I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

Editor’s Note: Former tech executive and angel investor Jeff Brown — picked Bitcoin before it jumped as high as 52,400%, Tesla before it jumped as high as 2,150%, and Nvidia before it jumped as high as 32,000%. Today, he’ll show you how to claim a stake in Elon Musk’s upcoming IPO – BEFORE the company goes public. Click here to see the details or read more below.

Dear Classic Car Enthusiasts, Collectors and Followers,

The 2026 classic car market appears to be in a very different place compared to just a few years ago. In short, it’s no longer booming. Instead, it may be cooling, self-correcting, and becoming more selective and layered.

A current snapshot of the market may help put things into perspective.

If you’re buying: it’s very much a buyer’s market—and one of the best windows in years.

Around 70/80% of classic car values have either fallen or remained flat. Supply now outstrips demand, discouraging competition, which makes negotiation – and, crucially, negotiating skill – more important than ever.

Sellers are becoming more realistic, and cars are sitting on the market for longer. The upside? This market correction (not a crash) means better value and greater choice.

If you’re selling: it can be challenging (unless you’re in the right segment). Many classic cars have declined in value and are harder to sell. Buyers are cautious, and auction results are softer.

The market is increasingly split: top-end cars continue to perform strongly, while the mid-range sector remains weaker.

The auction scene has shifted again, with American markets leading the field and achieving strong results – particularly with Ferraris and Porsches.

By comparison, British classics have reached rock-bottom across the board, and sales are struggling across the pond.

We all know Jaguars are not looking up – yet. Perception isn’t helped by poor auction results, which often receive the wrong kind of publicity… frequently from those who never attend auctions, handle the cars, or truly understand them.

The number of cars entering auctions each month has increased significantly – not necessarily in absolute value, but due to a lack of buyers. Values are being driven down, a trend often inaccurately reported as simply “poor results.”

At the same time, the number of so-called experts reporting on auction results and market conditions has grown, with some offering inconsistent interpretations – raising questions about the depth of real expertise.

We’re seeing a growing number of enquiries from owners considering selling their classics, and it’s encouraging to see people taking a sensible approach, asking questions and exploring different options. That said, many are still anchored to past values, and the reality is that the market has changed, however unfair that may seem.

On a positive note, shows continue to attract strong attendance, with increasingly professional displays. Let’s hope this momentum continues in the months ahead.

If you are considering selling your classic or searching for something special, we are always here to assist.

The “Prince of Wales” (often shortened PoW) specification refers to a special, more discreet version of the Vantage Volante — combining the powerful Vantage engine with a more understated body style, closer to the standard Volante rather than the aggressive “X-Pack” styling of the regular Vantage Volante.

Of those, 22 were right-hand drive (i.e. for the UK/home market) three of these were converted by Aston Martin Works Service to left hand drive in period, this being one of the three.

The jewel in the Newport Pagnel crown, one of the most desirable Aston Martin V8 model cars elegance and refine, the ultimate V8 for the era.

Just two owners from new and an excellent example.Read More

With only 20 of the 50 production cars built being left hand drive and one of only eight with automatic transmission, makes this a very desirable collectors motorcar and one, which can be driven with a smile.

We have known this car from new, well documented and European registered.Read More

This stunning 1955 Aston Martin DB2/4 was purchased in 2016 as a “barn find”, it had been sitting under a tarpaulin for over 40years in a heated workshop!

The car was subsequently dismantled and subject to a complete nut and bolt restoration. Quite outstanding example. Eligible for the Mille MigliaRead More

The car today has been totally stripped and is in the process of a total nut and bolt rebuild to the exact original specification, including all the very special extras the car was supplied with.

One very special and unique motor car. When ONLY the best will do.Read More

This beautiful 1958 Aston Martin DB MK III, is one of 84 cars made and even less in left hand drive format as this one is. Finished in dark blue paint with black mohair hood and black leather trim, just outstanding car.

Supplied new by US Importer H.S Inskip in USA and sold new to The Weathermatic Corporation of Long Island City, New York, USARead More

This outstanding Aston Martin DB4 The car has been subject to a total body off restoration with detailed photographs of the work carried out.

The engine was rebuilt by Oselli and gearbox and axle overhauled by BPA Engineering. The attention to details on the restoration is just amazing, it is just a work of art, faultless in every way.Read More

This Aston Martin DB4 Series 4 is quite special and totally unique, its NOT just a standard DB4 Series 4, No its a well constructed and thought about car with so many nice to have extras, which enhance the car so well in so many ways.

A total one off at a realistic asking price.Read More

This 1969 Aston Martin DB6 was one of the last batch of cars built before the DB6 MKII was launched. Sold new by HR Owen in London and order in Silver Birch with Black trim.

Purchased by the current owner in 2006 and has been subject to a full stage by stage refurbishment with the following work carried out by known Aston Martin specialist:Read More

One of 29 right hand drive cars produced . This was the penultimate car produced, so quite unique.

The car has a lovely history file and has been very well looked after using known people to take care of this special motor car.

The exterior colour is now Pearl Black with the original Black leather trim and a new Black Mohair hood and the car also has a full tonneau cover.Read More

Traditional Aston Martin British Racing Green with Tan Leather interior, black Mohair hood, this manual left hand drive car is so stylish and a cool motor car.Read More

The Aston Martin Works Demonstrator Minky January 1992 the new cars sales was in the depths of slow down, so the Aston Martin Service and Restoration department launched the Aston martin Virage 6.3 conversion. The demonstration vehicle known as Minky was the most published Aston Martin of the era, making the front page of many magazines.Read More

Following the purchase the current owner underwent a rigorous and in-depth cleaning of the whole car uncovering any part of the nook and cranny which required cleaning, rust treatment or replacing.

This car was going to win concours events, NOT just any old concours the target was Elite, the very best.Read More

This low milage Manual car has an interesting history with known owners one being Alan White drummer of Oasis, the documented history file confirms the low milage and perfect all round condition.

The manual transmission and the rumble of the sports exhaust really makes the car a unique drivers car a true GT.Read More

This concours winning car is probably the BEST prepared Vanquish and is fitted with the SDP (Sports Dynamics Pac) which went on to be the Vanquish S without the super light weight wheels. The car started life as the company demonstrator being the car used for PR and customer demonstration use. The car is packed with extras others were not a-custom to, with the Linn music system, pop up dash screen and so much more.Click Here

This factory all matching numbers Left Hand Drive DBS Vantage with manual transmission and A/C is the best of the best, restored by all the right people to perfection.

The car has a full main dealer service history and four known previous owners.

The paintwork is exceptional, no damage or defects, the wheels and tyres are spotless, the roof is in very good order and the interior trim in very good condition.Click Here

This Aston Martin Virage Volante was one of only two left hand drive cars to have the full 6.3 conversion and the only car with manual transmission form. Outstanding condition and drives so well. Rare car with so much attitude and drives so well. Sounds amazing.Click Here

This very fine example finished in its original Windsor Red exterior paint with Magnolia leather trim with dark red piping and Beige Wilton carpets piped dark Red.

Left Hand Drive EFI with ONLY 22,000 kms and well documented, supporting the outstanding condition.

Over his long career, Buffett invested through Vietnam… through the Gulf War… through the war in Afghanistan… during the conflict with Iraq… and countless other conflicts we’ve been involved in across the globe.

