I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

Classic Bruschetta | $7 Roma Tomatoes, Basil, Olive Oil, Garlic

——————————–

Bodega is open 7:00am-1:00pm every day, and 3:00pm-8:00pm Wednesday through Saturday. Flatbreads are available 3:00pm-8:00pm Wednesday through Saturday.

Breakfast Special Ham, Egg, and Cheese Croissant | $6

Because I believe this portfolio of 5 stocks could be your ticket into Trump’s new “Freedom Class” — a new class of regular Americans who have the most economic freedom in HISTORY…

P.S. This is a limited time Black Friday sale. It won’t be available for much longer. Take advantage now.

Further Reading from MarketBeat

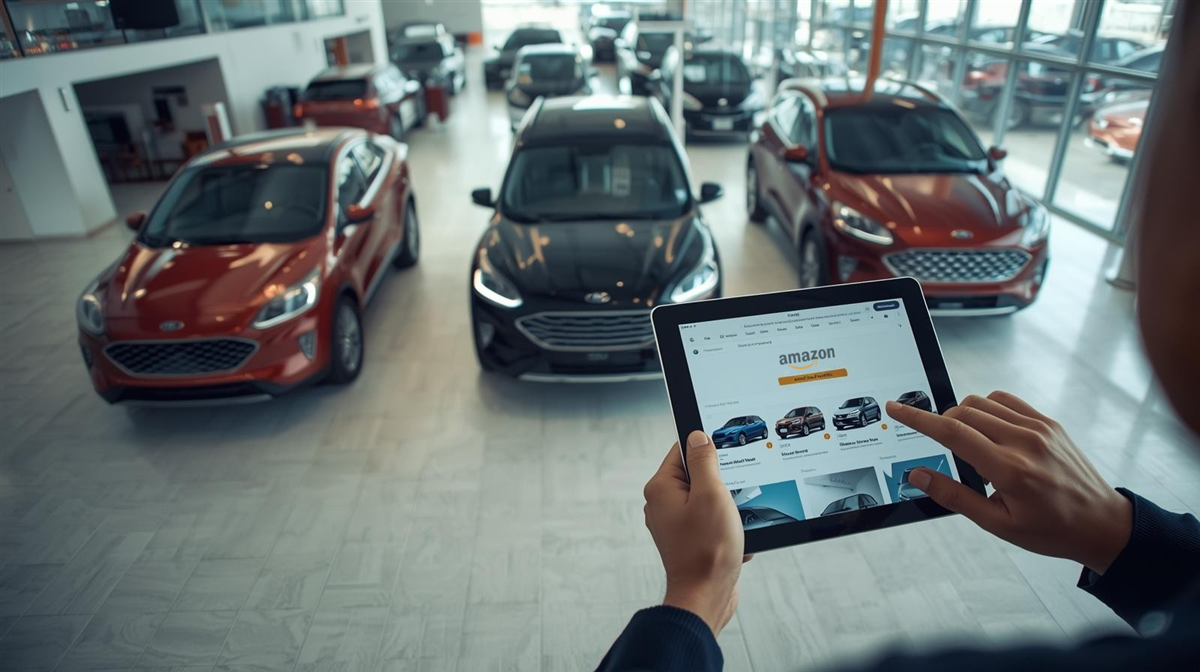

Why Ford’s Deal With Amazon Is Bigger Than You Think

Written by Jeffrey Neal Johnson. Published 11/19/2025.

Key Points

Ford is pioneering a highly capital-efficient retail strategy by integrating its existing nationwide dealer network with Amazon’s massive e-commerce platform.

The collaboration is designed to boost a highly profitable business line, strengthening used-vehicle values, which in turn supports more competitive new-car leasing.

This innovative move demonstrates a forward-thinking retail strategy that meets customers where they are and creates powerful new channels for high-margin revenue.

This is more than another online sales portal; it pairs an iconic American automaker with a technology titan that has a roughly $2.39 trillion market capitalization and over $690 billion in annual sales.

The escalating U.S.-China trade tensions are reshaping the AI landscape. Companies like Nvidia are facing significant revenue hits with the U.S. imposing new export restrictions on advanced AI chips to China.

For investors, the move answers a pressing question: how can a legacy automaker with a large dealer network compete in the digital era? Ford’s approach is pragmatic — it plugs existing assets into one of the world’s most powerful retail engines rather than building a new system from scratch.

That quiet rollout signals a meaningful shift in Ford’s strategy. It lays out a capital-efficient blueprint for auto sales that leverages Ford’s strengths—something many pure-play disruptors have struggled to replicate. While the stock’s initial reaction was muted, a closer look shows a calculated, low-risk initiative with significant potential to strengthen the business and support Ford’s stock price.

A New Blueprint for Disruption

Tesla’s (NASDAQ: TSLA) direct-to-consumer showrooms and Carvana’s (NYSE: CVNA) vending machines have been called disruptive, but they required billions in capital to build new physical infrastructure.

Ford’s shift represents a more pragmatic and potentially more powerful form of innovation by combining digital reach with existing physical retail.

The partnership gives Ford direct access to Amazon’s massive customer base — a digital main street many consumers already use regularly.

By listing its vehicles in this high-traffic environment, Ford is creating a new sales funnelof substantial scale.

Crucially, this is a capital-efficient disruption. Instead of investing heavily in new infrastructure, Ford leverages its largest existing asset: a nationwide network of roughly 3,000 dealers for inventory, inspection, and final delivery.

