*Sponsored

(Nasdaq: CVKD) Jumps Green Out Of Today’s Bell (Huge Acquisition News Circulates)

*Click Here To Get Our Alerts Faster Via SMS*

December 12th

Dear Reader,

Cadrenal Therapeutics, Inc. (Nasdaq: CVKD) is making early green moves this Friday while holding the top spot on my watchlist.

Could it be because of this week’s game-changing acquisition announcement?

If you haven’t yet, check it out:

Cadrenal Therapeutics Acquires VLX-1005, a First-in-Class Phase 2 12-LOX Inhibitor for Patients with Heparin-Induced Thrombocytopenia (HIT)

From the article:

“With the acquisition of VLX-1005, Cadrenal continues to advance novel therapeutics to treat or prevent thrombosis in high-risk patients,” said Quang X. Pham, Chairman and CEO of Cadrenal Therapeutics. “HIT remains a dangerous condition without a therapy that addresses its immune-driven biology. The emerging data from VLX-1005 suggest meaningful potential to improve patient outcomes while maintaining favorable tolerability. We believe this is a compelling strategic addition to our pipeline, with the market size for HIT reaching $1Bn in the US and EU.”

Don’t forget. CVKD has a very low float.

With approx. 1.54Mn shares in its float, it’s critical to watch for heightened volatility potential.

Take a moment to review my initial (Nasdaq: CVKD) report below and consider this profile for your radar.

—–

A specialized cardiovascular drug developer has just announced an agreement to acquire a late-stage, first-in-class asset targeting a key enzyme pathway implicated in serious clotting complications linked to common hospital therapies.

This 12-lipoxygenase program, including the VLX-1005 candidate and related assets, is intended to complement the company’s existing focus on high-need anticoagulation settings, where current options often leave patients at meaningful risk.

With the deal structured around future clinical and regulatory milestones, leadership appears intent on carefully deploying capital while advancing a differentiated approach to complex, immune-driven thrombotic disease.

Now, mix in a low float of fewer than 2Mn shares and a pair of analyst targets suggesting SIGNIFICANT upside potential, and there’s no doubt why this Nasdaq profile just rocketed up my watchlist.

Drop what you’re doing and consider this under-the-radar idea for your radar:

*Cadrenal Therapeutics, Inc. (Nasdaq: CVKD)*

Cadrenal Therapeutics, Inc. is a biopharmaceutical company developing therapeutics for patients with cardiovascular disease.