Throughout this period… Buffett stuck to one fundamental strategy above all others…

You see, after analyzing over 3,000 stocks and 40,000 data points, our institutional research – which members of all the top 10 money managers in the world pay thousands to access – suggests a specific group of “unbeatable advantage” stocks could be set to soar…

And if you want to avoid any more nasty surprises thanks to the turmoil playing out in the markets right now…

…and potentially add a whole range of “unbeatable advantage” stocks to your portfolio that could be set to double in the coming weeks and months.

The smart move is to get as close as possible to Buffett’s oldest and most profitable strategy.

P.S. I lay everything out right here – including the name and ticker of the one stock you should buy today.

This ad is sent on behalf of Altimetry, 110 Cambridge Street, Cambridge, MA 02141. If you would like to optout from receiving offers from Altimetry please click here .Stockguru LLC (dba InvestingDistrict), 2563 cherry hill ln, Hermitage, PA 16148, United StatesYou may unsubscribe or change your contact details at any time.

In 2025, Karman (NYSE: KRMN) was among the hottest stocks in the market. Shares ended the year near $73, rising more than 300% from their IPO price of $22. The new year has been more of a mixed bag. The stock remains up more than 15% in 2026; however, it is down around 25% from its all-time high, reached in January.

The reaction after Karman’s latest earnings report exacerbated this fall, with shares tanking nearly 14% in one day.

Karman is a supplier of mission-critical components for rapidly growing defense technologies. The company’s revenue growth in 2025 was among the highest in its industry. The firm also sported impressive margins.

Amid this backdrop, is there an opportunity in shares of Karman? Let’s dive into the firm’s latest report to assess this question.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

Karman Posts Top-End Growth with Strength Across Segments

In its fiscal Q4 2025, Karman posted revenue of $134.5 million, or a growth rate of just over 47%. This figure moderately surpassed estimates. For the full year, revenue grew by almost 37% to $471.5 million. Within a group of over 20 U.S. aerospace and defense stocks with market capitalizations above $10 billion, Karman’s full-year growth rate was the second highest. Only Rocket Lab’s (NASDAQ: RKLB) growth of 38% was greater.

Within this, all of Karman’s segments exhibited impressive growth during the quarter.

Meanwhile, the firm posted a full-year gross margin of 40% and an operating margin of 15.5%. These figures were in the top five and top 10, respectively, within the aforementioned group. The company’s operating margin also sits in notable contrast to Rocket Lab’s, which was -38% in 2025.

Adjusted earnings per share (EPS) nearly quadrupled year over year (YOY) from 3 cents to 11 cents. Full-year adjusted EPS nearly tripled from 13 cents in 2024 to 37 cents in 2025. The firm’s 11-cent figure in Q4 was in line with expectations.

Adjusted EBITDA margin is one of the company’s preferred profitability metrics. The figure rose 230 basis points YOY in Q4 to 31.2% and rose 10 basis points YOY in 2025 to 30.8%.

Robust Long-Term Defense Spending Is Vital to KRMN’s Outlook

Undoubtedly, Karman is putting up fantastic results, with top-of-the-industry growth and profit margins that exceed companies many times its size. Still, the stock trades at a forward price-to-earnings ratio of approximately 130x. This shows that the market is pricing in several years of high growth and long-term margin expansion.

Clearly, the company is benefiting from robust demand across key defense verticals. However, the key question is how many years this can last. The company’s $800 million backlog provides strong near-term visibility, being 1.7 times higher than its 2025 revenue. However, it does not provide visibility over five to 10 years.

Karman has shown that its products are competitive, evidenced by the combination of its strong growth and sizable margins. However, a highly bullish outlook on long-term defense spending is ultimately key to taking a bullish stance on Karman at its current price.

So, what is Karman saying on this front, and what do external developments indicate?

Why is the White House suddenly building a new “Fort Knox?” Hidden inside this fortress lies a critical new resource Moody’s calls “the new oil.” Demand is doubling every 6 months, and Fox News is calling it the “new arms race.” On April 20, a major event could ignite a handful of under-the-radar stocks, setting off what could be biggest commodity boom in history.Click here for all the details.

Karman Touts “Generational” Demand Increase as Conflicts Wage

Karman forecasts an even better year ahead in 2026, projecting midpoint revenue growth of 53%. The company expects its adjusted EBITDA margin to contract moderately to around 29.5% due to recent acquisitions.

The company believes it is in the midst of a “generational” increase in demand across key products. This includes missiles, interceptors, hypersonics, unmanned aerial systems, maritime defense, and space and launch. Karman says, “This is a demand environment that we expect to persist through the end of the decade and beyond.” The company also believes that additional growth vectors like the “Golden Dome” will materialize over time.

Conflicts in Ukraine and the Middle East show that tensions around the world are ratcheting up. The White House is seeking $200 billion in additional funding for the conflict in Iran. Pending congressional approval, this would be around a 24% increase versus the Pentagon’s previously approved $838.7 billion annual budget.

Furthermore, European NATO countries have committed to greatly increasing their defense spending as a percentage of gross domestic product. This rearmament effort remains in its relatively early stages. A potential conflict between the United States and China over Taiwan is another factor to consider.

These dynamics work strongly in Karman’s favor. Nonetheless, Karman remains a relatively risky bet due to its valuation. The stock’s large post-earnings drop, despite Karman’s strong results and guidance, highlights this.

Still, analysts continue to take a bullish stance on the stock. The MarketBeat consensus price target near $117 implies over 30% upside in shares. Two targets updated after the company’s earnings report are even more optimistic, averaging $126. This figure suggests the stock could rise by over 40%.

This is a courtesy notice regarding potential changes that may affect your 2026 tax liability.

Many taxpayers unknowingly trigger higher bills due to retirement-account decisions made too late.

Reviewing your options now may help reduce future obligations and avoid surprises.

Get the free guide hereReagan Gold Group does not provide financial, legal, or tax advice. This material is for educational purposes only and should not be considered investment advice. All investments carry risk, including loss of principal. Past performance is not indicative of future results. Please consult a licensed financial advisor before making investment decisions.

If you no longer wish to receive promotional messages from this advertiser, please unsubscribe here. Or write to: 2029 Century Park E Suite 400, Los Angeles, CA 90067

Our research analysts are set to release their next stock idea tomorrow morning just before 12:00 PM Eastern.

It will be sent first to investors that sign up to receive the Early Bird Stock of the Day via text, and the next morning to email newsletter subscribers.

Don’t miss your chance to be the first to see our next stock pick. Our last pick was quite popular with subscribers.

This is a free service from The Early Bird and MarketBeat. If you want to take advantage of this unique buying opportunity, simply click the link below to add yourself to our distribution list.

Analyst Optimism: MarketBeat’s Most Upgraded Stocks of 2026

Submitted by Leo Miller. Article Published: 3/26/2026.

Key Points

A few months into 2026, Wall Streetanalysts are loving these three stocks.

All have received more than 30 upgrades during the year.

This includes two names that have benefited significantly from artificial intelligence tailwinds, and a giant shipping stock persisting through headwinds.

With nearly three months of 2026 behind us, the stock market has been anything but predictable. Many software stocks have been hammered, and every name in the Magnificent Seven is in the red. Overall, the S&P 500 Index is down more than 3% and recently slipped below its 200-day simple moving average.

Still, there are pockets of strength. Some companies are building on breakout 2025 performances, while others are staging significant recoveries. And although the market hasn’t fully rewarded it, analysts have grown increasingly bullish on one of the top Magnificent Seven names.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

Earlier in 2026, MarketBeat identified three stocks among the most upgraded by Wall Street analysts, with price targets implying substantial upside.

