I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

Avoid risky picks! The Safe Stock Selector Checklist reveals how to find strong, reliable stocks before the crowd catches on. Get Your Free Report Now. [ad]

Louis Navellier spent 46 years building a system that measures what institutions measure before they buy. When his grading system upgrades a stock from C to B, it means: BlackRock, Vanguard others could be about to deploy billions. That’s when retail investors should buy – not 6 months later when CNBC covers it. Get 3 FREE STOCK SEARCHES and see how YOUR stocks grade right now. [ad]

Conflict in Iran has sent oil prices up, prompting some experts to worry that stagflation, or low economic growth and high inflation, could be possible for the U.S. economy.

Privacy Policy | Advertiser DisclosureDISCLAIMER: Stocks and options trading have large potential rewards, but also large potential risk. You must be aware of the risks and be willing to accept them in order to invest in the stocks and options markets. Don’t trade with money you can’t afford to lose. This is neither a solicitation nor an offer to Buy/Sell stocks or options. No representation is being made that any account will or is likely to achieve profits or losses similar to those discussed in this report. The past performance of any trading system or methodology is not necessarily indicative of future results. All trades, patterns, charts, systems, etc., discussed in this report are for illustrative purposes only and not to be construed as specific advisory recommendations. Information contained in this correspondence is intended for informational purposes only and was obtained from sources believed to be reliable. Information is in no way guaranteed. No guarantee of any kind is implied or possible where projections of future conditions are attempted.

Stockguru LLC (dba InvestingDistrict), 2563 cherry hill ln, Hermitage, PA 16148, United StatesYou may unsubscribe or change your contact details at any time.

This information is disseminated on behalf of Metalla Royalty & Streaming.

*MTA* Shows Signs of life at the open Runs then pulls back a bit BUT…

The post market ticker tape is back over $8.00…

We’re gonna keep this one going. Gold Was down but this was Up!!

there’s more unfolding to this story.. We can feel it!

So here we go!

ROUND 2 Starts tomorrow!

*NYSE:MTA*

and this still looks GOLDEN (6 month chart)

Full report below compensation in the disclaimer.

Metalla Royalty & Streaming (MTA): A High-Margin Gateway to Strong Gold, Resilient Silver, and Copper’s Structural Supply Crunch!

MTA is Leveraged Exposure to Record Gold, Surging Silver, and Copper’s Structural Supply Crunch — Without the Operational Risk of Mining!

Greetings All,

Gold has reasserted itself as a monetary anchor in an era defined by inflation persistence, sovereign debt expansion, and central bank accumulation. Silver’s dual role as both a store of value and a critical industrial input is amplifying upside pressure as renewable energy and electrification demand accelerates. Copper, meanwhile, is increasingly viewed as a strategic metal essential to energy security, electric vehicles, and next-generation infrastructure—just as new supply struggles to come online.

Within this backdrop, companies that can offer leveraged exposure to all three metals—without the capital intensity and operational volatility of mining—stand out.

Metalla Royalty & Streaming (NYSE: MTA) is emerging as one of those differentiated platforms.

A Royalty Model Built for Margin Expansion

MTA operates a royalty and streaming model, meaning it provides capital to mining operators in exchange for a percentage of future production or revenue. It does not operate mines. It does not bear sustaining capital costs. It does not face labor disputes, environmental liabilities, or cost overruns!

Instead, itreceives top-line exposure to metal prices and production growth.

In a rising price environment—especially one where cost inflation pressures miners—this model can produce expanding margins and scalable cash flow. As production increases across its underlying assets, revenue can grow without proportional increases in expenses. That structural advantage becomes particularly powerful during strong commodity cycles like the one that has been unfolding. Gold and silver hit record highs in early 2026.

A Clear Financial Inflection Point

The third quarter of 2025 marked a defining milestone. MTAreported its first-ever profitable quarter, with revenue more than doubling year-over-year to $4 million and net income turning positive.

Management characterized the quarter as a “step-change” moment—signaling that the company’s portfolio has reached the scale necessary to generate sustainable earnings.

This transition from portfolio builder to cash-flow generator is critical. Royalty companies often require years of disciplined asset accumulation before meaningful earnings materialize.

With profitability now established and multiple development assets advancing toward production, MTAappears to be entering a new phase of financial maturity.

Diversified Exposure Across Gold, Silver, and Copper

MTA’s portfolio includes approximately 100 royalties spanning producing, development, and exploration-stage assets across gold, silver, and copper.

This diversification reduces reliance on any single project while embedding multiple pathways to upside through mine expansions, restarts, feasibility updates, and exploration success.

Its exposure aligns closely with the dominant macro forces of 2026.

Gold’s surge reflects monetary hedging and central bank demand. Silver’s breakout is supported by accelerating industrial usage in solar and electrification. Copper faces projected structural supply deficits as electric vehicles, renewable infrastructure, and AI-driven data centers expand globally.

By holding royalties across all three metals, MTA captures both precious-metal monetary demand and base-metal industrial growth.

Built-In Catalysts Without Additional Capital Risk

A distinguishing feature of the royalty model is perpetual optionality. As operators advance projects, expand capacity, extend mine lives, or discover additional resources, the royalty holder benefits automatically—without investing incremental capital.

MTA’s portfolio includes numerous near-term catalysts: mine restarts, production ramp-ups, staged expansions, permitting milestones, and construction decisions across multiple jurisdictions. Each development has the potential to increase attributable production and royalty revenue, reinforcing the company’s ability to compound cash flow over time.

