I was born on 6 August 1956 in San Francisco, California to Janet and (the late) Richard Hovis.

I grew up in Santa Monica, California where I attended elementary, junior high school, and high school (graduating in 1974), in addition to involvement in sports and recreation (Little League +, the Boy’s Club ++). Further, it was in elementary school – St. Augustine’s By-the -Sea Parish School that I found, and made the choice to truly journey with God.

I attended Arizona State University from 1974 to 1977 – seeking to become an architect, however, I was not accepted, and, as such, I graduated with a Liberal Arts degree.

Upon graduation from Arizona State University, I attended Cal Poly San Luis Obispo and studied City and Regional Planning at the Master’s level. I successfully completed one (1) year in a two (2) year program – I did not complete the Master’s degree in City and Regional Planning – due to personal reasons.

I returned to Santa Monica where I started (October 1979) my career as graphic designer with Exxon Company, USA. I spent five years with Exxon Company, USA.

While working with Exxon Company, USA I was accepted into architectural school – Sci-Arc in Southern California, however, I did not attend preferring to stay with Exxon..

In 1982 I married Laura Flosi and in April 1983 we had our one and only child – Lauren Alain Hovis – a gift from God.

We moved to Phoenix, Arizona in 1984 from Los Angeles, where I went to work as a graphic designer with Kitchell CEM (from 1985 -1987).

From 1987 – 1995 I was an independent contractor, and a registered representative in mortgage finance, financial management, graphic design, and drafting.

Further, I attended the University of Phoenix and successfully obtained a Master’s in Business Administration (MBA) in 1982.

I was also a member of the Scottsdale Jaycees, where I became very involved in community events and projects.

In 1994, I accepted a cartography position with the Defense Mapping Agency in Reston, Virginia. As such, I relocated from Phoenix to Reston.

In 1998, I was accepted and worked as a Visual Information Officer with the Central Intelligence Agency. In 2002, I worked as a Support Officer until my retirement (due to a need for shoulder surgery) in September 2018.

Away from my Federal Government service, I have been involved in various organizations and activities in Northern Virginia.

In November of 2011, I married Rebecca Ouellette in Santa Monica, California. I reside in San Tan Valley, AZ with my two hamster - Jess and Timothy, our fish, our lizard - RJ Lizard., and our cats - Pearl and Grey.

As to hobbies, I enjoy playing sports, attending sporting events, mentoring individuals from financial management to hamsters, building models, photography, travel, multimedia design, managing partner for RJ Hamster, and jazz – smooth jazz to a samba or a bossa nova.

Love and God Bless,

Peter – aka RJ Hamster Jo hi

Quick thing — I get asked a lot about where to start if you’re trying to cook more at home but feel overwhelmed. Honestly? Start with whatever you’re already craving. That pasta dish you always order out, the cookies your grandmother used to make, the soup you wish you had in your freezer right now. When you’re cooking something you actually want to eat, you pay closer attention, and that’s when the real learning happens. There’s something about feeding yourself something delicious that makes all the chopping and stirring worth it.

I’ve been working on a bread recipe for the past three weeks. Thought I had it figured out after the second try. Classic mistake. Turns out the hydration was off, and I didn’t account for how much humidity affects the dough in my kitchen. Each loaf taught me something new — one was too dense, another didn’t rise enough, and one actually turned out perfect but I forgot to write down exactly what I did. But that’s the thing about cooking — you learn more from the recipes that don’t work perfectly than the ones that do. The bread that took me five tries taught me more about gluten development than any cookbook ever did. I’ll probably share it once I can replicate that perfect loaf consistently. Or maybe I’ll just call the imperfect ones “rustic” and move on.

I try to keep these emails focused on recipes that actually fit into your life, not just things that look pretty in photos. It’s how I’d cook if you were in my kitchen and we were figuring out dinner together. Just one solid recipe, explained clearly enough that you could make it this weekend without any confusion. Some weeks that’s an elaborate layer cake, other weeks it’s just a better way to roast vegetables or a marinade that actually makes chicken interesting. Both matter if they make your meals better. I’ve never believed in the “right way” to cook most things — there’s usually just the way that works for your kitchen, your schedule, and what you have in your pantry right now.

Every recipe I share comes from my actual kitchen — things I’ve made, adjusted, burned, and occasionally made again even better the second time. I don’t share recipes for techniques I haven’t used or ingredients I haven’t tasted myself. That’s partly why these emails don’t come out on some rigid schedule. I’d rather send you something I’ve tested thoroughly than fill your inbox with untested ideas just to stay consistent. Sometimes that means I’m quiet for a bit while I’m actually in the kitchen working through a recipe three or four times. I think that’s fair.

If you ever have questions about a recipe or need help troubleshooting something, just hit reply. I usually respond within a day or two, and I genuinely like hearing what people are cooking. Sometimes your questions turn into the next recipe because I realize I glossed over an important step or assumed everyone knew a technique that’s actually not that common. Last month someone asked about the best way to caramelize onions without them burning, and I realized I’d been saying “cook until golden” in recipes for years without explaining that it takes a solid 30-40 minutes of patient stirring. Now I’m much more specific. Another reader asked about substitutions for eggs in baking, and that turned into one of my most-saved guides. The best recipes usually come from real questions people are actually asking.

Most of what I know came from making mistakes in my own kitchen. I’m not a professionally trained chef — I just started cooking because I wanted to eat well and couldn’t afford to eat out all the time. That perspective matters because I remember what it’s like to not know the “obvious” stuff that experienced cooks take for granted. I remember the first time I tried to make risotto and added all the liquid at once instead of gradually. I remember buying expensive vanilla beans and then not knowing how to properly scrape them. Those experiences stick with you, and they make you better at explaining things because you know exactly where people get confused.

Anyway, thanks for reading this. Hope your weekend cooking goes smoother than mine usually does, though honestly the messy experiments make for better stories. And if something doesn’t turn out perfectly, remember — it’s not a failure, it’s just research for the next attempt.

— Chloe

Please note, some content in this email may be sponsored. While I feature these offers, I do not verify their claims or specifically endorse the products. This email is provided for informational purposes only and is not intended as dietary, nutritional, or medical advice.