Micron Takes Crown as Most Upgraded Stock of 2026

Leading the list is memory chip makerMicron Technology (NASDAQ: MU), which has received the most analyst upgrades so far. MarketBeat has tracked 40 upgrades on MU, a figure that reflects the stock’s strong start to 2026. Year to date, Micron is up more than 30%, adding to its roughly 240% gain in 2025.

Among analysts who updated targets following the report, the average target rose to roughly $548, suggesting more than 40% upside. Still, investors should note MU also received a couple of Hold (or equivalent) ratings after the report.

Micron’s rally has been driven in part by a shortage of a key component used in AI data centers: high-bandwidth memory (HBM). Micron is one of just three suppliers—along with Korean firms Samsung Electronics (OTCMKTS: SSNLF) and SK Hynix—that produce HBM. All three are effectively sold out of HBM capacity for 2026, giving them significant pricing power. That dynamic helped Micron’s revenue grow about 196% year over year in the last quarter, while gross margin rose roughly 1,800 basis points.

Historic Market Share Gains Help Lead FDX Shares and Price Targets Higher

A somewhat surprising entrant on this list is FedEx (NYSE: FDX), which has garnered 35 upgrades and ranks as MarketBeat’s second most upgraded stock of 2026. In 2025, FedEx underperformed the S&P 500—delivering a total return of about 5% versus the index’s nearly 18% gain. That underperformance was partly tied to tariffs and other headwinds to global trade; in April 2025, amid President Trump’s “Liberation Day” announcement, FedEx shares briefly fell as much as 31%.

Since then, the stock has staged a solid recovery. FedEx returned 28% in the second half of 2025 and is up more than 20% so far in 2026, helped by market-share gains in the U.S. and effective cost management. In its latest quarter, the company said it achieved its “strongest profitable market share growth” in over 20 years.

The MarketBeat consensus price target for FedEx sits near $394, implying just over 10% upside. The average of targets updated after the earnings release is somewhat higher at $411, nearer to 15% upside. Among roughly a dozen updated targets, about a quarter of analysts assigned a Hold (or equivalent) rating, and Morgan Stanley placed an Underweight on the stock.

Alphabet delivered an impressive 66% total return in 2025, driven by growth across key businesses and enthusiasm for its Gemini AI model. The MarketBeat consensus price target is roughly $367, implying more than 20% upside.

There has been a notable disconnect between the stock and analyst targets since Alphabet’s last earnings report. Despite beating estimates on both revenue and adjusted EPS, the share price is down over 10%. One reason: Alphabet’s 2026 capital expenditure guidance of $175 billion to $185 billion came in well above expectations.

Still, analysts have become more bullish. Among those issuing targets after the report, the average rose to about $383, suggesting potential upside of more than 30%. Of 32 updated targets, only four were Hold (or equivalent) while 28 were Buy (or equivalent).

MU, FDX, and GOOGL Are Winning the Hearts of Analysts

Micron, FedEx, and Alphabet are clearly attracting significant analyst support. That’s a positive signal, but price targets are not guarantees — they reflect analysts’ 12-month views and can change quickly with new information. Investors should use them as one input among many when evaluating potential trades or longer-term investments.

Exclusive Content

Winnebago’s Q2 Earnings Show It Navigating a Tough Landscape

Author: Chris Markoch. Publication Date: 3/26/2026.

Key Points

Winnebago’s Q2 FY2026 earnings beat expectations, but revenue growth driven by pricing rather than volume is raising sustainability concerns.

Macroeconomic uncertainty, including interest rates and geopolitical tensions, is weighing on consumer confidence ahead of peak RV season.

Analysts remain bullish on WGO stock with over 20% upside, but increased institutional selling signals caution in the near term.

Winnebago Industries Inc. (NYSE: WGO) is one of the leading recreational vehicle (RV) manufacturers in the country. Beyond market share, the company’s March 25 earnings report showed solid results but underscored that revenue gains are being driven more by price increases than by higher unit volumes.

Investors were skeptical of that dynamic. After the Q2 2026 earnings report, WGO shares fell nearly 7% by the close.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

The results did beat expectations on both the top and bottom lines. Revenue of $657.4 million topped analyst estimates of $628 million and rose almost 6% from $620.2 million in the same quarter of 2025. Adjusted earnings per share of $0.27 met expectations and were 42% higher year over year.

Those numbers are notable given this is historically a light quarter outside peak RV season. Here’s what current shareholders and prospective investors can take away from the Q2 report.

Earnings Highlight Consumer Uncertainty Heading Into RV Season

Winnebago isn’t a broad economic bellwether, but as a consumer discretionary company its results offer insight into consumer confidence.

Heading into peak RV season, many consumers remain cautious about making large purchases. According to the Conference Board’s Consumer Confidence Index, measures “remained well below the four-year peak achieved in November 2024.”

Earlier in the year, sentiment had been improving on the back of lower gas prices, larger tax refunds and easing rates—factors that typically boost consumer willingness to spend. But as Q1 closed, new uncertainties emerged.

Geopolitical tensions involving the United States, Israel and Iran could keep oil prices elevated, which would blunt some of the benefit of tax refunds. At the same time, the direction of interest rates remains uncertain, and no analyst can say with certainty where rates will be later this year.

That said, Winnebago appears to be navigating a difficult backdrop reasonably well and could benefit if the economy grows steadily. Still, the current geopolitical and macroeconomic uncertainties make short-term forecasting challenging.

Winnebago Balances Slower Growth With Strong Financial Discipline

That growth, however, is modest compared with the surge in 2020–2021 at the height of the pandemic, when RV ownership experienced a unique boom. RVs are generally one-time purchases and the market has since become more saturated, but the continued YOY gains show that demand persists.

What Winnebago can control is financial discipline. While the RV maker reported less cash than a year earlier, it also reduced net leverage. The company is maintaining shareholder-friendly policies: the board kept the quarterly dividend at $0.35 per share, which equates to $1.40 annually and is supported by next year’s earnings projections. Winnebago also has about $180 million remaining on its stock buyback authorization, which should help bolster investor confidence.

WGO Stock Outlook Hinges on Analyst Optimism vs. Institutional Selling

Winnebago’s Q2 report hasn’t resolved the tension between analyst optimism and institutional selling. The MarketBeat analyst consensus pegs the one-year price target at $42.80, implying potential upside of more than 30% at the time of writing. That’s down from roughly $60 a year ago but has been steady for about nine months. Of 11 analysts covering the stock, the consensus rating is Hold, with four recommending Buy.

Meanwhile, institutional investors have been net sellers over the past 12 months: roughly $1.45 billion in outflows versus about $275 million in inflows. That pace of selling is the highest among institutions since Q1 2024 and has picked up over the last two quarters.

The volume isn’t extreme yet, but the trend bears watching. It’s possible analysts are anticipating a recovery before institutional activity follows. Investors should monitor analyst guidance and institutional flows in the coming weeks.

For long-term holders, the pullback appears driven more by macroeconomic concerns than company-specific problems. Patient investors can collect the dividend while waiting for clearer economic signals. Prospective buyers may want to watch the 50-day simple moving average— a close and hold above that level could indicate a shift in momentum.

Thank you for subscribing to MarketBeat!

MarketBeat empowers investors to make better investment decisions by delivering real-time financial information and unbiased market analysis.