Institutional Validation and Strategic Capital

Another noteworthy development has been institutional interest. Public disclosures revealed that affiliated entities of Tether collectively hold approximately 8.9% of MTA’s outstanding shares.

As one of the largest physical gold buyers in recent quarters, Tether-linked capital entering the royalty space highlights a broader convergence between digital liquidity and hard-asset exposure.

While the investment remains passive, the presence of a well-capitalized and globally recognized financial player adds visibility and may signal confidence in the long-term thesis surrounding precious metals and diversified royalty platforms.

Why Streaming and Royalties Can Outperform Traditional Mining in Volatile Commodity Cycles

Unlike traditional mining companies, royalty and streaming businesses do not operate mines, manage labor forces, fund sustaining capital, or absorb cost overruns.

Instead, they provide upfront financing to operators in exchange for a percentage of future production (royalties) or the right to purchase metal at predetermined, discounted prices (streams).

This structure allows them to maintain exposure to rising gold, silver, and copper prices while avoiding many of the operational risks that can erode margins during inflationary periods.

When energy, labor, or equipment costs rise, miners feel the pressure directly—royalty and streaming companies generally do not. As production grows or metal prices increase, their revenue can scale with minimal incremental expense.

The Bottom Line

The metals breakout seen in early 2026 was driven by monetary instability, industrial transformation, and strategic de-risking from concentrated supply chains. Gold’s record highs, silver’s industrial acceleration, and copper’s tightening structural supply picture together form a powerful macro backdrop.

Within this environment, Metalla Royalty & Streaming (MTA) offers leveraged exposure to all three metals through a diversified, high-margin royalty model that minimizes operational risk while maximizing upside participation.

With its first profitable quarter behind it, a deep pipeline of catalysts ahead, and growing institutional attention, MTA appears increasingly positioned to benefit. Start your research!

Disclaimer

Hugealerts.com and Tradingwire.com are owned by Sideways Frequencey LLC (“Sideways Frequency”). Press releases, research reports, company profiles and other investor relations materials, publications or presentations, including web content (investor awareness services) released by Hugealerts.com and Tradingwire.com are based on publicly available data obtained from sources we believe to be reliable but are not guaranteed as to accuracy and are not purported to be complete. As such, the information should not be construed as advice designed to meet the particular investment needs of any investor. Furthermore, some of the content contained in our publications and websites may contain forward-looking statements found in information made publicly available by the companies we highlight. This forward looking information fits within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 including statements regarding future possible events, expected continual growth of a company, the potential value of its securities, and look forward in time which include everything other than historical information, involve risk and uncertainties that may affect a company’s actual results of operation. We therefore strongly encourage that you visit and review any and all financial information made publicly available by highlighted companies. Any opinions expressed in Hugealerts.com and Tradingwire.com reports, company profiles, or other investor relations materials and presentations are subject to change, are expressed and given as of the date of publication, and we disclaim any obligation to advise you of any change in any information contained herein. The information contained herein is not intended to be used as the basis for investment decisions and should not be construed as advice intended to meet the particular investment needs of any investor. The information contained herein is not a representation or warranty and is not an offer or solicitation of an offer to buy or sell any security. To the fullest extent of the law, Hugealerts.com,Tradingwire.comand their affiliates, specialists, advisors, and partners will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of the information provided, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information provided to any person or entity (including but not limited to lost profits, loss of opportunities, trading losses and damages that may result from any inaccuracy or incompleteness of this information). Stock market investing is inherently risky. Hugealerts.com, Tradingwire.com and their affiliates are not responsible for any gains or losses that result from the opinions expressed in press releases, on this website, in its research reports, company profiles or in other investor relations materials or presentations that it publishes electronically or in print. We strongly encourage all investors to conduct their own research before making any investment decision. For more information on stock market investing, visit the Securities and Exchange Commission (“SEC”) at www.sec.gov. and/or the Ontario Securities Commission (“OSC”) at www.osc.gov.on.ca. and/or the British Columbia Securities Commission (“BCSC”) at https://www.bcsc.bc.ca/.

Income Disclosure

Sideways Frequency has been retained by Metalla Royalty and streaming LTD (NYSE:MTA).and has received cash compensation of $150,000.00 to perform promotional and advertising services for a limited time. This agreement has been ongoing since February 2026 and is related to the engagement of investor awareness services for Metalla Royalty and streaming LTD (NYSE:MTA).. Sideways Frequency, Hugealerts.com, Tradingwire.com and their partners and affiliates may buy and sell shares of securities or options and warrants of the companies mentioned on this website at any time.

Sideways Frequency LLC and its affiliates may buy and sell shares of securities or options and warrants of the companies mentioned in this publication or website at any time but are not and will not at any time become affiliates or owners of more than 5% of the issued and outstanding stock of the highlighted companies.

Sideways Frequency and its beneficial owners and affiliates, including Hugealerts.com andTradingwire.com do not own any shares in Metalla Royalty and streaming LTD (NYSE:MTA).

Investor awareness services and programs are designed to help small-cap companies communicate their investment characteristics. Sideways Frequency, Hugealerts.com, Tradingwire.comand their investor awareness services include the preparation of a research profile(s), multimedia marketing, and other awareness services based on the publicly available information of our clients and prepared by our partners. As such, our opinion is neither unbiased nor independent, and you should consider that when evaluating our statements regarding Metalla Royalty and streaming LTD (NYSE:MTA).

Besides the report you just grabbed, you’ll start receiving our free daily newsletter packed with:

Market Headlines: Business and equity stories guiding the market move.