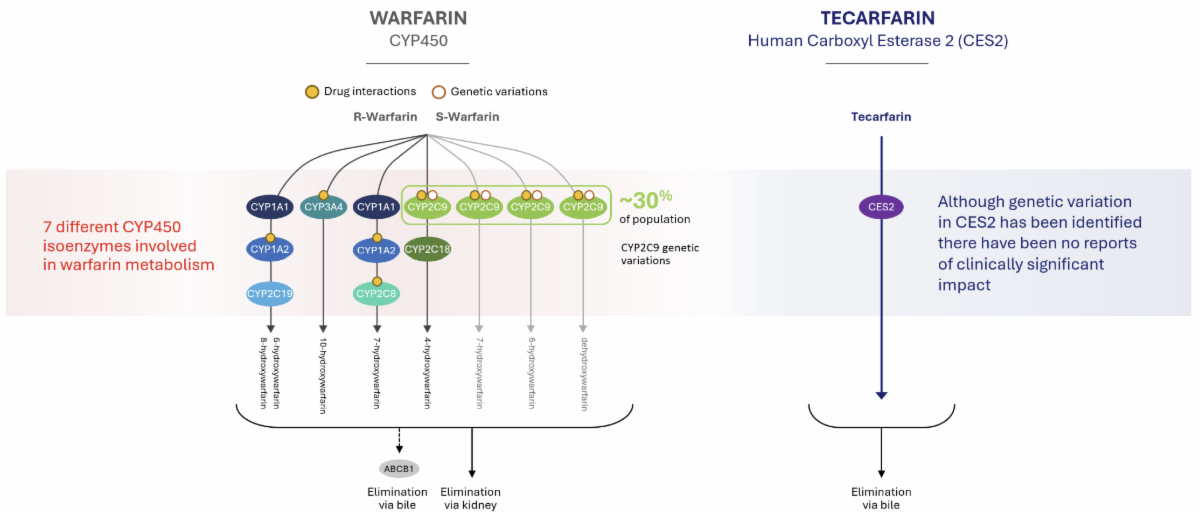

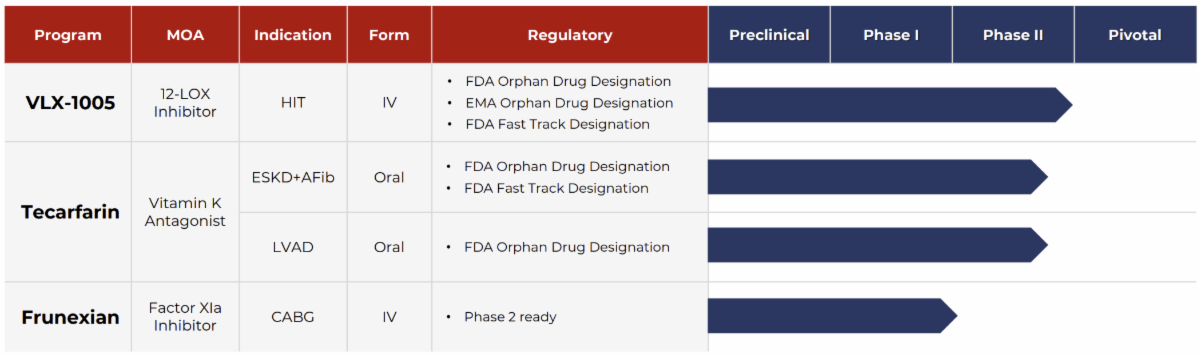

Cadrenal’s lead investigational product is tecarfarin, a novel oral vitamin K antagonist anticoagulant that addresses unmet needs in anticoagulation therapy.

Tecarfarin is a reversible anticoagulant (blood thinner) designed to prevent heart attacks, strokes, and deaths due to blood clots in patients requiring chronic anticoagulation.

And based on several potential breakout catalysts, (Nasdaq: CVKD) has found its way to the top of my watchlist. Check them out:

#1. A Mind-Blowing December Acquisition Positions CVKD For Disruption Of A $40Bn Global Anticoagulation Market.

#2. A Low Float Could Create An Environment Of Heightened Volatility Potential.

#3. A $45 Analyst Target Suggests Triple-Digit Potential Upside From Current Levels.

#4. Another Analyst Reiterates A $30 Target For CVKD.

#5. A Major Acquisition Has Game-Changing Potential For Cadrenal’s Pipeline.

But more on those in a second…

Company Breakdown: Cadrenal Therapeutics, Inc. (Nasdaq: CVKD)

Cadrenal Therapeutics is a late-stage biopharmaceutical company developing tecarfarin, an investigational anticoagulant designed as a superior and safer Vitamin K antagonist (VKA) for patients with implanted cardiac devices or rare cardiovascular conditions.

The company strives to improve patient outcomes and reduce major adverse events among these populations, who currently lack any approved chronic anticoagulation options besides warfarin—a medication known for its serious side effects and complex management requirements.

Through its innovative approach, Cadrenal aims to alleviate some of the most significant challenges faced by patients and healthcare providers who rely on warfarin.

Cadrenal’s Phase 3-ready drug candidate, tecarfarin, represents a novel VKA anticoagulant supported by extensive data suggesting its potential to be superior to warfarin, with the possibility of fewer adverse events such as strokes, heart attacks, bleeding, and death.

Tecarfarin has received orphan drug designation for heart failure patients with left ventricular assist devices (LVADs), as well as both orphan drug and fast track status for end-stage kidney disease (ESKD) patients with atrial fibrillation (Afib).

The company is actively pursuing pivotal clinical trials and exploring clinical and commercial partnership opp’s.

Cadrenal also plans to investigate tecarfarin in patients with mechanical heart valves who experience anticoagulation difficulties due to genetic warfarin resistance, polypharmacy, or kidney impairment.

Tecarfarin is metabolized through a different pathway than warfarin, and data indicate that its efficacy remains unaffected by common drug-drug interactions or kidney impairment—challenges that are prevalent among these patient populations.

Phase 2/3 clinical trials have demonstrated that tecarfarin may offer greater stability and increased time in therapeutic range, which is inversely correlated with major adverse events.

As the only new VKA blood thinner in development specifically for warfarin-dependent patients with implanted cardiac devices or rare cardiovascular conditions, Cadrenal is boldly challenging the status quo, seeking to innovate a new anticoagulant that delivers better care to underserved patients.