This email message is a paid sponsorship sent on behalf of The Early Bird, a third-party advertiser of MarketBeat. Why did I get this email message?.

If you need assistance with your newsletter, please email our South Dakota based support team at contact@marketbeat.com.

Over the past few months, many investors have likely encountered the phenomenon known as the “SaaS Apocalypse.” The term describes a wave of selling in software-as-a-service (SaaS) stocks as markets reassess the impact of new artificial intelligence (AI) tools.

To some extent, markets have been indiscriminately selling stocks with even a SaaS-adjacent business model. But the extent to which AI will disrupt each SaaS company is far from uniform.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

One tech stock that may fit this description is Datadog (NASDAQ: DDOG). While shares have recovered from recent lows, the stock is still down about 10% year-to-date in 2026 and nearly 40% from its 52-week high.

Some investors believe the market may be underestimating what Datadog’s role could look like in an AI-heavy enterprise environment.

Understanding the Drivers Behind the “SaaS Apocalypse”

One of AI’s big promises is that AI agents will be able to act autonomously within enterprise workflows.

The theory is that deploying agents will allow companies to cut costs by automating tasks that previously required expensive SaaS products or larger teams. That prospect has driven heavy selling of incumbent SaaS companies.

Proponents—including companies such as OpenAI, Anthropic, and Google’s parent Alphabet (NASDAQ: GOOGL)—argue that a single employee equipped with AI agents could replace the work of several people, reducing headcount and labor costs. Their pitch: pay to deploy AI agents, and you’ll need fewer employees.

However, AI is far from infallible and can make mistakes. Those errors are visible even with consumer-facing chatbots and can create distrust. Inside an organization, the consequences of mistakes can be larger—customer impact, revenue leakage, and operational disruption. Businesses are therefore unlikely to adopt AI agents at scale without first building trust and having fast, reliable tools to diagnose failures. This is where observability vendors say they can help.

Outsourcing Thinking: AI Agents Increase the Need for Observability

Datadog sells observability software. It collects telemetry from companies’ applications—both internal and customer-facing—so teams can detect problems, identify root causes, and resolve incidents.

While AI agents could reduce some labor costs, they also introduce complexity and generate much more observable data.

A video on Datadog’s AI Agent Monitoring toolillustrates this. The presenter describes a fictional personal-finance app called Budget Guru: a user asks the AI agents powering the app to buy $500 of a stock and remind them of an overdraft fee.

A human could perform that task in a few clicks and do the internal thinking required to execute it. Budget Guru, however, coordinated five separate AI agents to complete the request—effectively outsourcing the decision-making a human would have handled—and in the process generated a large volume of logs, traces, and events about how the outcome was reached.

AI agents create telemetry that would not exist if a human had performed the same task. As the number of moving parts grows, so do potential failure points. In that context, agents don’t eliminate the need for monitoring—they raise the bar for it.

That dynamic should increase demand for observability platforms like Datadog, turning dispersion risk into opportunity.

Datadog: Impressive Growth, Profitability, and Analyst Support

In its latest quarter, Datadog’s revenues rose 29%to $953 million. The company also generated free cash flow of $291 million, yielding a free cash flow margin of roughly 31%.

The Rule of 40 is a common metric for evaluating SaaS businesses, combining growth and profitability. Scores above 40 are considered healthy; Datadog’s score sits near 60.

Wall Street analysts also see upside. The MarketBeat consensus price target is near $180, implying more than 40% upside. Price targets updated after the company’s latest earnings report average slightly lower at about $174.

With strong growth, solid profitability, analyst backing, and potential agentic-AI tailwinds, there is reason to believe DDOG could weather—or even benefit from—the so-called “SaaS Apocalypse.”

This Month’s Bonus Story

Autonomous Security and the New AI Arms Race

Authored by Jeffrey Neal Johnson. Article Published: 3/25/2026.

Key Points

CrowdStrike’s massive, real-time dataset provides its AI-driven security platform a significant competitive advantage.

Palo Alto Networks leverages its comprehensive, all-in-one platform and proven profitability to capture the enterprise market.

The essential industry-wide shift toward autonomous security creates a powerful and durable tailwind for both companies.

The cybersecurity battlefield has fundamentally and irrevocably changed. A new class of autonomous artificial intelligence (AI), known as agentic AI, is being rapidly adopted by businesses to drive unprecedented productivity. But this powerful technology also creates an urgent, escalating threat: malicious actors are already weaponizing these tools to launch attacks that operate at a speed, scale, and sophistication beyond human capacity to manage.

That reality has triggered a nonnegotiable, industry-wide spending cycle. The era of relying on human-led security teams to manually triage alerts is over. To survive and operate, enterprises must now invest heavily in autonomous defense systems that can fight AI with AI.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

This market shift has created a substantial investment opportunity. Leading the way are two industry titans, CrowdStrike (NASDAQ: CRWD)and Palo Alto Networks (NASDAQ: PANW), each of which has launched pioneering platforms to address this new frontier. Their strategic moves are powerful near-term catalysts that position both companies for meaningful long-term growth.

CrowdStrike: Unleashing a Data-Fueled Growth Engine

CrowdStrike has built its reputation on speed and intelligence, and its latest move into autonomous security doubles down on those strengths. The company recently unveiled its Agentic MDR platform, an AI-driven service that automates the lifecycle of threat detection, investigation, and response. Rather than simply alerting overwhelmed analysts, the system is designed to autonomously handle incidents at machine speed—precisely what’s needed to counter AI-powered attacks.

Agentic MDR is the logical evolution of CrowdStrike’s chief competitive advantage: its data. The cloud-native Falcon platform is powered by the proprietary Threat Graph, a massive dataset that processes trillions of security events each week.

That real-time data trains CrowdStrike’s AI models, giving them an exceptional view of the threat landscape. A security AI is only as effective as the data it learns from, and CrowdStrike’s data reservoir creates a meaningful and durable competitive moat.

For investors, Agentic MDR reinforces CrowdStrike’s high-growth narrative. The company is already expanding rapidly, with year-over-year revenue growth near 24%. The new platform should accelerate adoption of the Falcon ecosystem and drive add-on sales of high-margin services, directly addressing industry-wide alert fatigue. That creates a clear path to faster growth in annual recurring revenue and supports CrowdStrike’s growth-oriented valuation—a compelling catalyst for CrowdStrike’s stock.

Palo Alto Networks: The Profitable AI Security Fortress

Where CrowdStrike emphasizes data-driven speed, Palo Alto Networks is leveraging market scale and breadth to become the indispensable security partner for AI-enabled enterprises.

Palo Alto recently launched Prisma AIRS 3.0, a platform that secures the full lifecycle of AI agents. It helps organizations discover the AI tools in use across their environment, assess associated risks, and enforce consistent security policies from a single console.

This product is the capstone of Palo Alto Networks’ platform strategy. Enterprises—especially large, Fortune 500 customers—are tired of managing dozens of separate security vendors. By offering an integrated platform that spans network firewalls, cloud security, and now agentic AI, Palo Alto makes its ecosystem highly sticky. Once a large company adopts the platform, switching costs and complexity become prohibitively high, locking in long-term revenue.

That approach has created a financial fortress. For investors, Prisma AIRS 3.0 is a catalyst to deepen customer relationships and drive predictable growth. Palo Alto Networks is already profitable, with a net margin around 13% and a strong history of free cash flow generation. The new AI security capabilities should increase customer lifetime value and further expand margins, supporting Palo Alto’s stock and reinforcing its status as a blue-chip leader.