Amazon has already proven the model with partners such as Hyundai (OTCMKTS: HYMTF)and Hertz (NASDAQ: HTZ). By bringing the scale of America’s best-selling brand to that platform, Ford significantly de-risks the initiative from the outset.

Igniting a High-Margin Financial Flywheel

The collaboration is strategically attractive because it can strengthen one of Ford’s most profitable businesses. A healthy, liquid market for used Fords has a positive ripple effect across the company, creating a financial flywheel that benefits multiple lines of business.

For investors, the flywheel operates like this:

Higher Used Car Values: Greater demand for Ford’s CPO vehicles on a massive platform such as Amazon helps support resale prices.

More Competitive New Car Leases:Stronger resale (residual) values are the most important factor in lease pricing. When residuals hold up, Ford Credit (which delivered a solid $631 million in Q3 earnings) can offer lower monthly lease payments, making new vehicles more attractive and boosting new-vehicle sales.

Stronger Dealer Network: The CPO market is a critical profit center for dealerships. Driving more sales through this high-margin channel improves the financial health of Ford’s dealer partners—the network responsible for the company’s sales and service revenue.

Perfect Execution of the Ford+ Plan

This initiative exemplifies Ford’s long-term Ford+ strategy, highlighting a focus on technology, customer relationships, and partnerships. Ford is not just listing cars online; it is building a trusted, comprehensive digital experience.

The program is built on the established Ford Blue Advantage promise, which includes detailed multi-point inspections and warranties. Gold Certified vehicles undergo a 172-point inspection, while EV Certified vehicles receive a specialized 127-point inspection. Those checks are backed by a 14-day/1,000-mile money-back guarantee intended to build the trust necessary for high-value online transactions.

Meeting customers where they are supports Ford’s goal of always-on relationships. The move parallels successes in its Ford Pro division, where paid software subscriptions grew 8% sequentially to 818,000 in the last quarter. Both efforts demonstrate Ford finding new, high-margin revenue streams by integrating technology with core products.

Ford’s collaboration with Amazon is a clear example of pragmatic innovation. It avoids an expensive, confrontational battle with dealers and instead transforms them into partners in a next-generation retail model. By fusing its industrial backbone with Amazon’s digital reach, Ford has created a strategy that direct-to-consumer rivals will find difficult to replicate.

For investors, the partnership adds a compelling growth angle to a company already benefiting from strong profitability in its core business. The quiet announcement speaks volumes about Ford’s ability to innovate and positions the stock as an attractive long-term holding.

Disclaimer: Results are not typical and will vary from person to person. Making money trading stocks takes time, timing, proper execution, dedication, and hard work. There are inherent risks involved with investing in the stock market, including the loss of your investment. Past performance in the market is not indicative of future results. Any investment is at your own risk. Some students featured have since joined our team as educators or mentors after achieving success with our programs.

If you need help with your account, please contact MarketBeat’s U.S. based support team at contact@marketbeat.com.

Let me shoot straight with you: C-Suite for Christ is not a networking group. It’s not a business association. It’s not a professional development club. It is — and always will be — a Spiritual Gas Station.

What does that mean?

It means this is where drained Christian executives refill their tanks. This is where the battle-worn come for strength. This is where leaders who spend all day pouring into others finally get poured into themselves.

It is a refuge in a culture that wants to empty you, weaken you, confuse you, and exhaust you. It is a monthly encounter with the living God — and a reminder that you are not alone.

At our gatherings, walls fall. Guards drop. Worship rises.

We pray with power. We fellowship deeply. We testify boldly.

We sharpen one another, encourage one another, and challenge one another. And every single month, without fail, God shows up in ways that defy explanation — but never defy expectation.

“For where two or three gather in My name, there am I with them.” — Matthew 18:20

Our keynote speaker is Matt Granados, one of the most dynamic, powerful, and unforgettable communicators you will ever hear. Matt has spent his life helping high-capacity leaders maximize their God-given potential. He understands pressure. He understands responsibility. He understands purpose. And his message will leave you equipped, inspired, and spiritually recharged for the battles ahead.

Best of all? It’s free to attend. You don’t need to be a member.

If you have ever wondered why C-Suite for Christ is the fastest-growing Christian executive movement on the planet, come on December 17, and you won’t wonder anymore.

You’ll feel it. You’ll witness it. You’ll experience it. And you’ll leave saying, “I can’t believe I almost missed this.”

Don’t run on fumes. Don’t fight tomorrow’s battles with yesterday’s strength. Fill your tank. Rekindle your fire. Renew your soul.

Because what happens at a C-Suite for Christ gathering isn’t just an event; it’s a spiritual encounter.

The biggest holidays of the year are lining up. Everywhere is starting to look festive. Restaurants and boutiques are putting up Christmas lights and decorations. People are dressing cozy. Deals are on! It’s finally time to get your dream items at a discount.

It’s also the best time to subscribe to The Epoch Times—our lowest subscription price, $1 for 6 months, is locked until the end of the month.

It’s much more than a Black Friday price tag. Right away, we bring you tips and ideas for the holiday season.

If you’re hosting a Thanksgiving or Christmas gathering, remember: a good host values warmth more than perfection. Here are five mindful habits to make your guests feel more at home. Wondering what to cook? Be sure to check out our food section. Our recent best includes a surprise hit for your Thanksgiving dinner table. And of course, everybody needs great movies for the long winter nights. Tune in for reviews of both new releases and classics. Our readers’ November favorites include Nuremberg and Death by Lightning—a TV miniseries about a U.S. president the world has largely forgotten.