Tecarfarin’s Metabolic Advantage

Tecarfarin is metabolized via an alternate pathway that is abundant and essentially insaturable, thereby avoiding the bottleneck in the CYP450 pathway where warfarin is metabolized.

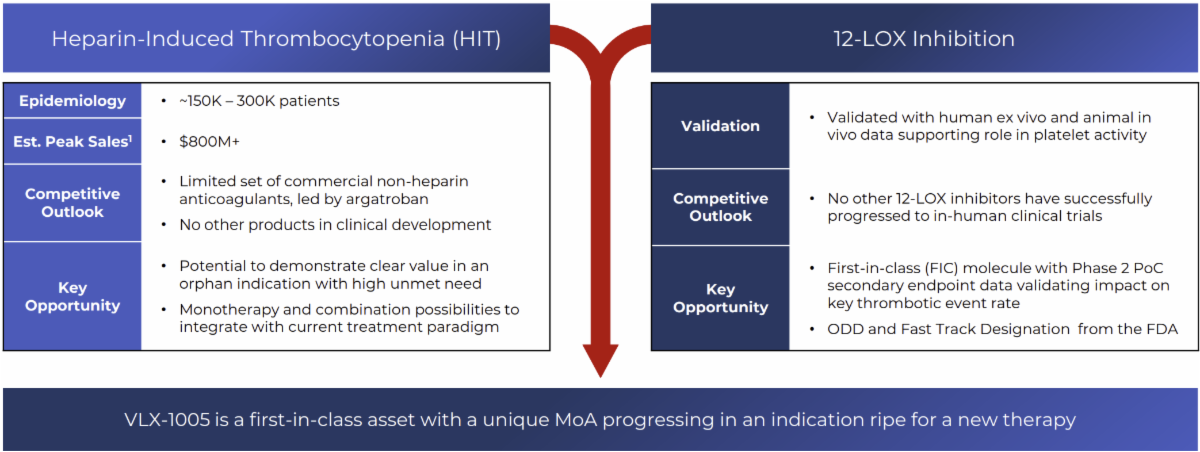

VLX-1005 Expands Company’s Portfolio With A Novel Immune-Targeted Approach – 12-LOX Inhibition

Recent Acquisition – VLX-1005

- A parenteral (intravenous) 12-Lipoxygenase (12-LOX) inhibitor designed to block key pathways in immune-mediated platelet activation

- Blocks platelet activation and inhibits thrombus formation

- Orphan Drug Designation (ODD) for patients with heparin induced thrombocytopenia (HIT)

- Acquired December 2025

VLX-1005: The only clinical stage 12-LOX inhibitor

VLX-1005 is uniquely positioned to address an underserved indication with a unique mechanism of action (MoA) and expected meaningful impact on thrombotic events beyond that achievable with current anticoagulant therapy.

Clinical Development Pipeline

Grab Sources Here: CVKD Website. CVKD Presentation.

—–

And as I mentioned earlier, (Nasdaq: CVKD) has several potential catalysts to consider immediately. Check them out:

#1. CVKD Potential Catalyst – A Mind-Blowing December Acquisition Positions CVKD For Disruption Of A $40Bn Global Anticoagulation Market.

Cadrenal Therapeutics Acquires VLX-1005, a First-in-Class Phase 2 12-LOX Inhibitor for Patients with Heparin-Induced Thrombocytopenia (HIT)

- Novel first-in-class therapeutic targeting a key immune signaling pathway and the underlying cause of HIT

- It is the first and only potent, highly selective inhibitor of human 12-LOX in clinical testing, distinguishing it from related compounds.

- Orphan Drug and Fast Track designations from the FDA

PONTE VEDRA, Fla., Dec. 11, 2025 (GLOBE NEWSWIRE) — Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a biopharmaceutical company developing transformative therapeutics to overcome the limitations of current anticoagulation therapy, today announced the acquisition of VLX-1005 and related 12-lipoxygenase (12-LOX) assets from Veralox Therapeutics (“Veralox”). The acquisition immediately strengthens Cadrenal’s pipeline with a late-stage, first-in-class drug candidate targeting a critical immune signaling pathway. This acquisition addresses yet another underserved therapeutic opp. in the $40Bn global anticoagulation market.