Member-Only Analysis: Breakout stock reports and trend insights.

Ready-to-Use Ideas: Partner-sourced opportunities to explore.

To access your new report, tap the button below.Get the Report

P.S. Shoot us a quick “hey” to avoid spam filters. To ensure our emails stay in your inbox, follow the whitelisting instructions.

Information, charts, or examples contained in this email are for illustration and educational purposes only and not for individualized investment management. This message contains commercial elements, such as advertising and partner offers for which we may receive affiliate compensation.

If you wish to no longer receive these offers, click on the unsubscribe link at the bottom of this email. Past performance is not indicative of future results. For these reasons, we strongly suggest trading in a DEMO/Simulated account.

The information provided by us is for educational and informational purposes only. We make no representations or warranties concerning the products, practices, or procedures of any company or entity mentioned.

2967 Dundas St. W. #990, Toronto, ON M6P 1Z2 | 917.672.7040

This information is disseminated on behalf of Metalla Royalty & Streaming.

*MTA* Shows Signs of life at the open Runs then pulls back a bit BUT…

The post market ticker tape is back over $8.00…

We’re gonna keep this one going. Gold Was down but this was Up!!

there’s more unfolding to this story.. We can feel it!

So here we go!

ROUND 2 Starts tomorrow!

*NYSE:MTA*

and this still looks GOLDEN (6 month chart)

Full report below compensation in the disclaimer.

Metalla Royalty & Streaming (MTA): A High-Margin Gateway to Strong Gold, Resilient Silver, and Copper’s Structural Supply Crunch!

MTA is Leveraged Exposure to Record Gold, Surging Silver, and Copper’s Structural Supply Crunch — Without the Operational Risk of Mining!

Greetings All,

Gold has reasserted itself as a monetary anchor in an era defined by inflation persistence, sovereign debt expansion, and central bank accumulation. Silver’s dual role as both a store of value and a critical industrial input is amplifying upside pressure as renewable energy and electrification demand accelerates. Copper, meanwhile, is increasingly viewed as a strategic metal essential to energy security, electric vehicles, and next-generation infrastructure—just as new supply struggles to come online.

Within this backdrop, companies that can offer leveraged exposure to all three metals—without the capital intensity and operational volatility of mining—stand out.

Metalla Royalty & Streaming (NYSE: MTA) is emerging as one of those differentiated platforms.

A Royalty Model Built for Margin Expansion

MTA operates a royalty and streaming model, meaning it provides capital to mining operators in exchange for a percentage of future production or revenue. It does not operate mines. It does not bear sustaining capital costs. It does not face labor disputes, environmental liabilities, or cost overruns!

Instead, itreceives top-line exposure to metal prices and production growth.

In a rising price environment—especially one where cost inflation pressures miners—this model can produce expanding margins and scalable cash flow. As production increases across its underlying assets, revenue can grow without proportional increases in expenses. That structural advantage becomes particularly powerful during strong commodity cycles like the one that has been unfolding. Gold and silver hit record highs in early 2026.

A Clear Financial Inflection Point

The third quarter of 2025 marked a defining milestone. MTA reported its first-ever profitable quarter, with revenue more than doubling year-over-year to $4 million and net income turning positive.

Management characterized the quarter as a “step-change” moment—signaling that the company’s portfolio has reached the scale necessary to generate sustainable earnings.

This transition from portfolio builder to cash-flow generator is critical. Royalty companies often require years of disciplined asset accumulation before meaningful earnings materialize.

With profitability now established and multiple development assets advancing toward production, MTAappears to be entering a new phase of financial maturity.

Diversified Exposure Across Gold, Silver, and Copper

MTA’s portfolio includes approximately 100 royalties spanning producing, development, and exploration-stage assets across gold, silver, and copper.

This diversification reduces reliance on any single project while embedding multiple pathways to upside through mine expansions, restarts, feasibility updates, and exploration success.

Its exposure aligns closely with the dominant macro forces of 2026.

Gold’s surge reflects monetary hedging and central bank demand. Silver’s breakout is supported by accelerating industrial usage in solar and electrification. Copper faces projected structural supply deficits as electric vehicles, renewable infrastructure, and AI-driven data centers expand globally.

By holding royalties across all three metals, MTA captures both precious-metal monetary demand and base-metal industrial growth.

Built-In Catalysts Without Additional Capital Risk

A distinguishing feature of the royalty model is perpetual optionality. As operators advance projects, expand capacity, extend mine lives, or discover additional resources, the royalty holder benefits automatically—without investing incremental capital.

MTA’s portfolio includes numerous near-term catalysts: mine restarts, production ramp-ups, staged expansions, permitting milestones, and construction decisions across multiple jurisdictions. Each development has the potential to increase attributable production and royalty revenue, reinforcing the company’s ability to compound cash flow over time.

Institutional Validation and Strategic Capital

Another noteworthy development has been institutional interest. Public disclosures revealed that affiliated entities of Tether collectively hold approximately 8.9% of MTA’s outstanding shares.

As one of the largest physical gold buyers in recent quarters, Tether-linked capital entering the royalty space highlights a broader convergence between digital liquidity and hard-asset exposure.

While the investment remains passive, the presence of a well-capitalized and globally recognized financial player adds visibility and may signal confidence in the long-term thesis surrounding precious metals and diversified royalty platforms.

Why Streaming and Royalties Can Outperform Traditional Mining in Volatile Commodity Cycles

Unlike traditional mining companies, royalty and streaming businesses do not operate mines, manage labor forces, fund sustaining capital, or absorb cost overruns.