Tale of the Tape: A Data-Driven Comparison

Both CrowdStrike and Palo Alto Networks stand to benefit from the AI security wave, but they offer distinct investment profiles. Here are the key differences:

Market Capitalization: Palo Alto Networks is larger, at approximately $128 billion, versus CrowdStrike’s roughly $100 billion valuation.

Revenue Growth (YOY): CrowdStrike leads with growth near 24%, while Palo Alto Networks posts a more mature but solid rate of about 15%.

Profitability (Net Margin): Palo Alto Networks is profitable with a net margin around 13%; CrowdStrike remains focused on growth and currently has a negative net margin.

Go-to-Market Strategy: CrowdStrike uses a land-and-expand approach—winning customers with its endpoint solution and upselling new modules. Palo Alto leverages incumbency to drive platform consolidation across the enterprise.

Core Advantage: CrowdStrike’s case rests on an AI-native, data-centric advantage and operational agility. Palo Alto’s strength is its entrenched, all-in-one enterprise platform and established profitability.

Choosing Your Champion for the Next Wave of Cybersecurity

Autonomous security is not a distant prospect; it is already reshaping the industry and creating a durable tailwind for cybersecurity vendors. For investors, the question isn’t whether the market will generate returns, but how best to capture that growth.

If you prioritize aggressive growth and innovation, CrowdStrike offers a focused bet on a best-of-breed, data-centric approach to AI security. Its momentum and market-share potential present an opportunity for above-market returns.

If you prefer stability and proven market leadership, Palo Alto Networks is the fortified incumbent. Its deep enterprise entrenchment, strong profitability, and integrated platform strategy create a predictable, long-term growth trajectory.

Ultimately, the choice depends on your investment objectives. What’s clear is that the AI security transition is a rising tide likely to lift both companies. Their recent platform launches are strong signals that CrowdStrike and Palo Alto Networks are well positioned for the most important technology trend of the next decade, making them compelling contenders for portfolios focused on the future.

Thank you for subscribing to DividendStocks.com’s daily newsletter for dividend and income investors that covers ex-dividend stocks, new dividend declarations, dividend stock ideas, and the latest market news.

This email content is a sponsored email sent on behalf of MarketBeat Alerts, a third-party advertiser of DividendStocks.com and MarketBeat.

If you have questions about your newsletter, feel free to contact MarketBeat’s South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

Equity Markets: U.S. stocks closed lower on Friday, with declines led by consumer discretionary and financials stocks. The S&P 500 is down over 7% for the year, while the Nasdaq remains in correction territory. Energy once again stood out as the top-performing sector, continuing its strong start to 2026 amid rising oil prices. Globally, Asian markets were mixed, and European markets trended lower.

Energy Markets: WTI crude prices moved higher amid ongoing disruptions in the Strait of Hormuz. Despite near-term volatility, opportunities continue to emerge across different asset classes.

Economic Data: The University of Michigan consumer sentiment index for March was revised down to 53.3, below expectations of 54.0. Rising gas prices and market volatility were cited as key drivers. Short-term inflation expectations climbed to 3.8% from 3.4%, raising concerns about persistent price pressures. Meanwhile, the S&P Global U.S. Manufacturing PMI increased to 52.4 from 51.6 in February, above the 51.3 forecast, led by a strong rise in new orders, particularly in export-driven sectors.

Bond Market: Yields moved higher, with the 10-year Treasury yield approaching 4.44%. The Atlanta Fed’s GDPNow model revised its Q1 GDP estimate down to 2.0% from 2.3% last week.

Tech & Cybersecurity: Cybersecurity stocks faced heavy selling pressure. CrowdStrike (CRWD) fell ~6% and Palo Alto Networks (PANW) dropped ~4% after reports of security risks tied to a new AI model by Anthropic. Semiconductor and memory stocks also declined sharply after Google (GOOGL) unveiled a new AI model designed to reduce memory requirements. Micron (MU) has now fallen six sessions in a row, while SanDisk, Western Digital, and Seagate each dropped over 1.5%. The PHLX Semiconductor Index (SOX) fell, with Nvidia (NVDA) hitting a three-month low.

Precious Metals & Crypto: Gold futures hovered near three-month lows under $4,500, influenced by reduced central bank buying. Bitcoin futures (/BTC) also dropped, signaling a broader risk-off sentiment. The Bitwise 10 Large Cap Crypto Index fell 6% week-over-week.

Corporate Highlights:

Tripadvisor (TRIP) gained following a Bank of America upgrade.

AstraZeneca (AZN) rose on positive clinical trial results for a COPD treatment.

Meta (META) and Alphabet (GOOGL) declined after a Los Angeles jury ruled both liable in a social media addiction case.

Netflix (NFLX) increased subscription prices for the first time since January 2025.

Other Key Headlines:

Tiger Woods Arrested: The golfer was arrested for a DUI following a rollover crash in Florida, raising questions about his health and potential participation in the upcoming Masters.

Global Trade: WTO members moved forward with the first baseline digital trade rules without full consensus, highlighting progress and ongoing tensions in shaping modern trade frameworks.

Legal News: Bank of America agreed to a $72.5 million settlement with victims of Jeffrey Epstein, part of a series of major legal payouts involving banks linked to his trafficking network.

Trump Signs Order to Pay TSA Workers Amid DHS Shutdown Standoff

Donald Trump signed an executive action Friday to ensure Transportation Security Administration employees receive pay after Congress failed to reach a funding agreement for the Department of Homeland Security. The move is aimed at easing mounting disruptions at U.S. airports. In the order, Trump said the administration would use “funds that have a reasonable and logical nexus to TSA operations,” calling the situation an emergency that threatens national security and strains the air travel system. Markwayne Mullin said TSA employees could begin receiving paychecks as soon as Monday.

Buffett Watch: Berkshire’s Losing Streak Extends as Market Pressures Build

Shares of Berkshire Hathaway have declined for eight consecutive trading sessions, marking their longest losing streak in more than seven years. This is the company’s longest stretch of daily losses since December 2018. Both share classes have come under pressure, with Class A shares down 4.7% and Class B shares falling 4.9% since their last gains on March 17. The decline comes amid broader market weakness driven by rising energy prices and geopolitical uncertainty tied to the Iran conflict.

Earnings Spotlight: Conagra Brands (CAG)

Conagra Brands (CAG) is expected to report Q3 2026 earnings on April 1, with analysts forecasting a decline in revenue to $2.77 billion (down 2.6%) and earnings of 40 cents per share (down 21.6%). High input costs and increased promotional spending are offsetting improvements in frozen and snack volumes, leading to expected top and bottom-line pressure.