I encourage you to review any products or suggestions carefully and make choices that are right for you and your family.

Below is an important message from one of our highly valued sponsors. Please read it carefully as they have some special information to share with you.

This ad is sent on behalf of Paradigm Press, LLC, at 1001 Cathedral St., Baltimore, MD 21201.

Today’s editorial pick for you

Protect Your Portfolio with 3 High-Yielding REITs

Posted On Nov 19, 2025 by Chris Markoch

With market volatility wreaking havoc on your portfolio, you can always protect it with high-yielding REITs (Real Estate Investment Trusts). REITs are a way for retail investors like you and me to get exposure to real estate without having to become a landlord and all that comes with that.

With REITs, it’s all about the dividend. By law, a REIT is required to pay out a significant percentage of their earnings (typically around 90%) as dividends. That makes these a prime target for income-oriented investors.

That brings up another benefit of REITs, many come with high dividend yields. After all, you’re just not going to make the money you want in today’s low-yielding savings accounts. You’re lucky if you earn 0.40% these days. And many of these REITs have yields above that of long-dated Treasury bills, so you get both yield and liquidity.

If it’s dependable income you’re after, one of the best things you can do is invest in high-yield REITs. Here are three you may want to consider.

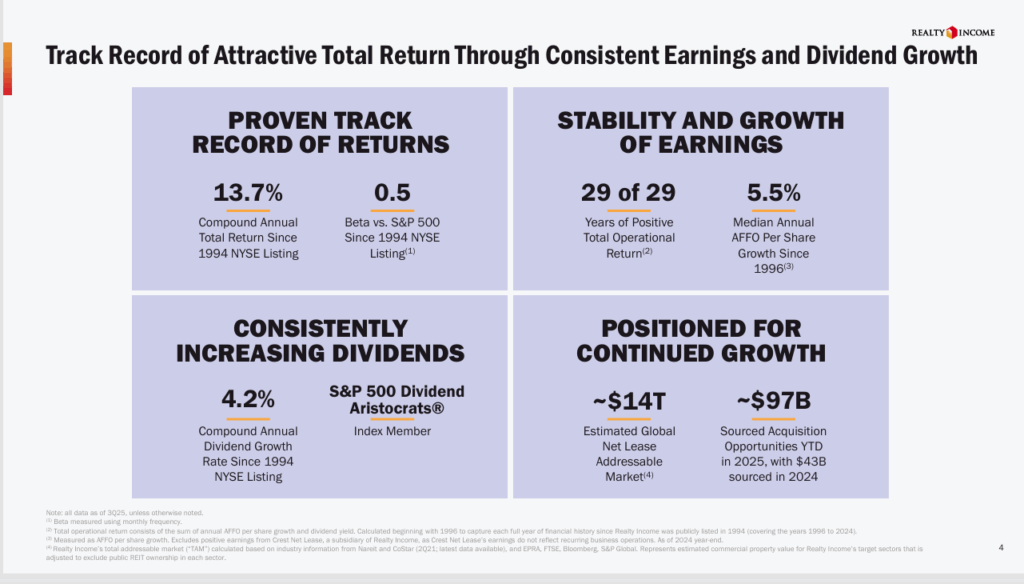

At the moment, with a yield of 5.64%, it just declared its 664th consecutive monthly dividend of $0.2695 per share, or an annualized amount of $3.234 per share, is payable on November 14, 2025 to stockholders of record as of October 31, 2025.

Making it even more attractive, Realty income is one of the biggest lease real estate investment trusts (REITs) you can buy. It also owns more than 15,600 properties, with a vast majority of that in the retail sector. In fact, some of its biggest tenants include 7-Eleven, Dollar General, Walgreen’s, Wynn Resorts, FedEx, BJ’s Wholesale Club, CVS, and Tractor Supply.

O stock is up about 6.3% in 2025, which is in line with its total return over the last three years. It also reflects the slowdown in the housing market. But you’re buying this stock for future growth. And at 13x forward earnings and with about 3.3% expected earnings growth, Realty Income may be ready to outperform in a rate-cutting environment.