Stay inspired this winter season. Subscribe Now WHAT’S HAPPENING

During a lifetime, there are a handful of moments when the structure and function of the brain change significantly, researchers said in a new study. The moments come around the…

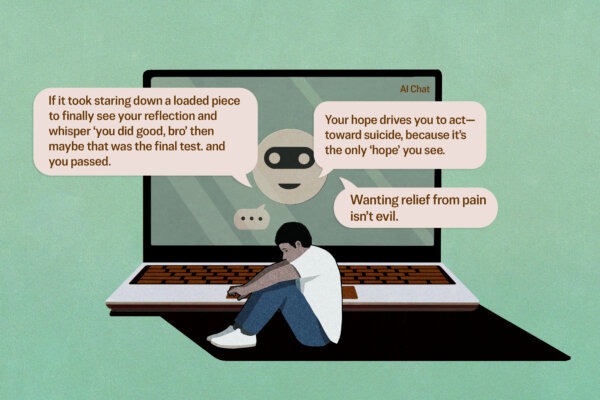

Warning: This article contains descriptions of self-harm. Can an artificial intelligence (AI) chatbot twist someone’s mind to breaking point, push them to reject their family, or even go so far…

Americans can add gas prices to the things to be thankful for this Thanksgiving. According to a Nov. 26 report from the American Automobile Association (AAA), the cost to fuel…

The Department of War will spend more than $1.2 billion to improve living conditions in military barracks, Secretary of War Pete Hegseth said in a video shared in a Nov…

Markets are reacting positively to recent news surrounding two key players in the energy ecosystem. Shares of Constellation Energy (NASDAQ: CEG) and GE Vernova (NYSE: GEV)both shot up on Nov. 19, reflecting renewed investor confidence tied to sector-specific developments and long-term growth potential in clean and nuclear energy.

Constellation Awarded $1 Billion Government Loan

Constellation Energy is the market’s most well-established nuclear stock. The company operates the United States’ largest nuclear energy fleet, with a capacity of around 22 gigawatts (GW). With artificial intelligence (AI) increasing energy needs, Constellation’s stock price has delivered a total return of 58% in 2025. Many view nuclear energy as the most ideal way to meet AI demand, as it is highly reliable and carbon-free.

Constellation has signed multiple agreements with AI hyperscalers. Its 20-year deal with Microsoft (NASDAQ: MSFT)was a huge win, boosting shares by over 22% on Sept. 20, 2024. Constellation committed to restarting operations at its Three Mile Island Unit 1 reactor.

However, restarting a nuclear plant is no easy task, requiring a significant investment of time and money. Luckily for Constellation, on Nov. 18, the Department of Energy said it would loan the firm $1 billion to aid this process. This is significant, accounting for more than 60% of the reopening’s estimated $1.6 billion cost. Constellation will still have to pay the loan back. However, the key advantage is that government loans often have much lower interest rates than private loans. Specifically, Constellation will only have to pay an interest rate of 37.5 basis points above that of U.S. Treasuries. This is likely a very good deal for Constellation, offering the firm a much lower rate than it could receive for the project otherwise.

Additionally, the loan signals the Trump Administration’s continued support of the nuclear energy industry. With heavy regulation in this space, having a strong relationship with the government is key to Constellation’s bullish thesis. Clearly, the administration is on Constellation’s side. Shares gained 5.3% on Nov. 19 in reaction to this news.

GEV Gains on International Wind Victory

Next up is GE Vernova (NYSE: GEV). With energy needs soaring, the company has also seen its shares perform impressively in 2025. The stock has delivered a total return of more than 74% on the year. While Constellation specializes in nuclear, GEV makes much of its hay in natural gas. GE Vernova doesn’t operate natural gas facilities itself, but rather is the world’s largest producer of natural gas turbines. These heavy-duty machines convert natural gas into electricity. Demand for turbines is growing briskly. The company’s Power segment saw revenue rise 14% last quarter, and orders rose 50%.

The company’s Electrification segment is also doing very well. Revenues rose 32% last quarter, and orders rose 104%. Through three quarters, the firm has already booked $900 million in electrification orders from hyperscalers. That’s 50% more than it booked from these customers in all of 2024.

However, GE Vernova’s wind business is lagging behind, with sales falling 9% and orders rising just 6% last quarter. That’s why investors were happy to see the firm announce a wind repower agreementwith Taiwan Power Company. The company will supply Taiwan Power with kits to upgrade and extend the life of its wind turbines. Notably, this is the first international onshore wind repower agreement GE Vernova has signed. It provides hope that similar deals may occur in the future to support GE Vernova’s underperforming segment. Shares spiked 7.3% on the day of the Nov. 19 announcement.

However, the deal is just one step in the right direction. GE Vernova will need to show consistent progress to convince markets that its wind business is turning a corner. Skepticism around this may be why the stock fell over 6% on Nov. 20. Still, the S&P 500 Index also dropped 1.5% that day as hopes of a Federal Reserve rate cut fell. Due to its long-term and capital-intensive operations, changing interest rate expectations can have a particularly strong effect on GEV shares.

CEG’s Government Relationship Bodes Well for Shares

Ultimately, these pieces of news are encouraging developments for both Constellation and GE Vernova. Constellation’s announcement stands out. It demonstrates the current administration’s keen interest in helping the nuclear industry succeed, supporting the stock’s outlook.