Instead, they provide upfront financing to operators in exchange for a percentage of future production (royalties) or the right to purchase metal at predetermined, discounted prices (streams).

This structure allows them to maintain exposure to rising gold, silver, and copper prices while avoiding many of the operational risks that can erode margins during inflationary periods.

When energy, labor, or equipment costs rise, miners feel the pressure directly—royalty and streaming companies generally do not. As production grows or metal prices increase, their revenue can scale with minimal incremental expense.

The Bottom Line

The metals breakout seen in early 2026 was driven by monetary instability, industrial transformation, and strategic de-risking from concentrated supply chains. Gold’s record highs, silver’s industrial acceleration, and copper’s tightening structural supply picture together form a powerful macro backdrop.

Within this environment, Metalla Royalty & Streaming (MTA) offers leveraged exposure to all three metals through a diversified, high-margin royalty model that minimizes operational risk while maximizing upside participation.

With its first profitable quarter behind it, a deep pipeline of catalysts ahead, and growing institutional attention, MTA appears increasingly positioned to benefit. Start your research!

Disclaimer

Hugealerts.com and Tradingwire.com are owned by Sideways Frequencey LLC (“Sideways Frequency”). Press releases, research reports, company profiles and other investor relations materials, publications or presentations, including web content (investor awareness services) released by Hugealerts.com and Tradingwire.com are based on publicly available data obtained from sources we believe to be reliable but are not guaranteed as to accuracy and are not purported to be complete. As such, the information should not be construed as advice designed to meet the particular investment needs of any investor. Furthermore, some of the content contained in our publications and websites may contain forward-looking statements found in information made publicly available by the companies we highlight. This forward looking information fits within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 including statements regarding future possible events, expected continual growth of a company, the potential value of its securities, and look forward in time which include everything other than historical information, involve risk and uncertainties that may affect a company’s actual results of operation. We therefore strongly encourage that you visit and review any and all financial information made publicly available by highlighted companies. Any opinions expressed in Hugealerts.com and Tradingwire.com reports, company profiles, or other investor relations materials and presentations are subject to change, are expressed and given as of the date of publication, and we disclaim any obligation to advise you of any change in any information contained herein. The information contained herein is not intended to be used as the basis for investment decisions and should not be construed as advice intended to meet the particular investment needs of any investor. The information contained herein is not a representation or warranty and is not an offer or solicitation of an offer to buy or sell any security. To the fullest extent of the law, Hugealerts.com,Tradingwire.com and their affiliates, specialists, advisors, and partners will not be liable to any person or entity for the quality, accuracy, completeness, reliability or timeliness of the information provided, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information provided to any person or entity (including but not limited to lost profits, loss of opportunities, trading losses and damages that may result from any inaccuracy or incompleteness of this information). Stock market investing is inherently risky. Hugealerts.com, Tradingwire.com and their affiliates are not responsible for any gains or losses that result from the opinions expressed in press releases, on this website, in its research reports, company profiles or in other investor relations materials or presentations that it publishes electronically or in print. We strongly encourage all investors to conduct their own research before making any investment decision. For more information on stock market investing, visit the Securities and Exchange Commission (“SEC”) at www.sec.gov. and/or the Ontario Securities Commission (“OSC”) at www.osc.gov.on.ca. and/or the British Columbia Securities Commission (“BCSC”) at https://www.bcsc.bc.ca/.

Income Disclosure

Sideways Frequency has been retained by Metalla Royalty and streaming LTD (NYSE:MTA).and has received cash compensation of $150,000.00 to perform promotional and advertising services for a limited time. This agreement has been ongoing since February 2026 and is related to the engagement of investor awareness services for Metalla Royalty and streaming LTD (NYSE:MTA).. Sideways Frequency,Hugealerts.com, Tradingwire.com and their partners and affiliates may buy and sell shares of securities or options and warrants of the companies mentioned on this website at any time.

Sideways Frequency LLC and its affiliates may buy and sell shares of securities or options and warrants of the companies mentioned in this publication or website at any time but are not and will not at any time become affiliates or owners of more than 5% of the issued and outstanding stock of the highlighted companies.

Sideways Frequency and its beneficial owners and affiliates, including Hugealerts.com and Tradingwire.com do not own any shares in Metalla Royalty and streaming LTD (NYSE:MTA).

Investor awareness services and programs are designed to help small-cap companies communicate their investment characteristics. Sideways Frequency, Hugealerts.com, Tradingwire.com and their investor awareness services include the preparation of a research profile(s), multimedia marketing, and other awareness services based on the publicly available information of our clients and prepared by our partners. As such, our opinion is neither unbiased nor independent, and you should consider that when evaluating our statements regarding Metalla Royalty and streaming LTD (NYSE:MTA).

I’m thrilled to see you’re all signed up for FutureProof 2026.

The predictions I share at the event will no doubt feel very shocking.

You’re going to witness how fast the fate of the world’s biggest AI companies can turn around and wipe out virtually all the wealth they have created over the past three years.

The good news is that I’ll be sharing specifics on where I believe this $10 Trillion wealth transfer will move next — down to the names and tickers of specific stocks.

But…

There’s one important step I recommend you take immediately…

Upgrade to a FutureProof 2026 VIP right now, if you haven’t done so already.

This is the best way to guarantee you don’t miss any of the bonus content and research I release before going live with the biggest prediction of my career on Wednesday, March 18th.

And if you upgrade to a VIP attendee now, you’ll gain access to an exclusive research report I just finished called Meet the Mag 7 Killers: 3 Heavy Assets Crushing AI Hyperscalers in 2026.

