, traces, and events that wouldn’t exist if a human handled the same task. As the number of moving parts grows, so do the potential failure points. In that context, AI agents don’t remove the need for monitoring—they raise the bar for it.

This dynamic should increase demand for observability platforms like Datadog, turning disruption risk into opportunity.

Datadog: Impressive Growth, Profitability, and Analyst Support

In its most recent quarter, Datadog’s revenues rose 29% to $953 million. The company also generated free cash flow (FCF) of $291 million, yielding an FCF margin of roughly 31%.

The Rule of 40—which combines growth and profitability to evaluate SaaS firms—is a common benchmark. Scores above 40 are generally considered healthy; Datadog’s score sits near 60.

Wall Street analysts also see upside. The MarketBeat consensus price target is near $180, implying more than 40% upside. Price targets updated after the company’s latest earnings put the average slightly lower, at about $174.

With strong growth, solid profitability, analyst backing, and potential agentic AI tailwinds, there is reason to believe DDOG could withstand—or even benefit from—the so-called “SaaS Apocalypse.”

This email is a paid advertisement sent on behalf of Huge Alerts, a third-party advertiser of MarketBeat. Why did I get this email?.

This message is a paid advertisement for BioStem Technologies Inc. (OTC: BSEM) from Sideways Frequency and Huge Alerts. American Consumer News, LLC dba MarketBeat receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $14,000. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either Sideways Frequency or Huge Alerts. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding BioStem Technologies Inc. (OTC: BSEM) on Huge Alerts’ website for additional information about the relationship between Huge Alerts and BioStem Technologies Inc. (OTC: BSEM).

If you need help with your subscription, please contact our U.S. based support team at contact@marketbeat.com.

You are receiving this email because you signed up for Monument Traders Live. To stop receiving special invitations and offers from Monument Traders Live, please click here. Please note: This will not impact the fulfillment of your subscription in any way.

Please do not reply to this email as it goes to an unmonitored inbox.

Nothing published by Monument Traders Alliance should be considered personalized investment advice. Although our employees may answer your general customer service questions, they are not licensed under securities laws to address your particular investment situation. No communication by our employees to you should be deemed personalized investment advice. We allow the editors of our publications to recommend securities that they own themselves. However, our policy prohibits editors from exiting a personal trade while the recommendation to subscribers is open. In no circumstance may an editor sell a security before subscribers have a fair opportunity to exit. The length of time an editor must wait after subscribers have been advised to exit a play depends on the type of publication. All other employees and agents must wait 24 hours after publication before trading on a recommendation.

Any investments recommended by Monument Traders Alliance should be made only after consulting with your investment advisor and only after reviewing the prospectus or financial statements of the company.

Protected by copyright laws of the United States and international treaties. The information found on this website may only be used pursuant to the membership or subscription agreement and any reproduction, copying or redistribution (electronic or otherwise, including on the world wide web), in whole or in part, is strictly prohibited without the express written permission of Monument Traders Alliance, LLC, 14 West Mount Vernon Place, Baltimore, MD 21201.