What’s Ahead

Economic:

Monday (March 30): no reports

Tuesday (March 31): Chicago PMI, Consumer Confidence, FHFA Housing Price Index, S&P Case-Shiller Home Price Index

Wednesday (April 1): ADP Employment Change, Construction Spending, EIA Crude Oil Inventories, ISM Manufacturing Index, MBA Mortgage Applications Index

Thursday (April 2): Business Inventories, Continuing Claims, EIA Natural Gas Inventories, Factory Orders, Initial Claims

Friday (April 3): Nonfarm Payrolls, Unemployment, Average Hourly Earnings, Average Workweek, ISM Non-Manufacturing Index

Earnings:

Monday (March 30): Aura Biosciences Inc. (AURA), Bicara Therapeutics Inc. (BCAX), Fermi Inc. (FRMI), ICON PLC (ICLR), Maze Therapeutics Inc. (MAZE), Progress Software Corp. (PRGS), Rezolve AI PLC (RZLV), USA Rare Earth Inc. (USAR)

Tuesday (March 31): Chagee Holdings Ltd. (CHA), FactSet Research Systems Inc. (FDS), McCormick & Company (MKC), nCino Inc. (NCNO), Nike Inc. (NKE), PVH Corp. (PVH)

Wednesday (April 1): Cal-Maine Foods Inc. (CALM), Conagra Brands Inc. (CAG), Lamb Weston Holdings Inc. (LW), MSC Industrial Direct Co. (MSM), NovaGold Resources Inc. (NG), RH Inc. (RH), UniFirst Corp. (UNF)

Thursday (April 2): Acuity Inc. (AYI), AngioDynamics Inc. (ANGO), Lindsay Corp. (LNN)

Friday (April 3): Trilogy Metals Inc. (TMQ)

Disclaimer: We are engaged in the business of advertising and promoting companies. All content on our website is for informational purposes only and should not be construed as an offer or solicitation of an offer to buy or sell securities. Neither the information presented nor any statement or expression of opinion, or any other matter herein, directly or indirectly constitutes a solicitation of the purchase or sale of any securities. Neither the owner of Trading Wire nor any of its members, officers, directors, contractors or employees are licensed broker-dealers, account representatives, market makers, investment bankers, investment advisers, analyst or underwriters. Investing in securities, including the securities of those companies profiled or discussed on this website is for individuals tolerant of high risks. Viewers should always consult with a licensed securities professional before purchasing or selling any securities of companies profiled or discussed on Trading Wire. It is possible that a viewer’s entire investment may be lost or impaired due to the speculative nature of the companies profiled. Remember, never invest in any security of a company profiled or discussed on this website unless you can afford to lose your entire investment. Also, investing in micro-cap securities is highly speculative and carries an extremely high degree of risk. Trading Wire makes no recommendation that the securities of the companies profiled or discussed on this website should be purchased, sold or held by viewers that learn of the profiled companies through our website.

Some of the content on this website contains “forward-looking statements.” Such statements may be preceded by the words “intends,” “may,” “will,” “plans,” “expects,” “anticipates,” “projects,” “predicts,” “estimates,” “aims,” “believes,” “hopes,” “potential,” or similar words. Forward-looking statements are not guarantees of future performance, are based on certain assumptions, and are subject to various known and unknown risks and uncertainties, many of which may be beyond a company’s control, and cannot be predicted or quantified, and, consequently, actual results may differ materially from those expressed or implied by such forward-looking statements. It is hereby noted that forward-looking statements contained herein may include everything other than historical information, involve risk and uncertainties that may affect a company’s actual results of operation. A company’s actual performance could greatly differ from those described in any forward-looking statements or announcements mentioned on this website or the websites contained within. Factors that should be considered that could cause actual results to differ include: the size and growth of the market for the company’s products; the company’s ability to fund its capital requirements in the near term and in the long term; pricing pressures; unforeseen and/or unexpected circumstances in happenings; etc. and the risk factors and other factors set forth in the company’s filings with the Securities and Exchange Commission. However, a company’s past performance does not guarantee future results.

Generally, the information regarding a company profiled or discussed on this website is provided from public sources tradingwire.com makes no representations, warranties or guarantees as to the accuracy or completeness of the information provided or discussed. Viewers should not rely solely on the information obtained through our website or in communications originating from our website. Viewers should use the information provided by us regarding the profiled companies as a starting point for additional independent research on the companies profiled or discussed in order to allow the viewer to form his or her own opinion regarding investing in the securities of such companies. Factual statements, or the similar, made by the profiled companies are made as of the date stated and are subject to change without notice and Trading Wire has no obligation to update any of the information provided. Trading Wire, its owners, officers, directors, contractors and employees are not responsible for errors and omissions.

From time to time certain content on this website is written and published by our employees or third parties. In addition to information about our profiled companies, from time to time, our website will contain the symbols of companies and/or news feeds about companies that are not being profiled by us but are merely illustrative of certain activity in the micro cap or penny stock market that we are highlighting. Viewers are advised that all analysis reports and news feeds are issued solely for informational purposes. Any opinions expressed are subject to change without notice. It is also possible that one or more of the companies discussed or profiled on this website may not have approved certain or any statements within the website. Trading Wire encourages viewers to supplement the information obtained from this website with independent research and other professional advice. The content on this website is based on sources which we believe to be reliable but is not guaranteed by us as being accurate and does not purport to be a complete statement or summary of the available data. Third Party Web Sites and Other Information This website may provide hyperlinks to third party websites or access to third party content.Trading Wire, its owners, officers, directors, contractors and employees are not responsible for errors and omissions nor does Trading Wire control, endorse, or guarantee any content found in such sites. Trading Wire does not control, endorse, or guarantee content found in such sites. By accessing, viewing, or using the website or communications originating from the website, you agree that Trading Wire, its owners, officers, directors, contractors and employees, are not responsible for any content, associated links, resources, or services associated with a third party website. You further agree that Trading Wire, its owners, officers, directors, contractors and employees shall not be liable for any loss or damage of any sort associated with your use of third party content. Links and access to these sites are provided for your convenience only. Trading Wire uses third parties to disseminate information to subscribers. Although we take precautions to prevent others from obtaining our subscriber list, there is a risk that our subscriber list, through no wrong doing on our part, could end up in the hands of an unauthorized party and that subscribers will receive communications from unauthorized third parties. We encourage viewers to invest carefully and read the investor issuer information available at the web sites of the United States Securities and Exchange Commission (SEC). The SEC has launched an investor-focused website to help you invest wisely and avoid fraud at www.investor.gov and filings made by public companies can be viewed at www.sec.gov and/or the Financial Industry Regulatory Authority (FINRA) at: www.finra.org. In addition, FINRA has published information at its website on how to invest carefully at www.finra.org/Investors/index.htm.

Our investment research analysts are going to be releasing their next investment idea tomorrow morning, around 10:00 AM Eastern time.

It will be first sent to subscribers that sign up to receive American Market News via SMS, then later in the morning to people who subscribe to our email newsletter or read our content on our website.

Don’t miss out on your opportunity to be among the first to see our next stock idea. Our last idea was quite popular with our subscribers.

This is a free service from American Market News. If you want to take advantage of this unique research opportunity, just click the link below to be added to our priority distribution list.

Investors often live between two extremes. One is taking aggressive swings at growth stocks, including some that are highly speculative. The other is exiting equities altogether and waiting for brighter days.

There are obvious risks to both approaches. Being too aggressive can leave investors exposed to large and unnecessary losses when the market turns. Conversely, sitting out when a bullish reversal occurs prevents investors from capturing the biggest gains.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

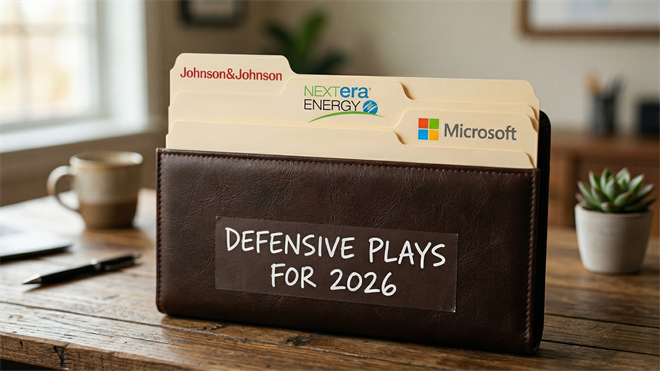

That’s a long way of saying that attempting to time the market isn’t an ideal strategy. A better approach is to own stocks that play offense and defense at the same time — the kind of strategy that can serve investors well after a quarter marked by uncertainty and elevated volatility, leaving many questions unanswered.