Inside this report, you’ll get a list of three of my favorite stocks that are significantly outperforming the Mag 7 so far in 2026.

These “asset heavy” companies are a bellwether of the regime change that I predict will kick off in earnest when the $10 Trillion Market Shock hits on April 24th.

Mag 7 Killer #1: One of America’s most prolific energy producers firmly positioned to fuel America’s AI buildout…

Mag 7 Killer #2: Offshore driller whose blockbuster merger announcement could create the most powerful deep-sea drilling company in history…

Mag 7 Killer #3: The company digging up the one material every AI data center on earth cannot be built without.

**IMPORTANT:This research report is only available to our VIP registrants.**

This ad is sent on behalf of Banyan Hill Publishing. P.O. Box 8378, Delray Beach, FL 33482.Advertising Disclosure: This email contains paid advertisements. This email is from our associates at Banyan Hill.

Legal Entity Information: Investing Ideas Daily is owned and operated by Darwin Investor Network, a DBA of The Darwin Agency, Inc.

Disclaimer: Nothing in this email should be considered personalized financial advice. Always conduct your own due diligence when investing. We urge you to read our full disclaimer by clicking on the terms of use link below.

Unsubscribe: You are receiving this email as part of your complimentary subscription to the Investing Ideas Daily E-Letter. If you would like to unsubscribe, you can do so by clicking on the unsubscribe link below.Darwin Investor Network 2319 N Andrews Avenue, Fort Lauderdale, FL 33311 support@investingideasdaily.com | 1-800-496-9838Investing Ideas Daily | Privacy Policy | Terms of Use Unsubscribe | View Online

That’s the number NVIDIA CEO Jensen Huang put on the table at this year’s NVIDIA GPU Technology Conference known as GTC. He wasn’t referring to the market cap of his company, which is far beyond that level. He was referring to the amount of revenue he expects NVIDIA will earn from 2025 to 2027.

And that implies NVIDIA is on a path to generate roughly $500 billion in 2027 alone. Only Walmart (WMT) and Amazon (AMZN) have more annual sales than that.

This is an extraordinary figure. And the reason for this is simple… AI-driven demand continues to increase, just as we’ve been predicting at Brownstone Research.

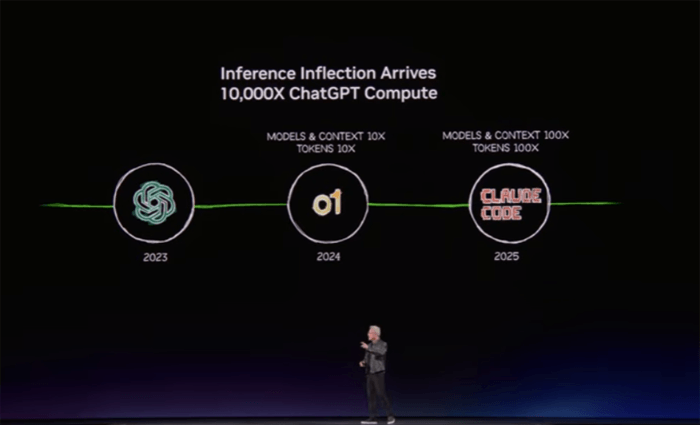

Since the release of ChatGPT in late 2022, NVIDIA estimates that token generation demand per AI task has increased 10,000x. At the same time, overall model usage has surged 100x. Together, that implies a 1,000,000x increase in compute demand in just a couple of years.

Huang doesn’t believe this is going to slow down either. Neither do we. Frontier AI model companies are clamoring for more compute. He said:

It’s the feeling that OpenAI has, it’s the feeling that Anthropic has. If they could just get more capacity, they could generate more tokens, their revenues would go up, more people could use it, the more advanced, the smarter the AI could become.

We are now at that positive flywheel system, we have reached that moment… the inference inflection has arrived.

It’s important to understand this quote. OpenAI, Anthropic, Google, xAI and Meta are all operating with the same mindset. If they can access more compute, they can scale their products, improve performance, and generate more value.

That’s why Huang described this moment as an inflection point. The industry has entered a self-reinforcing loop where demand for compute feeds on itself. The more capacity that comes online, the more it gets used.

The Next Wave Is Even Bigger

What most investors still don’t appreciate is what comes next. We are moving beyond simple prompts and responses and into the era of autonomous AI agents.

These systems don’t just answer questions. They run workflows, write code, analyze data, and make decisions. And importantly, they operate continuously.

With the release of OpenClaw – the open-source agentic AI platform that Jeff’s been covering in The Bleeding Edge – it’s now easier than ever for individuals to program their own AI agents that will continuously do work for them.

Now OpenClaw is designed to run locally on a computer, but the reality is that meaningful workloads will still be pushed into hyperscale environments where compute can scale efficiently.

This shift matters because persistent, always-on AI systems consume far more compute than the first wave of chatbot-style interactions. Which means the next surge in demand will be even greater.

And it’s not just OpenClaw. Another leading player in AI software, Perplexity, just recently launched Perplexity Computer, which has the ability to leverage all frontier AI models. Rather than being open-sourced like OpenClaw, Perplexity Computer has been productized with platform security and ease of use in mind. No programming skills are required at all.

The Problem We Can No Longer Ignore

This brings us to the real constraint… Not chips. Not software. Not capital.

Electricity.

If NVIDIA hits the scale Jensen Huang is signaling, we’re no longer talking about incremental growth in data center capacity. We’re talking about a step-function increase in global power demand.

Let’s walk through what that actually looks like.