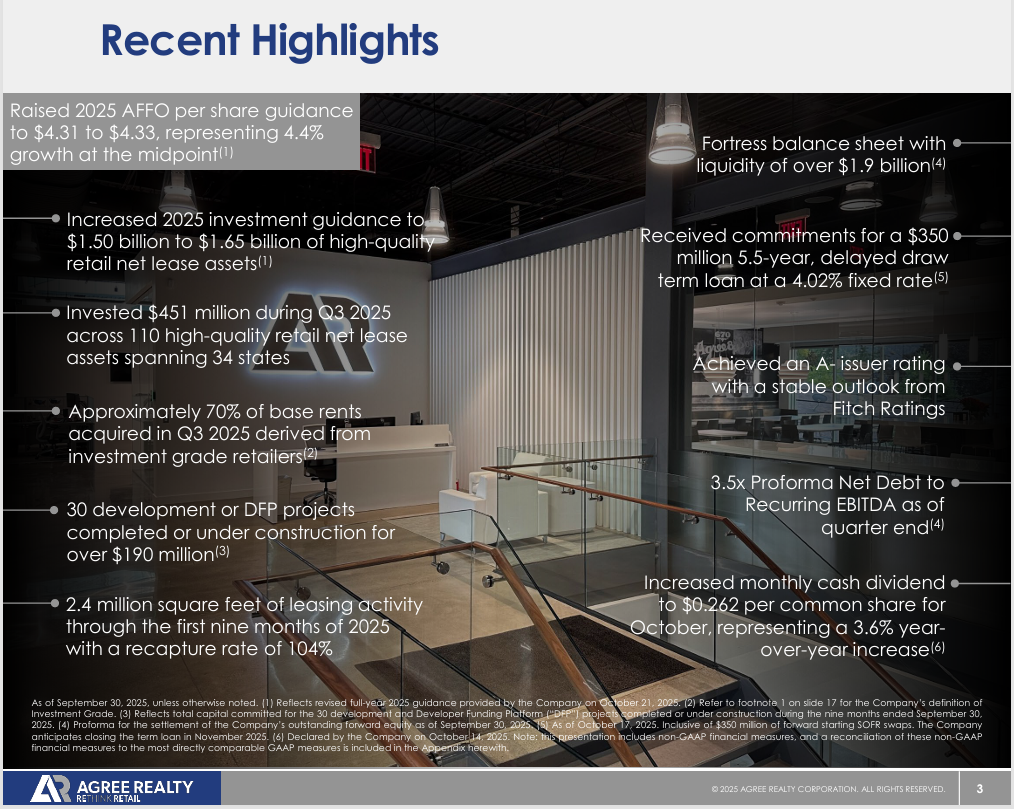

REITs to Buy: Agree Realty

With a yield of 4.26%, Agree Realty (NYSE: ADC) is a net lease REIT with a strong focus on retail. ADC just declared a monthly dividend of $0.262 per share, or an annualized dividend amount of $3.144 per share. The dividend is payable November 14, 2025, to stockholders of record at the close of business on October 31, 2025.

Some of its top clients include Tractor Supply, TJX Companies, Walgreen’s, Walmart, Dollar General, Best Buy, CVS, Hobby Lobby, and The Home Depot to name a few.

Like Realty Income, ADC stock is only up about 3.5% in 2025. However, the stock also has an attractive forward P/E ratio of around 17x and analysts project around 4% earnings growth in the next 12 months.

REITs to Buy:EPR Properties

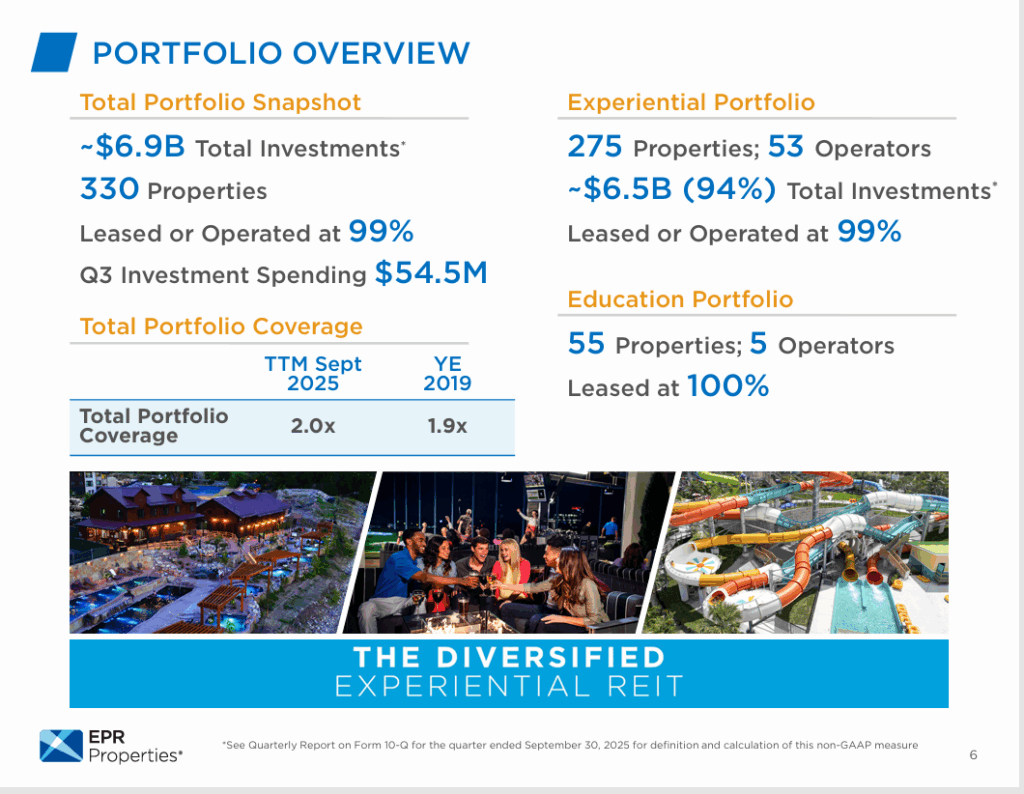

There’s also EPR Properties (NYSE: EPR), which yields 6.91% and invests in amusement parks, movie theaters, ski resorts, and other entertainment properties. That’s a reason why EPR stock is up about 15% in 2025. The experiential economy has still been lifting the broader economy. Lower interest rates may allow that trend to continue into 2026.

EPR Properties just declared a monthly cash dividend of $0.295 per share, which is payable October 15, 2025, to shareholders of record on September 30, 2025. This dividend represents an annualized dividend of $3.54 per common share.

EPR stock has an attractive forward P/E of around 10x earnings and analysts forecast about 2.3% earnings growth in the next 12 months.

This is a PAID ADVERTISEMENT provided to the subscribers of StockEarnings Free Newsletter. Although we have sent you this email, StockEarnings does not specifically endorse this product nor is it responsible for the content of this advertisement. Furthermore, we make no guarantee or warranty about what is advertised above.

Your privacy is very important to us, if you wish to be excluded from future notices, do not reply to this message. Instead, please click Unsubscribe.

StockEarnings, Inc 33 SE 4th St, Suite 100, Boca Raton, FL 33432 USA W: 877.6.STOCKS StockEarnings.com

You may have heard that Tesla is planning to launch a brand new product called “Optimus”.

Elon Musk called it “mind blowing” and has already launched his biggest ever insider buy of Tesla stock.

Others have dubbed it “terrifying”.

But whatever your views on Elon Musk and the seemingly inevitable rise of robotics, you absolutely need to know about a way you could make 10 times your money as Optimus launches, without ever buying a single share of Tesla.

See, I think almost everyone owns all the wrong stocks to profit from Optimus, which Elon Musk and Tesla insiders are racing to launch very soon.

All 10 of the biggest money managers in the world have followed my institutional firm’s work. That includes professionals from huge names like Goldman Sachs and JP Morgan.

And yet a lot of folks I talk to on Wall Street have the Optimus story all wrong.

Make no mistake: there’s no stopping Elon Musk right now – and his plans have huge implications for the stock market. Tesla may never trade at this price again.