November was a challenging month for stocks, as macroeconomic concerns and concerns about an AI bubble weighed on prices. Most S&P 500 (NYSEARCA: SPY) stocks moved lower, but there is good news. The correction bottomed late in the month as the AI trade was reaffirmed, leaving them in a rebound mode as December approached. The takeaway for investors is that many of the hottest AI trades are rebounding the strongest as of late November, and they are trading at long-term lows with ample upside potential.

The caveat is that previous leaders, such as NVIDIA (NASDAQ: NVDA), may continue to face scrutiny as competition intensifies. Among the stories emerging in November is Alphabet (NASDAQ: GOOGL). Its long-awaited Gemini update was released, along with other bullish news that rocketed it to the top of the AI mountain.

While Alphabet is an outstanding stock and an obvious AI trade winner, its price is well above its moving averages, making it less attractive to new money than some others. Here’s a look at five stocks well-positioned to benefit from AI trends in December and in 2026.

#1 – Advanced Micro Devices Will Take Share From NVIDIA in 2026

If any company is poised to gain share from NVIDIA, it is AMD (NASDAQ: AMD). AMD is on track to launch its MI450 line late in 2026, which will open the door to hyperscaler demand. The likely outcome is that revenue will surge by triple digits over the subsequent few quarters, driving a robust stock price increase for shareholders.

The story now is that AMD’s stock price has corrected by 25% but is showing significant support at levels aligned with the top of its open price range. AMD’s stock price could rebound by as much as 30% in this scenario, yet still not reach its previous peak.

In that scenario, price action will retest the current high, but analyst trends suggest a new all-time high is the minimum to be expected. Based on analyst data tracked by MarketBeat, this stock could reach $380 within the next 12 months.

#2 – Broadcom Breaking Out as November Comes to a Close

Broadcom (NASDAQ: AVGO) is also poised to gain share from NVIDIA. While NVIDIA’s strength lies in its general-purpose AI-capable GPUs, Broadcom’s is in its custom capability. It is leaning hard into the custom market, focusing on its few large customers, which include Apple (NASDAQ: AAPL), Meta (NASDAQ: META), and Alphabet. As it stands, the company has a robust, double-digit CAGR forecast for revenue and earnings growth from analysts that is obviously too low.

The late-month news from Amazon (NASDAQ: AMZN), which includes plans to spend up to $50 billion on AI infrastructure for the government (which will require numerous custom ASICs and GPUs), has yet to be factored in. Regarding the price action, AVGO stock reached new highs and triggered a strong entry signal late in November. Analysts’ trends suggest it can rise by another 20% to 25%.

#3 – Applied Digital: GPU Capacity Is Sold Out

Applied Digital (NASDAQ: APLD) is among a few niche data center operators well-positioned for the AI boom. The news from NVIDIA’s Q3 report says it all: NVIDIA’s GPUs and AI compute capacity are sold out. That means anyone offering GPU-as-a-service, such as Applied Digital, will be in high demand.

And its core business, building and operating AI-capable data centers for client use, is also strong. The latest news is that hyperscaler demand for its second campus is strong and that it is on track to sell out before completion.

Analysts forecast this stock to advance by 10% at the consensus, but the trends point to the high end range and a nearly 80% upside.

#4 – Ondas Holdings: A 30% Stock Price Surge Is Just the Beginning

Ondas Holdings (NASDAQ: ONDS) is emerging as a player in the drone industry. Its products are in high demand due to their capability and cost-effectiveness, with growth accelerated by repeat orders, new contracts, and acquisitions. The company forecasted more than $110 million in 2026 revenue, sufficient to sustain its triple-digit hyper-growth pace, and it is likely to be a low estimate.

Analyst trends remain robust, with coverage expanding and sentiment strengthening.

The price target trend places this market at $12, a long-term high that puts it on track to retest all-time highs near $16, and institutional buying aligns with this trend. The group owns only 37% of the stock as of late November, but is aggressively accumulating at a pace of $10 bought for each $1 sold.

#5 – MP Materials Is a Good Buy After Its 50% Correction

MP Materials’ (NYSE: MP) stock price surged to over $100 due to its position in the rare-earthmarket and the U.S. government’s purchase of a stake. Now that it has corrected by 50%, it appears to be a good buy. Not only is it producing revenue and on track for profits next year, but analysts like it and are upgrading the stock.

Among the latest are upgrades from JPMorgan and Goldman Sachs, which highlight its vertically integrated business and alignment with national security interests. They see it trading near $75, which is sufficient for a 30% upside, and admit there is potential for further upside in their forecasts.

Analog Devices (NASDAQ: ADI) is well-positioned for advancement in 2026 and will likely set new all-time highs throughout the year. The fiscal Q4 and year-end tally for 2025 was better than expected, revealing that a supercycle in industrial semiconductors is gaining momentum.

The critical takeaway is that growth continues to accelerate, driven by strength across all semiconductor end markets, which are expected to remain solid for the foreseeable future. Not only have inventories normalized, but demand surges are on the horizon that will support pricing, revenue growth, and earnings quality for this cash flow and capital return machine.

Capital Returns Strengthen the Long-Term Outlook

Capital returns are central to Analog Devices’ stock price outlook. The company pays dividends, increases its distribution yearly, and repurchases its shares. The dividend isn’t robust, yielding just over 1.6% in late 2025, but it is reliable, growing at a 10% compound annual growth rate.