Assume NVIDIA reaches roughly $500 billion in annual revenue by 2027, driven primarily by its next-generation Vera and Rubin systems, alongside current Grace and Blackwell platforms.

At that scale, we’re looking at deployments on the order of millions of GPUs.

Using NVIDIA’s NVL72 architecture as a baseline, each rack contains 72 GPUs and 36 CPUs. To support that level of revenue, we arrive at roughly 125,000 racks – about 9 million GPUs – deployed globally.

Now consider the power draw. Each of these racks consumes approximately 200 kilowatts. Multiply that across the full deployment, and we’re already at 25 gigawatts of electricity demand just to run the compute hardware.

But that’s only part of the story.

Modern AI data centers require advanced cooling systems, networking infrastructure, and redundancy layers. When we account for total facility overhead using a typical power usage effectiveness (PUE) factor of 1.3, total demand rises to roughly 32 to 33 gigawatts.

And that’s just NVIDIA. Once we factor in AMD systems and the growing use of custom application-specific semiconductors for AI by hyperscalers, total demand quickly approaches 60 to 65 gigawatts.

That’s the true scale of what’s coming.

A Growing Gap Between Supply and Demand

And this is where the problem becomes clear.

A majority of these AI data centers are being built on U.S. soil. Last year, the United States added about 53 gigawatts of new power generation capacity, the highest level since 2002. On the surface, that sounds like progress.

But it’s not nearly enough. Even more concerning is what kind of power we’re adding.

According to the EIA, roughly 65% of new capacity is coming from solar and wind, both of which are intermittent energy sources. Another 28% is going toward battery storage, which helps manage variability but does not generate new electricity.

When we strip all of that out, only about 7% of new capacity – roughly 6.5 gigawatts – is true baseload power capable of running continuously, the kind necessary to power AI factories.

And we’re adding only a fraction of that in reliable, always-on power.

Even under the most optimistic projections, we’re nowhere close to closing that gap. And historically, actual buildouts fall well short of what’s planned.

Yes, we can attempt to reroute intermittent energy toward less critical use cases and reserve baseload power for AI. But that’s a temporary fix, not a scalable solution.

New Nevada court filing reveals Tesla may be next in line for an Elon Musk Mega Merger. Last time Tesla merged well positioned investors saw 30x gains. Don’t miss out. Legendary tech angel investor shares the details in this short briefing. Click now to avoid being left behind.

Tech Bros thought they were gods. That AI would appear if they commanded it. But the physical world doesn’t care about what Silicon Valley wants. And the $635 billion they’re throwing at it can’t change reality. What’s coming next in the markets is a full-on Regime Change – a violent reorganization of market winners and losers. Trillions will flee the Mag 7. And the money will find its way to a surprising new class of companies… Tomorrow at 1 p.m. ET, Eric reveals exactly where, including 15 free stock tickers to watch. Instantly reserve your free spot at FutureProof 2026 by clicking here.

The Biggest Bottleneck in AI

New power is the biggest hurdle that Jensen Huang and NVIDIA face in realizing their lofty revenue targets. And this problem will get worse every year. NVIDIA’s growth doesn’t stop in 2027. Not even close.

Wall Street is already projecting another 20% growth in 2028, pushing revenue over $600 billion. If I were to make a bet, I’d take the over on that number.

And every incremental dollar of that growth means more electricity. This is the constraint Jensen is solving for.

He needs more than just faster chips. He needs a new deployment model for compute itself.

This is what made one of the most important announcements at GTC so easy to miss.

NVIDIA Looks Beyond Earth

Huang didn’t just talk about next-generation systems for terrestrial data centers. He introduced something entirely different.

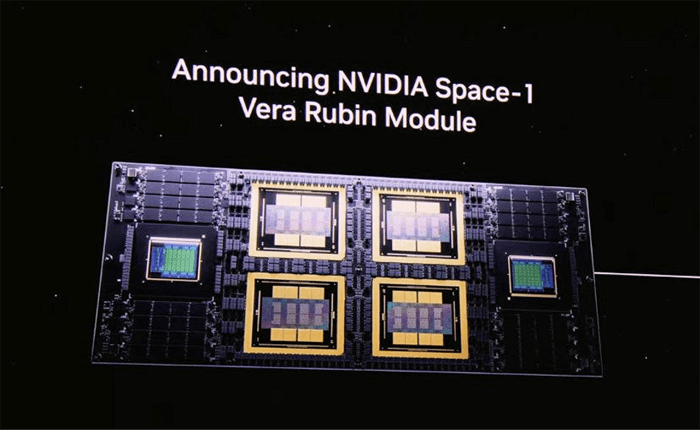

The NVIDIA Space-1 Vera Rubin module.

NVIDIA GTC Presentation | Source: NVIDIA

At first glance, it looks like a compact version of NVIDIA’s terrestrial GPU architecture. As we can see, the architecture pairs two Rubin GPUs with a single Vera CPU on a highly specialized board.

But that misses the point entirely. This system wasn’t designed for Earth. It was designed for orbital AI data centers.

Operating in space introduces a completely different set of challenges. Radiation constantly interferes with electronics, causing errors that can crash traditional systems. Instead of relying on slower, hardened chips, NVIDIA engineered around the problem.

The system runs duplicate computations across paired GPUs and compares the results in real time, instantly correcting any discrepancies. Combined with advanced error correction at the memory level, this creates a highly resilient architecture capable of operating in one of the harshest environments imaginable.