JNJ: Innovation With a Defensive Core

Since spinning off its consumer products division in 2023, some investors have come to view Johnson & Johnson (NYSE: JNJ) more like a technology stock, with growth increasingly anchored in innovation.

Those views are supported by a company that has shown solid year-over-year (YOY) revenue growth. Johnson & Johnson has also delivered robust earnings despite ongoing headwinds from litigation and tariffs.

Its Innovative Medicine division has successfully mitigated the impact of the patent cliff on past blockbusters like Stelara. The company’s medtech business is also beginning to show the benefits of high-growth, high-margin products, including robotics.

But with JNJ, getting hung up on the next quarter misses the point. Don’t get me wrong: 43% stock-price growth over 12 months is impressive. Still, it’s the company’s proven financial stability that provides the foundation for defensive-minded investors.

That’s one reason Johnson & Johnson is one of the rare stocks to have joined the ranks of the Dividend Kings. It has increased its dividend for 64 consecutive years, allowing generations of investors to benefit from compounding with JNJ stock.

NEE: Powering Growth the Steady Way

NextEra Energy (NYSE: NEE) is the most defensive play in this group. While it lacks the flash of some growth names, it embodies the steady offense-defense blend long-term investors crave. As North America’s largest generator of wind and solar energy, it sits at the forefront of the clean-energy transition.

What’s often overlooked is how well NextEra balances a growth mindset with predictable, regulated cash flow from its utility business, Florida Power & Light. That dual structure helps stabilize earnings, even during market turbulence or shifting rate expectations.

After a difficult 2023 that compressed its valuation under higher interest-rate pressure, NextEra has steadily rebuilt credibility by reaffirming its earnings-growth forecast of 6% to 8% annually through at least 2027. Management’s focus on disciplined capital allocation and funding projects from operations rather than debt is also helping restore investor confidence.

Dividends are another constant. NextEra is a Dividend Aristocrat that has raised its payout for 31 consecutive years, combining utility reliability with forward-looking innovation. For investors playing the long game in an uncertain macro environment, NEE offers a rare mix of defensive income and renewable-driven upside.

MSFT: A Safe Haven in Smart Tech

Microsoft (NASDAQ: MSFT) may not typically top lists of defensive stocks, but 2026 is no ordinary year. Here’s why Microsoft can be attractive to defensive-minded investors.

It starts with Azure, the company’s cloud platform, which combines compute, storage, networking, security, data and artificial intelligence (AI) into a full-stack solution. That mix of hybrid-friendly architecture, enterprise-grade security and AI integration forms the backbone of Microsoft’s competitive moat. Saying Azure drives sticky revenue is an understatement.

That part of the Microsoft story gets lost amid concerns about Copilot and the company’s fracturing partnership with OpenAI. Azure remains Microsoft’s growth engine, expanding at roughly 30% YOY.

The company is protecting that growth by investing to own its data centers. While that raises some concerns, they are largely misplaced: Microsoft is funding the expenditures with cash on hand, so shareholders face little risk of dilution.

Investors can view the current pullback as a buying opportunity. Trading around 23x earnings, MSFT is priced at a discount to its historical average and to the broader NASDAQ-100 index.

Sunday’s Bonus Article

A Market Divided on SentinelOne’s Future

Submitted by Jeffrey Neal Johnson. Article Published: 3/17/2026.

Key Points

SentinelOne recently achieved major operational milestones, including full-year profitability and significant revenue scale.

An unusually high volume of bullish call options indicates that sophisticated traders expect the stock’s price to rise.

SentinelOne’s long-term growth and profitability forecast, supported by Wall Street analysts, points toward future upside.

A perplexing scenario is unfolding around cybersecurity innovator SentinelOne (NYSE: S). The company recently reported a landmark fiscal year, hitting milestones that suggest it is gaining momentum. It crossed the coveted $1 billion annual revenue mark and, for the first time, delivered a full year of non-GAAP operating profitability. Despite these achievements, the market’s initial reaction to the results was nervous, and the stock came under immediate downward pressure.

Underneath that volatility, however, a strikingly different signal emerged. In the options market—where sophisticated traders often place high-conviction bets—bullish activity on SentinelOne surged. That created a clear division: a broader market reacting to a near-term forecast versus traders betting on a larger, potentially more profitable story.

The $7 Trillion Race for America’s Critical New Resource Moody’s calls it “the new oil.” Fox News calls it the “new arms race.” Elon Musk calls it “mind-blowing.” Demand is already doubling every 6 months. And on April 20, a major global event could ignite a handful of under-the-radar stocks, setting off what could be the biggest resource boom in history.Click here now for the full story

At the heart of this puzzle is the contrast between SentinelOne’s full-year performance and its conservative near-term outlook. For growth investors, scale plus profitability signals a maturing, sustainable business model, and SentinelOne’s fiscal 2026 results deliver that foundation.

Financial Milestones: Total revenue grew 22% to $1.001 billion. Annualized Recurring Revenue (ARR) climbed 22% to $1.12 billion, helped by a company-record $64 million in net new ARR in the final quarter. Reaching profitability reduces dependence on capital markets and signals operational discipline.

Platform Strength: SentinelOne is deepening customer relationships: 65% of enterprise clients now use three or more of its solutions. That deeper integration was validated by a major strategic win — securing internet infrastructure giant Cloudflare (NYSE: NET) by displacing a key competitor, widely understood to be rival CrowdStrike (NASDAQ: CRWD).

Diversified Growth Engines: SentinelOne is expanding beyond endpoint security. Its data solutions platform tops $130 million in ARR, while cloud security offerings exceed $160 million in ARR. These multiple growth pillars reduce reliance on any single segment.

That strong performance was briefly overshadowed by SentinelOne’s guidance for the first quarter of fiscal 2027. Management forecast revenue of $276 million to $278 million—just below analysts’ expectations—which prompted the initial sell-off.

The full-year outlook, though, is far more encouraging. SentinelOne projects fiscal 2027 revenue of $1.195 billion to $1.205 billion, roughly 20% growth. More notably, management is guiding to a full-year non-GAAP operating margin of about 10%, putting the company on a path toward the Rule of 40—a key benchmark for software investors that combines growth and profitability.

An Unmistakable Tell in the Options Market

While the stock chart initially reflected confusion, the options market sent a decisive message. On Friday, March 13, investors bought 19,630 call options on SentinelOne—about a 37% spike above the average daily volume. That surge came as the stock dipped in pre-market trading, suggesting traders viewed the weakness as a buying opportunity.

Institutional traders and other sophisticated participants often use options to place high-conviction bets with greater capital efficiency than buying shares outright. A call option gives the buyer the right to purchase a stock at a set price by a certain date. A sudden, large increase in call buying—especially amid seemingly negative headlines—is a strong indicator that experienced market participants believe the initial reaction is overdone and the stock may be undervalued.