And if you want to capitalize, there’s one stock I think needs to be on your radar right now.

I’d like to give you all the details today. And while my team has charged up to $100,000 to Wall Street for a single report on a situation like this…

Although modest, the results and outlook largely affirm analysts’ expectations and underscore the company’s solid cash flow and capital returns, which are supporting the stock.

The AI revolution is reshaping the investment landscape, and knowing where to place your bets is crucial. Our free report reveals the 10 top AI stocks that should be on your radar right now. Don’t miss your chance to get in on these high-potential tech plays.Download your free report today.

The takeaway is that headwinds persist, but this retail company is sustaining growth, maintaining margins, and building value for investors.

As a result, the stock is likely to revert to the high end of its existing trading range and could potentially set new highs in early to mid-2026.

Lowe’s Takes Share in Q3, Outperforms Competitor

Lowe’s posted a decent Q3 despite macroeconomic headwinds and a milder 2025 hurricane season. The company reported $20.81 billion in revenue, up 3.2% — outpacing competitor Home Depot by roughly 45 basis points, though revenue fell slightly short of consensus.

The growth was underpinned by a 0.4% comparable-sales increase (comps), also ahead of Home Depot, and by strength in services and the professional business. Services grew in double digits, and the professional segment is expected to accelerate from Q3’s solid levels thanks to recent acquisitions.

Margins were mixed but generally positive: gross margin widened, though gains were offset by higher operating costs.

The net result beat expectations: adjusted EPS of $3.06 rose 5.6% year over year, outpacing the 3.2% revenue gain and topping MarketBeat’s consensus by $0.11.

Importantly, cash flow remained sufficient to support the balance sheet and capital returns despite the recent acquisition, positioning the business for strength in 2026.

Guidance was mixed but ultimately investor-friendly. While it came in below consensus, the revisions reflect management’s improved confidence and broadly align with analysts’ forecasts, easing market concerns about capital return payments.

As of mid-November, the company’s dividend yield stands at an attractive 2.75% annually, complemented by share buybacks that further boost returns.

The company did not repurchase shares in Q3, allocating cash to the acquisition, but has reduced share count by more than 1.0% year-to-date and is expected to resume buybacks in coming quarters.

Analysts Forecast Robust Rebound for Lowe’s Stock

Analysts’ signals are mixed — cautious in parts — yet overall remain bullish. Recent price-target reductions still leave a consensus implying roughly 20% upside from the critical support level, and overall sentiment is pegged at Moderate Buy.

The Moderate Buy rating has been in place for over a year and shows no signs of faltering. The few analyst updates issued immediately after the release suggest the mixed trend will continue, but no change to the overall outlook is expected.

Institutional flows indicate investors are buying the November dip. Although activity has declined sequentially throughout the year, net institutional positioning remains bullish in every quarter, including the first half of Q4.

The Q4-to-date activity is noteworthy because it is poised to accelerate and may gain momentum now that results have been released.

Lowe’s Stock Confirms Support at a Critical Level

Lowe’s stock jumped about 5% after the Q3 release, rebounding from the prior day’s lows. The move confirms support at a key level and suggests a high probability of continued recovery. LOW could extend gains and potentially retest record highs in early 2026.

Thank you for subscribing to Earnings360, a morning newsletter that summarizes quarterly earnings for public companies that trade on U.S. markets.

This email communication is a sponsored email provided by Altimetry, a third-party advertiser of Earnings360 and MarketBeat.

This ad is sent on behalf of Altimetry, 110 Cambridge Street, Cambridge, MA 02141. If you would like to optout from receiving offers from Altimetry please click here.

If you have questions or concerns about your newsletter, please contact our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from Earnings360, you can unsubscribe.

Copyright 2006-2025 MarketBeat Media, LLC. All rights reserved. 345 N Reid Pl., Sixth Floor, Sioux Falls, South Dakota 57103. U.S.A..

Have you read “Behind the Scene”? It has some great stories about kitties and other animals saved by our refuge! Check it out by clicking on the link above.

Plan on visiting the Refuge? Please consider making a donation of one or some of the items on the list of daily-needed items:

To view Refuge Amazon Wish List use this link:

Sign up for an account at Chewy.com using this link and The Goathouse Refuge will receive a donation in your name!

Campus is quiet today. The hallways are empty, the classrooms still, and the front lawn rests beneath the lights that were switched on last night. This momentary calm before Thanksgiving offers a welcome pause and echoes the spirit of Advent, the season that begins not with noise, but with quiet anticipation.

Just hours ago, campus was filled with music, color, and energy as our community gathered for our annual tree lighting followed by the Fine Arts Extravaganza. The imagination and creativity our students shared stirred a spirit of gratitude fitting for Thanksgiving, while the glow of the lights pointed us toward the hope that shapes Advent and invites us to ponder the mystery of God made visible in the Incarnation. These moments remind us that our students are growing in ways that are sometimes celebrated in the spotlight and other times revealed gently and without fanfare.

In the spirit of the season, we are sharing our annual Advent booklet written by members of our faculty and staff. Each personal reflection is paired with sacred art from around campus. Together, they invite us to look more closely and notice how grace is present in the ordinary rhythm of our daily lives.

I hope these reflections offer a moment of peace in the weeks ahead and help guide our movement from Thanksgiving’s warmth to Advent’s expectant light.

Costco Members: This New Policy is a Game Changer—and it’s about much more than just bulk purchases! You already know the thrill of saving money thanks to your membership. That moment you walk past the register, knowing you got a massive discount, is unbeatable—almost as good as biting into that famous $1.50 hot dog. But what if we told you there are even more genius ways to stretch your dollars that you might be missing?

Saving money shouldn’t be a random occurrence; it should be a strategy. Your Costco card proves you’re already smart about where you spend, so take the next step and capitalize on this new information. We’ve compiled a quick list of essential money hacks that go far beyond the aisles of the warehouse.

Click here to check out our list and start discovering simple, smart ways to keep more cash in your wallet every month. Stop missing out on easy savings and start treating yourself to the financial freedom you deserve!

This email is never sent unsolicited. You have received this Newsmax email because you subscribed to it or someone forwarded it to you. To opt out, see the links below.