And despite those constraints, performance is staggering. The module delivers a 25x leap over prior generations, enabling real-time AI inference, autonomous decision-making, and even orbital training of advanced AI models.

A specific launch date has not yet been announced. But NVIDIA said six companies are already using its accelerated computing platforms to power next-generation space missions.

Contenders in the Space-Based Data Center Buildout

This is also why Elon Musk is looking towards outer space to expand AI data centers with his constellation of one million satellites.

In our latest issue of The Near Future Report, we said:

On Earth, building new power plants takes years. Transmission lines take even longer. Regulators slow everything down. Communities fight new infrastructure. And even when projects are approved, data centers compete for the same finite grid capacity.

But in low Earth orbit, those constraints disappear.

Approvals are easier to obtain. There is no NIMBY-ism fighting the construction. And no waiting years for utility hookups. Each AI satellite launches with its own power generation attached.

In space, solar panels generate about five times more electricity than they do on the ground. And they operate nearly 24 hours a day. Low Earth orbit (LEO) has no clouds, no inclement weather, and no night cycles when in sun-synchronous orbit.

That’s why Musk is thinking beyond terrestrial data centers.

And we are confident that Musk will achieve this.

Once Starship drives launch costs down toward $100 per kilogram – which we believe is achievable by 2028 based on the current trajectory – the economics of compute begin to shift in a way most investors aren’t prepared for.

At that point, orbital AI data centers will be the most cost efficient way to generate AI compute.

No land constraints. No grid bottlenecks. No cooling limitations. No permits to worry about. Just scalable, limitless free energy infrastructure operating in an environment purpose-built for exponential growth.

This is the moment the entire cost curve flips. And Elon Musk sees it coming.

That’s exactly why he’s now positioning SpaceX for a public offering. He wants to raise capital to accelerate his much larger vision.

Building orbital data centers isn’t just about launching satellites. It requires an entirely new supply chain from launch infrastructure to satellite components to advanced solar panels. And potentially even in-space manufacturing to power systems and next-generation compute architectures.

And Musk intends to build it all. This is a part of his AI masterplan.

Most investors are still focused on GPUs, software, and cloud providers. But the real shift is happening one layer deeper, at the infrastructure level.

More to come…

Regards,

Nick Rokke Senior Analyst, The Bleeding Edge

P.S. Hi, Jeff’s managing editor here. If you want to learn more about this, Jeff recently put together a detailed presentation breaking down the opportunity in the new space economy and the ensuing infrastructure buildout…

He covers how this transition is unfolding, why it’s happening now, and most importantly, how to identify which companies are positioned to benefit as the data center buildout moves beyond Earth.

It’s important to position yourself now because the transition is already underway. And the biggest gains are made early, before the majority of investors realize the magnitude of this shift.

To ensure our emails continue reaching your inbox, please add our email address to your address book.

This editorial email containing advertisements was sent to pahovis@aol.com because you subscribed to this service. To stop receiving these emails, click here.

Brownstone Research welcomes your feedback and questions. But please note: The law prohibits us from giving personalized advice.

To contact Customer Service, call toll free Domestic/International: 1-888-512-0726, Mon-Fri, 9am-7pm ET, or email us here.

Here’s your free report on the 3 AI stocks poised to join MAG 7’s trillion-dollar club:

If you feel you have received this email in error, please click here to unsubscribe from the Smart Money and InvestorPlace Digest e-letters, as well as marketing from InvestorPlace.

In addition to this free report, you’re now also a member of the free Smart Money newsletter. Nearly every Tuesday, Thursday, and Saturday, I’ll hare insights on the latest market “megatrends,” how to hedge against inflation, which stocks you should avoid, and more.

You’ll also begin receiving the InvestorPlace Digest, a daily e-letter where Jeff Remsburg shares critical analysis to help you navigate the turbulence in today’s markets.

Before you read up on those companies, I want to warn you about an even more urgent trend unfolding in the markets…

While everyone’s celebrating a tech stock boom that feels unstoppable, I’m seeing massive warning signs that could wipe out millions of portfolios in the coming months.

I’m telling investors to SELL these three “too big to fail” stocks immediately:

My track record on these warnings speaks for itself.

When I said, “Sell Twitter, Buy Ormat,” Twitter crashed 64% while Ormat soared 100%.

When I called “Sell Lennar, Buy Valero,” Lennar lost half its value while Valero tripled.

That’s why I’ve put together a must-see video with 7 new “Sell This, Buy That” recommendations that could help safely steer your course in the markets.

In this urgent video presentation, you’ll discover:

✓ Why NVIDIA’s AI chip dominance could be about to crumble (and why there’s a better alternative to investing in chips altogether)

✓ Why you should swap out Bezos’ ecommerce behemoth for an unknown retailer that could be more “like buying Amazon in 2005”

✓ Tesla’s fatal robotics flaw (and the little-known company already outshining Tesla in this space)

We’re entering a strange period I call “The Age of Chaos”, where knowing which stocks to buy and which stocks to avoid will become more crucial than ever.

It’s an age where investing missteps could turn millionaires penniless virtually overnight.

And where savvy stock pickers stand to multiply their wealth by 10X or more.

It’s time to upgrade your stocks now for a shot at bigger, stronger wins.

Why Mastercard and Visa Are the Definition of Forever Stocks

Written by Jordan Chussler. Article Posted: 3/14/2026.

Key Points

The financials sector has lagged the S&P 500 this year, but two payment processing giants continue to deliver the kind of margins and earnings consistency that define long-term holdings.

Despite recent sector-wide struggles, Visa and Mastercard function as a veritable duopoly, controlling over 90% of payments outside of China.