VLX-1005 is a novel, potent, selective small-molecule inhibitor of 12-LOX, a key pathway driving immune platelet-mediated inflammation and a contributor to the pathogenesis of HIT. This potentially life-threatening complication can occur in up to 5% of patients exposed to heparin – the most commonly used parenteral anticoagulant – regardless of dose, schedule, or route of administration. HIT antibodies can cause catastrophic and life-threatening arterial and venous thrombosis. Approximately 300,000 patients in the United States are evaluated each year for suspected HIT, and an estimated 56,000 confirmed diagnoses occur each year. Mortality and thromboembolic event (TE) rates remain high despite currently available therapies.

Two Phase 1 studies of VLX-1005 in healthy participants have demonstrated that VLX-1005 was well tolerated, with no deaths, no serious adverse events, and no trend in adverse event reporting with increasing doses. A recent Phase 2 study (VLX-1005-003) evaluated VLX-1005 in individuals with suspected HIT, and interim results demonstrated encouraging reductions in thromboembolic events. These events have become a preferred, clinically meaningful endpoint for regulators, clinicians, and payers, given the rising rates observed in current HIT populations.

VLX-1005 has received Orphan Drug Designation (ODD) and Fast Track designation from the U.S. Food and Drug Administration, as well as orphan drug status from the European Medicines Agency. Second-generation therapeutics targeting 12-LOX are also under development for type 1 diabetes and other immune-mediated and inflammatory diseases.

“We are pleased the advancement of VLX-1005 for the treatment of HIT will continue under the leadership of Cadrenal,” said Matthew Boxer, Co-Founder of Veralox Therapeutics. “The program has found a home in Cadrenal, where it aligns with a shared vision and excitement regarding the promise 12-LOX technology may offer patients.”

“With the acquisition of VLX-1005, Cadrenal continues to advance novel therapeutics to treat or prevent thrombosis in high-risk patients,” said Quang X. Pham, Chairman and CEO of Cadrenal Therapeutics. “HIT remains a dangerous condition without a therapy that addresses its immune-driven biology. The emerging data from VLX-1005 suggest meaningful potential to improve patient outcomes while maintaining favorable tolerability. We believe this is a compelling strategic addition to our pipeline, with the market size for HIT reaching $1Bn in the US and EU.”

…

Read the full article here.

—–

#2. CVKD Potential Catalyst – A Low Float Could Create An Environment Of Heightened Volatility Potential.

According to info from the Yahoo Finance website, CKVD has a very low float.

The website reports this profile to have roughly 1.54Mn shares in its float.

Why is that important? It’s important on one crucial level. Volatility potential.

If positive company news appears towards the end of 2025, could it provide a breakout spark when paired with this volatile potential?

—–

#3. CVKD Potential Catalyst – A $45 Analyst Target Suggests Triple-Digit Potential Upside From Current Levels.

Last month, Noble Capital Markets analyst, Robert LeBoyer, reiterated his $45 price target.

From Thursday’s 4:00PM EST closing valuation, that target provides CVKD with a potential upside of 300+%!

Details from the report:

Conclusion. Cadrenal continues to make progress in several tecarfarin indications and its newly acquired portfolio to meet the need for anticoagulants where current drugs are not effective or contraindicated due to safety. We are reiterating our Outperform rating and $45 price target.

—–

#4. CVKD Potential Catalyst – Another Analyst Reiterates A $30 Target For CVKD.

Another analyst, David Bautz of Zacks Small-Cap Research, reiterated their $30 target for CVKD in September.

From its 4:00PM EST close on Thursday, that targets suggests 150+% potential upside for CVKD.

Report highlights:

Cadrenal has now enhanced its pipeline with the acquisition of frunexian and the other Factor XIa inhibitors and we look forward to additional information regarding their development. The shift to focusing on ESKD patients for tecarfarin is important as there is a significant need for effective anticoagulant therapy for those patients and we believe positive results could also serve to de-risk the development of tecarfarin in other indications such as in LVAD patients. Before incorporating frunexian into our model we will wait and see what development path the company decides to pursue with it, thus our valuation remains at $30 per share.

—–

#5. CVKD Potential Catalyst – A Major Acquisition Has Game-Changing Potential For Cadrenal’s Pipeline.