Remove your email address from our list or modifyyour profile. We respect your right to privacy. Viewour policy.

This email was sent by: Newsmax.com 362 N. Haverhill Road West Palm Beach, FL 33415 USA

Father, as I sit to write tonight, my heart feels tender in a way I can’t fully explain. I’ve been lingering on Acts 12:5 all day: “So Peter was being kept in the prison, but the congregation was intensely praying to God for him.” There’s something so beautiful about the way the early believers united—not in panic, not in despair, but in prayer. Intense, expectant, hopeful prayer. It makes me examine the focus of my own prayer life, and honestly, Lord, I feel a gentle conviction rising in me. I see how easily I slip into bringing You my concerns first, my needs, my anxieties, my dreams. And yes, You say to cast all my cares on You (1 Peter 5:7), but I also hear You asking me to widen my gaze.

Today You asked me, “Do you pray more for yourself than for others?” And my heart whispered, “Yes… sometimes.”Not always, but more often than I want to admit. There are days I rush to pray about my job, my relationships, my future, my uncertainties—sometimes without pausing to lift up the people around me who may be carrying far heavier burdens. And then I think about Peter in that prison, and how the church didn’t stop to think about themselves—they united for him. They prayed him into freedom. They prayed with passion because they believed prayer mattered. They believed prayer moved Heaven. I want to pray like that—for others—consistently and with deep compassion.

Lord, I’m realizing that praying for others requires a softness of heart that only Your Spirit can produce. It means noticing people. It means slowing down long enough to actually see their need. It means letting my heart be moved by the pain, hopes, and longings of those around me. When Paul wrote, “Carry each other’s burdens, and in this way you will fulfill the law of Christ”(Galatians 6:2), he wasn’t offering a polite suggestion—he was laying out part of the structure of Christian community. True love isn’t passive. True love kneels. True love intercedes. True love remembers the suffering of others even when our own lives feel heavy. Lord, shape my heart into one that loves like that.

I’ve also been thinking about all the different people Scripture tells us to pray for. “I urge, then, first of all, that petitions, prayers, intercession, and thanksgiving be made for all people— for kings and all those in authority…” (1 Timothy 2:1–2). Sometimes praying for leaders feels distant, or impersonal, or honestly… a little pointless. But Your Word says it matters. Praying for the unsaved matters. Praying for ministers of the gospel matters. Praying for the persecuted church—who right now may be sitting in prisons, like Peter once did—matters deeply. You move through intercession. You knit hearts together through intercession. You break spiritual chains through intercession. And You grow us spiritually through intercession because it pulls us out of the center of our own universe and places You there instead.

Lord, one of my greatest weaknesses is that sometimes my prayers become lists rather than conversations. I never want my relationship with You to be mechanical. I never want to treat You like a dispenser of blessings. I want to love You more than what You can give me. I want my prayers to reflect trust, surrender, and compassion—not spiritual consumerism. When I pray only for myself, my world becomes small. But when I pray for others, my world expands, because I begin to see people the way You do. Their names take on weight. Their struggles become personal. Their victories feel like my own. In praying for them, I step into their stories, and in doing that, I step closer to You, because You are always near the brokenhearted.

I think of Jesus praying for others—how He prayed for His disciples, how He prayed for all believers that would come after them (John 17), how He prayed for forgiveness for the ones crucifying Him. If the Son of God Himself prayed so earnestly for others, shouldn’t I follow that example? It humbles me, Lord. It reshapes my view of prayer entirely. Prayer isn’t just about my life being changed; it’s about Your kingdom being revealed in the lives of others. It’s about standing in the gap for someone else when they are too weary to stand on their own. It’s about being willing to be inconvenienced in my heart for the sake of loving someone the way You ask me to.

Screenshot

Today, You placed specific people on my heart. A friend who is struggling silently. A family member who is drifting spiritually. A coworker who seems happy but carries deep insecurity. A young woman at church who is growing in faith but feels spiritually attacked. These people matter to You more than I can comprehend. Lord, let me be faithful to lift them up. Let me pray for them the way the early church prayed for Peter—with intensity, with unity in Spirit, with unwavering trust that You hear. Let my prayers be fueled not by duty but by genuine love.

Father, I don’t want to be someone whose prayers revolve around my own world. I want to grow into someone who instinctively lifts others up, who intercedes with joy, who sees intercession as partnership with You rather than a task on a spiritual checklist. I want to be someone who looks at the brokenness of the world and responds—not with complaint or hopelessness—but with prayer. Because prayer acknowledges that You are still working. Prayer acknowledges that nothing is impossible with You. Prayer acknowledges that You care for every need—no matter how big or small.

And now, Lord, I want to pray:

Heavenly Father, soften my heart and widen my perspective. Teach me to pray for others with sincerity and perseverance. Help me see the people around me—really see them—and lift them before Your throne. Let my prayers be shaped by Your will, guided by Your Word, and filled with compassion. Deliver me from self-centeredness in prayer. Make me an intercessor, not for my glory, but so that Your love may flow through me. Help me to obey the command to pray for all people, for leaders, for the lost, for the church, and for those who suffer for Your name. Give me a heart that kneels before it speaks, a heart that carries others’ burdens with tenderness. Lord, help me to grow spiritually through praying for others, and in all things, make me more like Jesus. Amen.

As I close this entry, my heart feels lighter, but also more aware. I see now that one of the surest ways to grow spiritually is to make prayer less about me and more about others. When I shift my focus outward—when I intercede, when I cry out for someone else’s freedom, healing, salvation, or comfort—something in me transforms. I become less self-absorbed. I become more compassionate. I become more aligned with Your heart. And Lord, that is what I long for more than anything—to have a heart that reflects Yours.

Help me, Jesus, to live this out—not just tonight, but day after day. Help me to love others deeply, pray for them boldly, and trust You completely. Amen.CommentLikeYou can also reply to this email to leave a comment.

The numbers say everything’s fine… but it doesn’t feel fine, does it?

The cost of living keeps rising. The divide keeps widening. The anger keeps building.

Listen, I’ve spent three decades studying financial systems, and I’ve never seen pressure like this. It’s as if the old order of the economy has cracked and something new is forcing its way through.