Visa hasn’t missed on earnings in 10 years, while Mastercard has secured 21 consecutive quarterly beats.

After returning nearly 23% annually over the past two years, the financials sector has struggled this year. With a year-to-date loss of around 9%, the cohort ranks last among the S&P 500’s 11 sectors.

Zoomed out, however, many companies in the sector remain core holdings for buy-and-hold investors.

With high-quality growth stocks harder to find, two legacy firms in global payment processing and digital payments continue to deliver profit margins and business characteristics that make them candidates for “forever” stocks.

Why Digital Payment and Payment Processors Make for Good Forever Stocks

Payment processors typically enjoy higher profit margins than many other industries because of high-volume demand, extensive automation and technology-driven models that keep marginal costs per transaction very low.

The industry is also positioned for strong growth. Industry analytics firm Grand View Research estimates the global payment processing solutions market—valued at nearly $48 billion in 2022—will grow at a compound annual growth rate (CAGR) of 14.5% through 2030, reaching nearly $140 billion. Grand View also forecasts the digital payment market, valued at more than $114 billion in 2024, will expand at a 21.4% CAGR through 2030 to exceed $361 billion.

Although that growth and attractive gross margins might suggest the space is crowded, two of the biggest names in the industry still operate in a near-duopoly, handling more than 90% of credit card and digital payments processed outside China. With roots going back to the mid-1900s, these firms control much of the payment infrastructure and standards, which helps them set fees, limit competition and preserve strong margins.

Although challengers such as Block (NYSE: XYZ), with Cash App, and PayPal (NASDAQ: PYPL), with Venmo, seek to disrupt the market, none fit the “forever stock” profile better than the two companies below.

Mastercard: The $450 Billion Market Cap Company Focusing on Tech Integration

Since Michael Miebach became CEO of Mastercard (NYSE: MA) in 2021, management has focused on expanding tech platforms, supporting cross-border commerce and developing services that help clients reduce fraud, streamline payment flows and extract insights from payments data.

That strategy helped Mastercard report record revenue and net income in 2025. Revenue of nearly $33 billion represented a year-over-year (YOY) increase of more than 16%, and net income of almost $15 billion grew by a similar margin.

That profitability was driven in large part by a 100% gross margin throughout 2025, enabled by tech integrations and a minimal cost of goods sold such that quarterly gross profit closely matched quarterly net revenue.

For investors, that has translated into consistent earnings performance. The last time Mastercard missed an earnings estimate was Q3 2020 after the onset of the COVID-19 pandemic; since then it has recorded 21 consecutive quarterly earnings beats.

Most recently, Mastercard reported Q4 2025 EPS of $4.76, roughly a 25% YOY increase. Analysts expect earnings to grow about 17% over the next year, from $15.91 to $18.61 per share.

At the same time, Mastercard has been embracing broader fintech trends, transitioning from a traditional payments network toward an AI-driven, software-focused enterprise that emphasizes enhanced security, simplified B2B transactions with virtual cards and agentic AI tools.

Additionally, Mastercard pays a dividend. While its yield is modest (currently 0.69%), the company has raised its payout for 13 consecutive years, maintains a sustainable dividend payout ratio of 21.07%, and has a five-year annualized dividend growth rate of 13.70%.

Visa: Evolving and Adapting Since 1958

Visa (NYSE: V) operates a network-based model that lets partner banks and other financial institutions issue branded payment products while Visa focuses on infrastructure, standards and technology integration.

Like Mastercard, Visa is rapidly integrating fintech capabilities, pursuing AI-driven solutions and exploring blockchain-based settlement with the aim of shifting from traditional card transactions toward more flexible, digital-first experiences.

That approach helped Visa post record revenue and net income in 2025: revenue of about $40 billion, an 11% YOY increase, and net income of nearly $20 billion.

Visa’s consistency on earnings is notable. It hasn’t missed an earnings estimate in the past 10 years—in that span it met expectations twice and beat EPS estimates 38 times.

Much of Visa’s resilience is supported by its near-83% gross profit margin in 2025, in line with its long-term average.

Like Mastercard, Visa pays a modest dividend (current yield 0.87%). Its payout ratio is a healthy 25.14%, its five-year annualized dividend growth rate is 14.48%, and the company has raised its dividend for 17 consecutive years.

Thank you for subscribing to DividendStocks.com’s daily newsletter for dividend and income investors that covers ex-dividend stocks, new dividend declarations, dividend stock ideas, and the latest market news.

This email content is a paid advertisement for The Oxford Club, a third-party advertiser of DividendStocks.com and MarketBeat.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here

If you have questions or concerns about your account, feel free to email MarketBeat’s South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from DividendStocks.com, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights protected. 345 North Reid Place, Suite 620, Sioux Falls, S.D. 57103. United States of America..

Trouble viewing email? Click here You are subscribed to this newsletter as: peterhovis@icloud.com

FILM SCHEDULELEARN MOREMORE PROMOTIONSStep into the energy of the Phoenix Film Festival, where each spring brings a surge of bold films, fresh voices, and conversations that linger long after the credits roll. The lineup blends indie discoveries, thoughtful features, and films before they’re released in theatres, with opportunities to hear directly from the filmmakers behind them. It’s an easygoing way to catch something new, connect with fellow movie lovers, and enjoy eleven days at the movies.

Along the way, you’ll find special events, panel discussions, and some fun parties. Stay for a single screening, make a weekend of it, or turn it into a full movie getaway—it’s a simple, memorable way to experience storytelling at its finest.