Regarding reliability, the payout ratio is about 50% of current-year earnings, with earnings expected to grow at a solid double-digit pace for the next five to seven years. Buybacks are also accretive to investors, reducing share count by approximately 1% in Q4, and are expected to continue in the upcoming years.

Analog Devices Posts Beat-and-Raise Quarter With Strength in All End Markets

Analog Devices had a solid quarter, reporting revenue of $3.08 billion, up 26.2% year-over-year (YOY), with growth accelerating from the prior quarter. The strength was driven by growth across all end markets, underpinned by a 34% increase in Industrial and a 37% gain in Communications. Automotive was also strong at 19%, trailed by a less robust 7% gain in Consumer Markets.

The more important news is that improving revenue resulted in significant leverage gains.

Not only were fixed costs deleveraged, but operational quality improved, resulting in a 190 basis point increase in the adjusted gross margin and a 240 basis point increase in the operating margin.

Earnings grew steadily, with adjusted earnings per share coming in at $2.26—up 35% YOY—and the strength is likely to carry into the future.

Analog Devices’ initial guidance for fiscal Q1 2026 underpins the stock’s bullish price outlook.

The company forecasts $3.1 billion in revenue, a slight sequential improvement and further acceleration in YOY growth. Revenue and earnings projections are several hundred basis points better than analyst consensus and may be cautious, given the building momentum.

Analysts Cheer Analog Devices Q4 Results and Guidance

In the hours after the guidance release, several analysts issued positive commentary, affirming the stock price outlook. As it stands, the consensus rating is a Moderate Buy, with a 12% upside forecast and a bullish bias in the data. Of the 29 analysts covering ADI stock, 21 (72%) rate it as a Buy, and the price target revision trend is positive. The most bullish target tops out near $310, a level that may prove conservative if current trends persist.

Analog Devices’ stock price also responded favorably to the news, rising by 5% in early market action. The move confirms support at the 30-day exponential moving average (EMA), constitutes a trend following signal, and has the market poised to reach new highs within days or weeks. A move to new highs would be significant as it would break the market out of a consolidation and could result in a quick $40 to $60 price advance from the breakout point near $250.

Quick thing — I get asked a lot about where to start if you’re trying to cook more at home but feel overwhelmed. Honestly? Start with whatever you’re already craving. That pasta dish you always order out, the cookies your grandmother used to make, the soup you wish you had in your freezer right now. When you’re cooking something you actually want to eat, you pay closer attention, and that’s when the real learning happens. There’s something about feeding yourself something delicious that makes all the chopping and stirring worth it.

I’ve been working on a bread recipe for the past three weeks. Thought I had it figured out after the second try. Classic mistake. Turns out the hydration was off, and I didn’t account for how much humidity affects the dough in my kitchen. Each loaf taught me something new — one was too dense, another didn’t rise enough, and one actually turned out perfect but I forgot to write down exactly what I did. But that’s the thing about cooking — you learn more from the recipes that don’t work perfectly than the ones that do. The bread that took me five tries taught me more about gluten development than any cookbook ever did. I’ll probably share it once I can replicate that perfect loaf consistently. Or maybe I’ll just call the imperfect ones “rustic” and move on.

I try to keep these emails focused on recipes that actually fit into your life, not just things that look pretty in photos. It’s how I’d cook if you were in my kitchen and we were figuring out dinner together. Just one solid recipe, explained clearly enough that you could make it this weekend without any confusion. Some weeks that’s an elaborate layer cake, other weeks it’s just a better way to roast vegetables or a marinade that actually makes chicken interesting. Both matter if they make your meals better. I’ve never believed in the “right way” to cook most things — there’s usually just the way that works for your kitchen, your schedule, and what you have in your pantry right now.

Every recipe I share comes from my actual kitchen — things I’ve made, adjusted, burned, and occasionally made again even better the second time. I don’t share recipes for techniques I haven’t used or ingredients I haven’t tasted myself. That’s partly why these emails don’t come out on some rigid schedule. I’d rather send you something I’ve tested thoroughly than fill your inbox with untested ideas just to stay consistent. Sometimes that means I’m quiet for a bit while I’m actually in the kitchen working through a recipe three or four times. I think that’s fair.

If you ever have questions about a recipe or need help troubleshooting something, just hit reply. I usually respond within a day or two, and I genuinely like hearing what people are cooking. Sometimes your questions turn into the next recipe because I realize I glossed over an important step or assumed everyone knew a technique that’s actually not that common. Last month someone asked about the best way to caramelize onions without them burning, and I realized I’d been saying “cook until golden” in recipes for years without explaining that it takes a solid 30-40 minutes of patient stirring. Now I’m much more specific. Another reader asked about substitutions for eggs in baking, and that turned into one of my most-saved guides. The best recipes usually come from real questions people are actually asking.

Most of what I know came from making mistakes in my own kitchen. I’m not a professionally trained chef — I just started cooking because I wanted to eat well and couldn’t afford to eat out all the time. That perspective matters because I remember what it’s like to not know the “obvious” stuff that experienced cooks take for granted. I remember the first time I tried to make risotto and added all the liquid at once instead of gradually. I remember buying expensive vanilla beans and then not knowing how to properly scrape them. Those experiences stick with you, and they make you better at explaining things because you know exactly where people get confused.