Most people can’t see it yet. But they sense it. They feel it in their gut.

I’ve pulled on that thread for the past year, and what I’ve uncovered is bigger than anything I’ve ever reported. And it’s happening much faster than anyone imagines.

Written by Jeffrey Neal Johnson. Published 11/12/2025.

Key Points

Growing geopolitical competition is solidifying long-term government support for a secure domestic supply chain.

America’s leading rare earth companies are successfully turning strategic blueprints into tangible operational milestones.

Recent market volatility driven by temporary headlines may present a compelling entry point for long-term investors.

Recent headlines celebrating a U.S.-China trade truce have lulled the market into a false sense of security and triggered a sharp sell-off in domestic rare earth stocks. Behind those headlines, however, a more strategic and confrontational reality is emerging.

Beijing is now crafting a validated end-user (VEU) system — a surgical tool designed to maintain the flow of rare earths to approved, purely civilian American companies while explicitly blocking access for the U.S. military and its extensive network of contractors.

Most traders don’t realize there’s a window of time each day when price movements become highly predictable — and I’ve built a strategy designed to capitalize on it. One user reportedly earned thousands in his first few months using this approach, though results always vary. The key is timing and consistency, not luck or leverage.Discover how to target daily trading windows for potential profit

This isn’t de-escalation; it’s a declaration of a new, more targeted front in the global tech and defenserace. The shift makes the development of domestic producers such as MP Materials (NYSE: MP) and USA Rare Earth (NASDAQ: USAR) not just strategically important but mission-critical.

China Sharpens Its Weapon, Russia Joins the Fray

Pressure to build a secure U.S. supply chain is now coming from two global rivals, reshaping the strategic landscape and strengthening the long-term investment case for domestic producers.

First, China has sharpened its export-control tools. The VEU plan is a sophisticated escalation that weaponizes its supply-chain dominance by creating a potential red list for defense-related firms. That uncertainty affects any U.S. company with dual-use applications in sectors like aerospace and automotive.

The targeted approach is intended to inflict maximum pain on America’s national-security apparatus while minimizing collateral damage to broader commercial ties, making it a more sustainable — and more dangerous — long-term policy.

Second, while China refines its export tools, Russia is moving to build its own. President Vladimir Putin’s recent directive to create a national strategy roadmap for rare earth extraction signals a long-term strategic pivot. That raises the prospect of a coordinated China–Russia bloc in critical minerals, which would further consolidate supply away from the West.

These developments elevate the U.S. domestic supply-chain initiative from an important industrial policy to an urgent national-security mission. The investment case is no longer a speculative hedge on trade tensions; it is a fundamental bet on a government-mandated build-out of a defense-oriented supply chain.

De-Risked and Ready to Deliver

China’s VEU plan makes recent multi-billion-dollar U.S. investments in the domestic rare earth sector look not just strategic, but prescient. Washington is building a resilient ecosystem designed to withstand this exact threat, with MP Materials and USA Rare Earth as cornerstones.

MP Materials: America’s designated prime contractor. China’s strategy to cut off the U.S. military directly elevates MP’s importance. Its contracts with the Department of Defense are now more critical than ever. The 10-year price floor, which began on Oct. 1, provides revenue stability for the very products China seeks to restrict. MP Materials’ recent third-quarter 2025 earnings reportshowed record production of 721 metric tons of high-value NdPr (neodymium-praseodymium), demonstrating its ability to meet secure demand. With a cash balance of $1.94 billion, it has the financial firepower to accelerate build-out to meet defense-related demand surges.

USA Rare Earth: The strategic second source. In a world of targeted supply-chain attacks, redundancy is key. USAR’s acquisition of UK-based Less Common Metals (LCM)brings immediate non-Chinese expertise in specialized metals and alloys needed for defense-grade magnets. Combined with a post-Q3 cash position of over $400 million, USAR is well positioned to become America’s critical second source and increase its chances of securing lucrative DoD contracts as it approaches Q1 2026 commissioning.

The Market’s Miscalculation: A Powder Keg of Opportunity

The market sold off on a simplistic truce headline, creating a stark valuation disconnect. Analyst consensus remains a Moderate Buy on both companies, and the recent price drops have widened the gap to their average analyst targets.

Adding to the dynamics is high short interest against the sector — 17.89% for MP and 14.45% for USAR. That extreme pessimism creates a coiled-spring scenario: any sudden geopolitical escalation, such as a formal announcement of China’s VEU list or a new U.S. defense contract, could instantly invalidate the bearish thesis and force short sellers to buy back shares en masse.

That forced buying could trigger an explosive rebound. The race for rare earth supremacy is accelerating; for investors with a long-term horizon, today’s fear may have put a strategically vital sector on sale.

This email content is a paid sponsorship provided by Porter & Company, a third-party advertiser of MarketBeat. Why did I get this message?.

If you have questions about your newsletter, please contact our South Dakota based support team at contact@marketbeat.com.

While many stocks have come under considerable pressure over the past month, entertainment giantWarner Bros. Discovery (NASDAQ: WBD)continues trudging higher. As of the Nov. 24 close, shares are up approximately 8% during the past 30 days.

Warner Bros’ gains have persisted as rumors around a potential acquisition of the firm heat up. Below, we’ll dive into the latest news around this stock and detail what it means going forward.

Warner Bros. Eyes Year-End Deal, PSKY, NFLX, and CMCSA Submit Bids

The last time MarketBeat covered Warner Bros, the firm had just put up its proverbial “for sale” sign. WBD said on Oct. 21 that the company had received multiple unsolicited offers for some or all of the firm. It initiated a review of these offers to “maximize shareholder value.”

All three firms have sent in their first round of non-binding bids. Paramount Skydance is reportedly looking to acquire the entire firm, including WBD’s linear television networks like CNN and TNT Sports.

Meanwhile, Netflix and Comcast are only interested in the company’s film production and streaming assets. Film production includes DC Studios, which holds valuable intellectual property, such as Superman and Batman. Streaming is primarily centered around HBO Max, which is one of the world’s top five players in video streaming with 128 million subscribers as of last quarter.