Cadrenal Therapeutics Enhances Anticoagulation Pipeline Through Acquisition of eXIthera’s Portfolio of Factor XIa Inhibitors

Acquisition significantly enhances the Company’s pipeline by adding novel assets in acute and chronic anticoagulation settings

Company is strategically poised to deliver differentiated therapeutics across the spectrum of cardiovascular thrombotic risk

PONTE VEDRA, Fla., Sept. 15, 2025 (GLOBE NEWSWIRE) — Cadrenal Therapeutics, Inc. (Nasdaq: CVKD), a biopharmaceutical company developing transformative therapeutics to overcome the gaps in anticoagulation therapy, today announced the acquisition of the assets of eXIthera Pharmaceuticals (“eXIthera”), including its proprietary portfolio of investigational intravenous (IV) and oral Factor XIa inhibitors. The acquisition significantly enhances Cadrenal’s pipeline, adding drug candidates that address large and underserved segments of the current $38Bn global anticoagulation market.

eXIthera’s lead asset, frunexian, is a first-in-class, Phase 2-ready intravenous (IV) Factor XIa inhibitor designed for acute care settings where contact activation of coagulation by medical devices plays a significant role, such as cardiopulmonary bypass, catheter thrombosis, and other blood-contacting implanted cardiac devices. The acquisition also includes EP-7327, an oral Factor XIa inhibitor, for the prevention and treatment of major thrombotic conditions.

“With this acquisition, Cadrenal is the only company in the world developing a novel vitamin K antagonist (tecarfarin) and Factor XIa inhibitors, a promising new class of anticoagulants,” said Quang X. Pham, Chairman and CEO of Cadrenal Therapeutics. “These newly acquired assets will expand Cadrenal’s capabilities in an effort to address even more critical gaps in current antithrombotic treatment, especially for patients for whom current therapies are unreliable or carry excessive bleeding risk.”

…

“This acquisition reinforces Cadrenal’s long-term vision of becoming a category leader in anticoagulation,” added Pham. “With tecarfarin planning a trial in patients with end-stage kidney disease transitioning to dialysis, our plans for LVAD patients, and the current addition of frunexian and EP-7327, we believe that Cadrenal is strategically positioned to deliver differentiated therapeutics across the entire spectrum of patients with cardiovascular thrombotic risk.”

…

Read the full article here.

—–

(Nasdaq: CVKD) Recap – 5 Potential Breakout Catalysts Lead The Way

#1. A Mind-Blowing December Acquisition Positions CVKD For Disruption Of A $40Bn Global Anticoagulation Market.

#2. A Low Float Could Create An Environment Of Heightened Volatility Potential.

#3. A $45 Analyst Target Suggests Triple-Digit Potential Upside From Current Levels.

#4. Another Analyst Reiterates A $30 Target For CVKD.

#5. A Major Acquisition Has Game-Changing Potential For Cadrenal’s Pipeline.

—–

Coverage is now officially underway on Cadrenal Therapeutics, Inc. (Nasdaq: CVKD).

As soon as updates pop up, I’ll get them out to you quickly. Talk soon.

Sincerely,

FierceAnalyst | Jaks Swift

Editorial Writer

(Always Remember The St-ock Prices Could Be Significantly Lower Now From The Dates I Provided.)

*FierceInvestor (FierceInvestor . com) is owned by SWN Media LLC, a limited liability company. Data is provided from third-party sources and FierceInvestor (“FI”) is not responsible for its accuracy. Make sure to always do your own research and due diligence on any day and swing profile I bring to your attention. We do not provide personalized fin-ancial advice, are not finan-cial advisors, and our opinions are not suitable for all in-vest-ors.

Pursuant to an agreement between SWN Media LLC and TD Media LLC, SWN Media LLC has been hired for a period beginning on 12/11/2025 and ending on 12/12/2025 to publicly disseminate information about (CVKD:US) via digital communications. Under this agreement, SWN Media LLC has been paid seventeen thousand five hundred USD (“Funds”). To date, including under the previously described agreement, SWN Media LLC has been paid seventy two thousand five hundred USD (“Funds”). These Funds were part of the funds that TD Media LLC received from a third party who did not receive the Funds directly or indirectly from the Issuer and does not own st-ock in the Issuer but the reader should assume that the clients of the third party own shares in the Issuer, which they will liquidate at or near the time you receive this communication and has the potential to hurt share prices.

Neither SWN Media LLC, TD Media LLC and their member own shares of (CVKD:US).

Please see important disclosure information here: https://fierceinvestor.com/disclosure/cvkd-fl5jc/#details

Fierce | 4834 NW 2nd Ave Unit #388 | Boca Raton, FL 33431 US

Unsubscribe | Update Profile | Constant Contact Data Notice