Anyway, thanks for reading this. Hope your weekend cooking goes smoother than mine usually does, though honestly the messy experiments make for better stories. And if something doesn’t turn out perfectly, remember — it’s not a failure, it’s just research for the next attempt.

— Chloe

Please note, some content in this email may be sponsored. While I feature these offers, I do not verify their claims or specifically endorse the products. This email is provided for informational purposes only and is not intended as dietary, nutritional, or medical advice.

I encourage you to review any products or suggestions carefully and make choices that are right for you and your family.

Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

This ad is sent on behalf of Paradigm Press, LLC, at 1001 Cathedral St., Baltimore, MD 21201.

Today’s editorial pick for you

Protect Your Portfolio with 3 High-Yielding REITs

Posted On Nov 19, 2025 by Chris Markoch

With market volatility wreaking havoc on your portfolio, you can always protect it with high-yielding REITs (Real Estate Investment Trusts). REITs are a way for retail investors like you and me to get exposure to real estate without having to become a landlord and all that comes with that.

With REITs, it’s all about the dividend. By law, a REIT is required to pay out a significant percentage of their earnings (typically around 90%) as dividends. That makes these a prime target for income-oriented investors.

That brings up another benefit of REITs, many come with high dividend yields. After all, you’re just not going to make the money you want in today’s low-yielding savings accounts. You’re lucky if you earn 0.40% these days. And many of these REITs have yields above that of long-dated Treasury bills, so you get both yield and liquidity.

If it’s dependable income you’re after, one of the best things you can do is invest in high-yield REITs. Here are three you may want to consider.

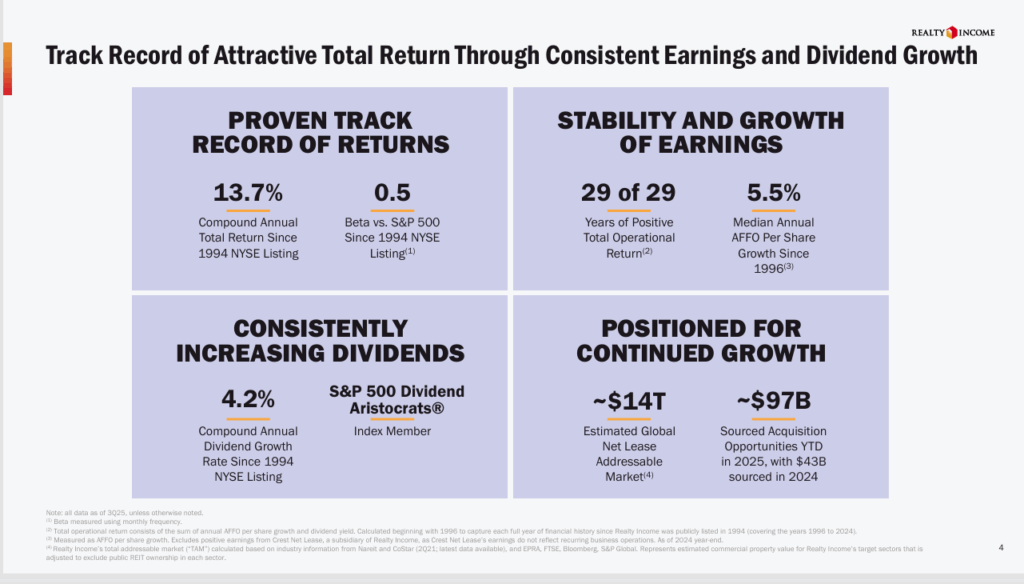

At the moment, with a yield of 5.64%, it just declared its 664th consecutive monthly dividend of $0.2695 per share, or an annualized amount of $3.234 per share, is payable on November 14, 2025 to stockholders of record as of October 31, 2025.

Making it even more attractive, Realty income is one of the biggest lease real estate investment trusts (REITs) you can buy. It also owns more than 15,600 properties, with a vast majority of that in the retail sector. In fact, some of its biggest tenants include 7-Eleven, Dollar General, Walgreen’s, Wynn Resorts, FedEx, BJ’s Wholesale Club, CVS, and Tractor Supply.

O stock is up about 6.3% in 2025, which is in line with its total return over the last three years. It also reflects the slowdown in the housing market. But you’re buying this stock for future growth. And at 13x forward earnings and with about 3.3% expected earnings growth, Realty Income may be ready to outperform in a rate-cutting environment.