The data reinforce that view. The volume put-to-call ratio that day was an exceptionally low 0.06. That compares bearish bets (puts) to bullish bets (calls); a 0.06 reading means bullish volume was more than 16 times higher than bearish volume, signaling pronounced positive sentiment.

SentinelOne’s intraday price action seemed to validate the optimism. After the pre-market drop, shares reversed and closed the regular session up nearly 5%. The options activity suggests traders expect the stock to rebound and that the guidance-induced dip may be transient.

Finding the Signal in the Noise

The narrative around SentinelOne is split between short-term noise and a longer-term signal. A cautious first-quarter forecast introduced volatility, but the company’s improving fundamentals and the options market’s emphatic message point to a bullish outlook. While some investors sold on the headline, others bought based on the substance of a profitable, growing enterprise.

That bullishness extends beyond the options pits. Despite trimming near-term price targets to reflect guidance, Wall Street analysts maintain a Moderate Buy consensus rating on the stock. The average price target of $19.43 implies upside of more than 30% from recent closing prices. For investors, the divergence between the initial market reaction and the surge in options activity makes a case for focusing on SentinelOne’s improving profitability, durable growth, and strategic position rather than reacting solely to a single quarter’s forecast.

Thank you for subscribing to Earnings360, a morning newsletter that summarizes quarterly earnings for public companies that trade on U.S. markets.

This email content is a sponsored email provided by American Market News, a third-party advertiser of Earnings360 and MarketBeat.

If you have questions or concerns about your newsletter, please feel free to contact our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. 345 N Reid Place, Suite 620, Sioux Falls, South Dakota 57103. USA..

Good morning. It’s Sunday. Here are today’s top stories:

More than 3,500 U.S. sailors and Marines aboard the USS Tripoli have arrived in the Middle East as the Pentagon continues to build up forcesin the region.

Iran has agreed to allow 20 Pakistani-flagged ships to pass through the Strait of Hormuz unharmed, Pakistani Foreign Minister Ishaq Dar said, calling the development “a meaningful step toward peace.”

A month has passed since U.S. and Israeli forces jointly launched a surprise attack on Iran, delivering the opening blow in an ongoing effort the U.S. military has dubbed Operation Epic Fury. Here’s where things stand after four weeks of fighting.

American Family farms face tough challenges in today’s economy, but some young farmers are finding success—and believe their kids will, too.

🍵 Health:This overlooked organ is linked to longevity, new researchsuggests.

U.S. Marines conduct a hike during a simulated amphibious assault on March 24, 2026. (U.S. Marine Corps photo by Cpl. Maksim Masloboev)

More than 3,500 U.S. sailors and Marines aboard the USS Tripoli have arrived in the Middle East as the Pentagon continues to build up forces in the region.

U.S. Central Command (CENTCOM) said on March 29 that the USS Tripoli had entered its area of responsibility. The amphibious assault ship is serving as the flagship of the Tripoli Amphibious Ready Group and the 31st Marine Expeditionary Unit, a combined force that includes ground, air, and naval elements.

One of the newest and most capable amphibious assault ships in the U.S. fleet, the USS Tripoli is designed to accommodate a larger air wing, including F-35 stealth fighter jets, V-22 “Osprey” tiltrotor aircraft, and other warplanes. It had been based in Japan before receiving orders nearly two weeks ago to deploy to the Middle East.

CENTCOM said the Tripoli brings transport aircraft, strike fighters, and amphibious assault capabilities to the region in addition to the Marines aboard.

The USS Boxer, another amphibious assault ship, along with the 11th Marine Expeditionary Unit, has also been ordered to the region from San Diego.

CENTCOM did not disclose more details on where the additional U.S. forces will be positioned, though they are likely to operate within striking distance of Iran, including near key locations such as Kharg Island, a major Iranian oil export terminal off the country’s coast.

In its most recent update on March 25, marking the fourth week of the campaign, CENTCOM said that more than 11,000 targets had been struck since the United States and Israel launched joint operations against Iran on Feb. 28. (More)

IRAN WAR

A spokesman for the Iran-aligned Houthi terrorist organization in Yemen said that the group had entered the Middle East conflict, launching a missile attack against Israel that Tel Aviv said was intercepted.

President Donald Trump said Friday that the United States likely doesn’t have to be there for NATO, noting that the alliance has provided little to no material support to U.S. military efforts against the Iranian regime.

A packed crowd at the Conservative Political Action Conference roared their approval as Iranian Crown Prince Reza Pahlavi urged President Donald Trump to reject leaving any faction of the Islamic regime in power.

LATEST NEWS

The partial shutdown of the Department of Homeland Security tied for the longest shutdown in U.S. history on March 28.

The Idaho legislature on Friday passed a bill that would make it a crime for anyone to use a public restroom or changing room of the opposite sex.

WORLD

Europe is going to need a “Trump-style revolution” to turn back the tide of illegal immigration that has changed the face of Europe, according to two former prime ministers.

The United States accused China of detaining Panama-flagged vessels in response to Panama’s termination of Hong Kong-based CK Hutchison’s concessions for two key ports.

The Chinese Communist Party has unveiled a long-term care insurance program that will require pensioners to continue contributing premiums, marking a significant shift in the country’s social welfare system and sparking public backlash.

OPINION: Charge Iran and China for Increasing US Gas Prices—by Anders Corr (Read)

🇺🇲American Thought Leaders: He Ran the World’s Biggest Payment Processor; Now He’s Taking on Social Security—Frank Bisignano (Watch)

Many of the most memorable April Fools’ Day hoaxes rely on careful storytelling, convincing details, and just enough plausibility to make audiences hesitate before laughing. (Robert Couse-Baker/CC BY 2.0)

On April 1, 1957, the usually staid British Broadcasting Corp. (BBC) reported that a Swiss region bordering Italy had produced an “exceptionally heavy spaghetti crop” that season due to the mild winter and the eradication of the spaghetti weevil. The camera panned farmers and gardeners picking spaghetti from trees, then sitting down to enjoy a supper of delicious pasta.

To be fair, spaghetti was unfamiliar to many Brits at the time. Other viewers immediately realized that the broadcasting giant had put together an elaborate April Fools’ Day joke, with a few in the audience upset that the BBC had broken character to run such nonsense. Yet many others swamped the station with phone calls, looking for details on how to grow their own spaghetti. BBC wits replied to these requests: “Place a sprig of spaghetti in a tin of tomato sauce and hope for the best.”

Older Americans will remember the Sidd Finch prank. The April 1, 1985, edition of “Sports Illustrated” ran George Plimpton’s “The Curious Case of Sidd Finch.” In this lengthy article, the well-known sportswriter reported the story of British orphan Hayden Siddhartha Finch, a 28-year-old versed in foreign languages, talented on the French horn, a Harvard dropout, and an aspirant Buddhist monk to boot, who might soon be pitching for the New York Mets. His throws across the plate were clocked at superhuman speeds as high as 168 mph.

Plimpton gleaned fictitious reactions from the team’s batters, whom Finch had supposedly pitched against in secret, and cited numerous conversations with Finch’s former fellow students and with Mets staff. The Mets went along with the gag, giving Finch a number and a locker. (More)

🎲 Games

Spot the Difference is our readers’ favorite. Play it here.

Our mailing address is: The Epoch Times, 129 West 29th Street, Fl 8, New York, NY 10001 | Contact Us

Our Morning Brief newsletter is one of the best ways to catch up with the news. Manage your email preferences here or unsubscribe from Morning Brief here.