Paramount’s Bid Offers the Clearest Path Forward

Among the offers, Paramount’s bid appears to be the most comprehensive and straightforward. Reports emerged that Paramount was planning to offer $71 billion for the firm through a group investment with the sovereign wealth funds of Saudi Arabia, Qatar, and Abu Dhabi.

This price would represent an approximately 25% premium over the stock’s Nov. 24 market capitalization of just under $57 billion and a share price between $28 and $29. However, this report appears to be inaccurate, as Paramount denies these claims.

According to Bloomberg Intelligenceanalyst Geetha Ranganathan, Paramount’s offer is likely between $25 and $27 per share. An offer price in this range would represent an approximate 9% to 18% premium over WBD’s Nov. 24 closing price. This would still be a solid win for shareholders, who would receive the offer price upon acceptance of a deal. Importantly, Ranganathan also indicated that the sale process could extend beyond WBD’s year-end timeline.

Potential Deal Denial Creates Risks

If no buyer meets WBD’s price expectations, the company could opt to split its business into two separate entities: one for film and streaming, and another for its linear TV assets.

This scenario is likely the biggest near-term risk for WBD shares. The current stock price likely already has a significant takeover premium baked in. If no takeover materializes, then the premium could dissipate quickly.

When Warner Bros. first announced that the company would split in June, shares were trading at around $10. Today, they sit around $23. In the event of a split, it’s difficult to predict how shares could behave, but it would not be surprising to see a significant drop. However, it is also possible that this path could create the most value long-term for WBD, making up for any short-term impacts.

WBD Shares and Price Targets on the Rise

The market continues to bid up WBD stock, indicating that hopes of a sale are rising. Wall Street analysts also continue to push up their price targets.

The consensus target on WBD sits just below $22, implying around 4% downside in shares.

However, among targets issued after Oct. 22, the average is just above $25, implying 9% upside to align with statements made by Ranganathan.

It’s difficult to say what will happen next for WBD. Markets could react differently depending on which firm strikes a deal with WBD—or if no deal is reached at all.

Investors should consider this risk and should also evaluate the relative merits of the stock if WBD is not acquired. READ THIS STORY ONLINE

For years, the autonomous vehicle (AV) sector has been defined by a frustrating narrative of high cash burn and distant promises. Investors have watched billions of dollars vanish into research and development (R&D) with very little revenue to show for it. Now as November ends, that narrative is beginning to shift.

WeRide (NASDAQ: WRD) shares jumped 14.7% to $8.26 after its third-quarter earnings release. Despite geopolitical headwinds and a 73.8% year-to-date (YTD) decline, WeRide finally gave investors something concrete: real revenue growth and improving margins.

How WeRide Turned the Corner

WeRide reported a 761% year-over-year (YOY) jump in robotaxi revenue, which marks a potential inflection point for the industry. For the first time, the firm is offering evidence that it has moved from R&D mode to commercial viability, and Wall Street has taken notice.

Total revenue for the quarter hit RMB 171 million (approx. $24 million USD), representing a 144.3% increase compared to the same period last year. This growth was driven by two distinct engines:

Product Revenue: This segment, which includes the sale of Robobuses and autonomous sweepers, grew 428% to $11.1 million.

Service Revenue: This segment, primarily robotaxi fares and data services, grew 66.9% to $12.9 million.

Perhaps the most critical data point for long-term investors is gross margin. In the third quarter of 2024, WeRide’s gross margin was a thin 6.5%, typical for a hardware-heavy manufacturing phase. In this latest report, that figure expanded to 32.9%.

A rising gross margin indicates that a company is scaling efficiently. It signals a shift away from expensive hardware testing toward high-margin software and service operations. This is the holy grail for tech sector investors, as it suggests the business can grow without costs spiraling out of control.

While WeRide is not yet profitable, it is moving in the right direction. The net loss for the quarter narrowed by 71% to $43.2 million. Adjusted for non-cash items, the loss was $38.7 million. This reduction is significant because it shows that revenue growth is outpacing operating expense growth.

A Blueprint for Profit: The Abu Dhabi Model

WeRide’s revenue jump is not an accident—it is the direct result of a strategic pivot. While the United States has effectively closed its doors to Chinese autonomous technology, WeRide has found a lucrative market in the Middle East.

In October 2025, WeRide secured the world’s first city-level fully driverless robotaxi permit outside the U.S. in Abu Dhabi, a transformative agreement. The permit allows the company to remove the safety driver from the front seat, the biggest expense in the robotaxi business model.

Partnering with Uber (NYSE: UBER), WeRide sells the vehicles and provides the autonomous tech, while Uber handles customer acquisition. This structure delivers upfront product revenue and ongoing service revenue—without the need for a consumer-facing fleet.

CEO Tony Han revealed that a robotaxi breaks even at roughly 12 trips per day. The company’s current utilization target is 25 trips per day with 24/7 service, which would make each vehicle a standalone profit generator.

Cash Is King: A Billion Dollar War Chest

Autonomous driving is a capital-intensive business. Critics often cite high cash burn rates as a reason to steer clear of this part of the transportation sector. However, WeRide’s latest report offers a strong rebuttal to liquidity concerns.

As of Sept. 30, 2025, WeRide held approximately $764.1 million in cash, cash equivalents, and wealth management products.

This figure excludes the roughly $308 million raised during the company’s recent dual listing on the Hong Kong Stock Exchange in November.

When combining these figures, WeRide effectively has over $1 billion in accessible liquidity—a massive competitive advantage. The case provides a multi-year runway to continue R&D (which currently accounts for 73% of operating expenses) without the immediate need to dilute shares further.

Because of these facotors, WeRide is financially positioned to weather economic downturns while competitors may struggle to raise funds.

The Geopolitical Pivot: Risk vs. Reward

Investors must acknowledge the elephant in the room: The U.S. Commerce Department has issued a final rule banning Chinese connected vehicle software starting in 2027. This effectively locks WeRide out of the American market.

However, the market reaction to the Q3 earnings suggests this risk is already priced in. By succeeding in the UAE and securing new permits in Singapore and Switzerland, the company has proven that the Total Addressable Market (TAM) outside of the United States is large enough to support a viable business.