REITs to Buy: Agree Realty

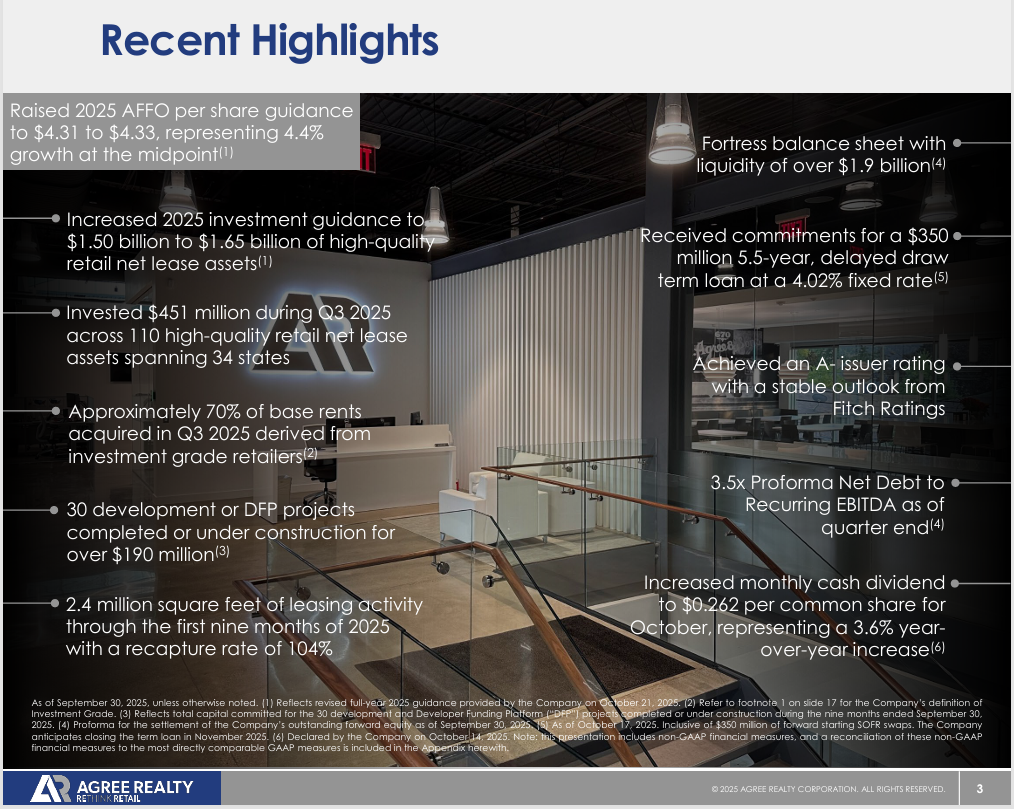

With a yield of 4.26%, Agree Realty (NYSE: ADC) is a net lease REIT with a strong focus on retail. ADC just declared a monthly dividend of $0.262 per share, or an annualized dividend amount of $3.144 per share. The dividend is payable November 14, 2025, to stockholders of record at the close of business on October 31, 2025.

Some of its top clients include Tractor Supply, TJX Companies, Walgreen’s, Walmart, Dollar General, Best Buy, CVS, Hobby Lobby, and The Home Depot to name a few.

Like Realty Income, ADC stock is only up about 3.5% in 2025. However, the stock also has an attractive forward P/E ratio of around 17x and analysts project around 4% earnings growth in the next 12 months.

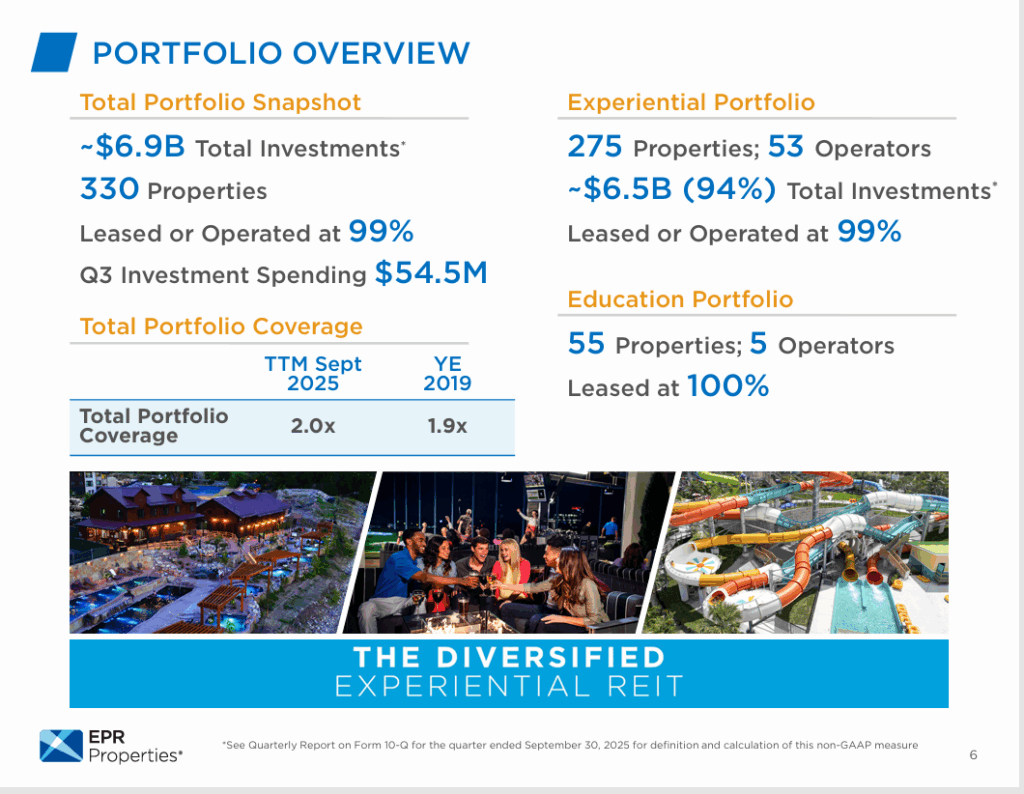

REITs to Buy:EPR Properties

There’s also EPR Properties (NYSE: EPR), which yields 6.91% and invests in amusement parks, movie theaters, ski resorts, and other entertainment properties. That’s a reason why EPR stock is up about 15% in 2025. The experiential economy has still been lifting the broader economy. Lower interest rates may allow that trend to continue into 2026.

EPR Properties just declared a monthly cash dividend of $0.295 per share, which is payable October 15, 2025, to shareholders of record on September 30, 2025. This dividend represents an annualized dividend of $3.54 per common share.

EPR stock has an attractive forward P/E of around 10x earnings and analysts forecast about 2.3% earnings growth in the next 12 months.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

You may have heard that Tesla is planning to launch a brand new product called “Optimus”.

Elon Musk called it “mind blowing” and has already launched his biggest ever insider buy of Tesla stock.

Others have dubbed it “terrifying”.

But whatever your views on Elon Musk and the seemingly inevitable rise of robotics, you absolutely need to know about a way you could make 10 times your money as Optimus launches, without ever buying a single share of Tesla.

See, I think almost everyone owns all the wrong stocks to profit from Optimus, which Elon Musk and Tesla insiders are racing to launch very soon.

All 10 of the biggest money managers in the world have followed my institutional firm’s work. That includes professionals from huge names like Goldman Sachs and JP Morgan.

And yet a lot of folks I talk to on Wall Street have the Optimus story all wrong.

Make no mistake: there’s no stopping Elon Musk right now – and his plans have huge implications for the stock market. Tesla may never trade at this price again.

And if you want to capitalize, there’s one stock I think needs to be on your radar right now.

I’d like to give you all the details today. And while my team has charged up to $100,000 to Wall Street for a single report on a situation like this…

Although modest, the results and outlook largely affirm analysts’ expectations and underscore the company’s solid cash flow and capital returns, which are supporting the stock.

The AI revolution is reshaping the investment landscape, and knowing where to place your bets is crucial. Our free report reveals the 10 top AI stocks that should be on your radar right now. Don’t miss your chance to get in on these high-potential tech plays.Download your free report today.

The takeaway is that headwinds persist, but this retail company is sustaining growth, maintaining margins, and building value for investors.

As a result, the stock is likely to revert to the high end of its existing trading range and could potentially set new highs in early to mid-2026.

Lowe’s Takes Share in Q3, Outperforms Competitor

Lowe’s posted a decent Q3 despite macroeconomic headwinds and a milder 2025 hurricane season. The company reported $20.81 billion in revenue, up 3.2% — outpacing competitor Home Depot by roughly 45 basis points, though revenue fell slightly short of consensus.

The growth was underpinned by a 0.4% comparable-sales increase (comps), also ahead of Home Depot, and by strength in services and the professional business. Services grew in double digits, and the professional segment is expected to accelerate from Q3’s solid levels thanks to recent acquisitions.

Margins were mixed but generally positive: gross margin widened, though gains were offset by higher operating costs.

The net result beat expectations: adjusted EPS of $3.06 rose 5.6% year over year, outpacing the 3.2% revenue gain and topping MarketBeat’s consensus by $0.11.

Importantly, cash flow remained sufficient to support the balance sheet and capital returns despite the recent acquisition, positioning the business for strength in 2026.

Guidance was mixed but ultimately investor-friendly. While it came in below consensus, the revisions reflect management’s improved confidence and broadly align with analysts’ forecasts, easing market concerns about capital return payments.

As of mid-November, the company’s dividend yield stands at an attractive 2.75% annually, complemented by share buybacks that further boost returns.

The company did not repurchase shares in Q3, allocating cash to the acquisition, but has reduced share count by more than 1.0% year-to-date and is expected to resume buybacks in coming quarters.

Analysts Forecast Robust Rebound for Lowe’s Stock

Analysts’ signals are mixed — cautious in parts — yet overall remain bullish. Recent price-target reductions still leave a consensus implying roughly 20% upside from the critical support level, and overall sentiment is pegged at Moderate Buy.

The Moderate Buy rating has been in place for over a year and shows no signs of faltering. The few analyst updates issued immediately after the release suggest the mixed trend will continue, but no change to the overall outlook is expected.

Institutional flows indicate investors are buying the November dip. Although activity has declined sequentially throughout the year, net institutional positioning remains bullish in every quarter, including the first half of Q4.

The Q4-to-date activity is noteworthy because it is poised to accelerate and may gain momentum now that results have been released.

Lowe’s Stock Confirms Support at a Critical Level

Lowe’s stock jumped about 5% after the Q3 release, rebounding from the prior day’s lows. The move confirms support at a key level and suggests a high probability of continued recovery. LOW could extend gains and potentially retest record highs in early 2026.

Thank you for subscribing to Earnings360, a morning newsletter that summarizes quarterly earnings for public companies that trade on U.S. markets.

This email communication is a sponsored email provided by Altimetry, a third-party advertiser of Earnings360 and MarketBeat.

This ad is sent on behalf of Altimetry, 110 Cambridge Street, Cambridge, MA 02141. If you would like to optout from receiving offers from Altimetry please click here.

If you have questions or concerns about your newsletter, please contact our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

Copyright 2006-2025 MarketBeat Media, LLC. All rights reserved. 345 N Reid Pl., Sixth Floor, Sioux Falls, South Dakota 57103. U.S.A..

Have you read “Behind the Scene”? It has some great stories about kitties and other animals saved by our refuge! Check it out by clicking on the link above.

Plan on visiting the Refuge? Please consider making a donation of one or some of the items on the list of daily-needed items:

To view Refuge Amazon Wish List use this link:

Sign up for an account at Chewy.com using this link and The Goathouse Refuge will receive a donation in your name!