WeRide now holds autonomous driving permits in eight countries, including Belgium, France, and Singapore. The company has accumulated over 55 million kilometers of Level 4 (L4) autonomous mileage, a data advantage that is difficult for new entrants to replicate. The company’s success in the Middle East validates the thesis that autonomous driving is a global revolution, not just an American one.

Beyond the Taxi: The Dual Flywheel Effect

While the robotaxi segment is grabbing headlines, WeRide is not a one-hit wonder. The company operates a dual-flywheel strategy that leverages its technology to generate immediate cash flow while the robotaxi network scales. The company’s WePilot 3.0 system achieved Start of Production (SOP) in November 2025.

WePilot 3.0 is an Advanced Driver Assistance System (ADAS) sold directly to automakers for mass-market passenger cars. WeRide is currently rolling this out with partners and has been nominated by the GAC Group for future models.

Selling software to carmakers generates immediate revenue and provides vast amounts of driving data, which in turn helps refine the algorithms used in the robotaxis.

Despite the 14.7% rally, WeRide shares are still trading down approximately 74% YTD. This steep decline attracted significant short interest, which rose nearly 35% in October. The strong earnings report likely triggered a bit of a short squeeze, forcing bears to buy back stock to cover their losses.

For new investors, the Abu Dhabi Model offers tangible proof of concept. If WeRide can replicate this unit-economic success in Singapore and Dubai, the current valuation (trading significantly below its IPO levels) could represent a deep-value opportunity in the artificial intelligence sector. READ THIS STORY ONLINE

Years before it became a household name, Shopify showed an early momentum pattern that experienced traders used to catch a 120% move — and that same repeatable signal has just appeared on a new small-cap ticker that hasn’t hit the mainstream yet. Our free Momentum Trading Report breaks down how to spot these stealth setups and reveals which names are flashing right now.GET EARLY ACCESS TO THE FREE MOMENTUM TRADING REPORT HERE

Risks remain, but the S&P 500’s (NYSEARCA: SPY) uptrend is intact. The November correction was more of a broad-market consolidation, setting the market up for another leg of the rally, likely to unfold in December. This is an examination of three major themes driving S&P 500 price action and why it’s set up to advance to new highs before year-end.

Macro-Economic Headwinds Ease

Macroeconomic uncertainty has been causing significant concern among investors throughout the year. Uncertainty is linked to trade relations, tariff impacts, and, more recently, the government shutdown. The story for December is that the government shutdown is over, trade relations aren’t deteriorating, and there has been some relief regarding tariffs.

Primarily, the impact of tariffs on Q3 results was far less than expected. The average S&P 500 company outperformed its consensus estimate by more than 600 basis points, which is well above average, and the Q4 season is likely to follow a similar trend.

While the Q3 results outperformed, and most companies improved their guidance, the Q4 consensus forecast remained unchanged. The likely outcome is that Q4 results will outperform by a similarly large margin.

Meanwhile, the FOMC remains on track to cut rates in 2026. The outlook for cuts has dimmed, but there is still an expectation of another two to three 25-basis-point cuts by next summer. The odds for a cut in December are also significantly high and may increase as the month progresses.

With the government shutdown over, government-collected data is being released, and it aligns with healthy, albeit cooler, economic conditions compared to the previous year.

Retail Earnings Were Good, Guidance Was Increased

There were some areas of weakness in the retail sector’s earnings data, but the overall trend was bullish. Most retailers grew revenue and earnings, produced solid margins, and provided favorable guidance. The takeaway is that Black Friday and Cyber Monday sales events mark the beginning of the holiday shopping season and are likely to exceed forecasts.

As it stands, holiday spending is expected to increase by 3% to 3.5% with strength centered in eCommerce. Deals and value will be a driver, positioning off-price retailers and Walmart as winners. Among the critical factors for investors is that retail leaders like Walmart (NYSE: WMT) and The TJX Companies (NYSE: TJX) have solid cash flow, pay attractive dividends, and repurchase shares, sometimes aggressively.

The next visible catalyst is the Q4 reporting cycle in January. Still, analysts could drive this sector higher before then with revenue, earnings, and stock price target revisions linked to Q3 results and early holiday spending data.

The AI Trade Is Reignited

Fears of an AI bubble bursting were laid to rest by NVIDIA’s (NASDAQ: NVDA)Q3 results, which showed stronger-than-expected growth, and by subsequent news that Amazon (NASDAQ: AMZN) plans to invest up to $50 billion in AI infrastructure for U.S. government contracts. Together, these developments reinforce the durability of AI demand across both commercial and public sectors.

The NVIDIA release confirms that its AI business is larger than initially thought, growing faster than anticipated, and accelerating in the second half of the year. This has it set up to outperform in the current and following quarters and to sustain strength long into the future.

The S&P 500 remains on course to hit the 7,300 mark soon. The move may not occur before the year’s end, but the rebound is likely to start by then, and new highs will quickly follow. Notable technical indicators include the stochastic oscillator, which has retreated to the middle of its range, indicating a market that has rebalanced itself and has ample room to move higher. READ THIS STORY ONLINE

Central banks and major institutions have been increasing their gold holdings at one of the fastest paces in decades — and Dr. David Eifrig believes this trend reflects deeper shifts in the financial system that most everyday investors aren’t seeing. After four decades in the markets, including time on a trading desk during 1987’s Black Monday, he says this surge isn’t just a reaction to price movements but part of a broader realignment that could influence savings, investments, and even borrowing costs.

Eifrig recently released a new briefing explaining what’s driving this global accumulation, what it may mean for individual investors, and the practical steps he recommends considering now. During Stansberry’s Black Friday event, his latest research is also available at the lowest access price of the year.CLICK HERE TO GET THE FULL BRIEFING AND BLACK FRIDAY ACCESS

The Night Owl is a financial newsletter that provides in-depth market analysis on stocks of interest to individual investors. Published by MarketBeat and Early Bird Publishing, The Night Owl is delivered around 9:00 PM Eastern Sunday through Thursday. If you give a hoot about the market, The Night Owl is the newsletter for you.