A message from our partners at Huge Alerts

BSEM: From Profitable Regenerative Leader to Advanced Wound Care Powerhouse with a Nasdaq Uplisting on the Horizon.

BioStem Technologies (OTCQB: BSEM) continues to separate itself from the small-cap MedTech pack with seven straight profitable quarters, FDA-registered manufacturing, and clinically proven BioREtain® technology that drives superior healing outcomes in diabetic foot ulcers.

The recent acquisition of BioTissue’s surgical and wound care business adds $29 million in revenue, a national sales network, and immediate access to hospital and surgical settings, creating a direct path into acute and advanced wound care markets.

With early adoption reflected in 40% year-over-year unit growth, a robust $300–$350 million market opportunity, and a potential Nasdaq uplisting in mid-2026, BSEM is executing on every element of a high-growth MedTech strategy.

With a $25.50 price target from Zacks, BSEM stands out as a small-cap MedTech name with significant upside potential, especially as it prepares for a potential Nasdaq uplisting in 2026. Strong financial discipline, expanding commercial reach, and validated clinical results make BSEM a rare small-cap story to keep an eye on.

This Month’s Exclusive Story

T-Mobile: The Buyback King’s Safe Haven Strategy

Submitted by Jeffrey Neal Johnson. Published: 2/4/2026.

In Brief

- The company is aggressively returning capital to shareholders through a massive share repurchase program and a rapidly growing quarterly cash dividend.

- Management has successfully pivoted from heavy infrastructure spending to a harvest phase that generates significant free cash flow for strategic allocation.

- Upcoming strategic updates are expected to reveal ambitious financial targets that build on the company’s award-winning network and industry-leading loyalty.

Investors are navigating a market littered with landmines. Headlines are dominated by speculation about the Federal Reserve, Treasury yields that won’t settle, and gold prices swinging wildly. The growth-at-all-costs mentality that powered the tech sector for the last decade has evaporated. In 2026, capital is fleeing speculative assets and hunting for safety.

Finding a safe harbor that still delivers returns is difficult. Government bonds, once the go-to safe asset, have become volatile amid inflation concerns. That has opened an opportunity for a specific type of equity: cash-rich, shareholder-friendly companies. T-Mobile US (NASDAQ: TMUS) has evolved into that profile. No longer just a scrappy wireless carrier, it now functions as a capital-return engine built to weather volatility. With a beta of just 0.44 — far lower than the S&P 500 — T-Mobile offers investors a way to stay invested without losing sleep.

From Building to Harvesting: The Cash Strategy

The biggest scam in the history of gold markets is unwinding (Ad)

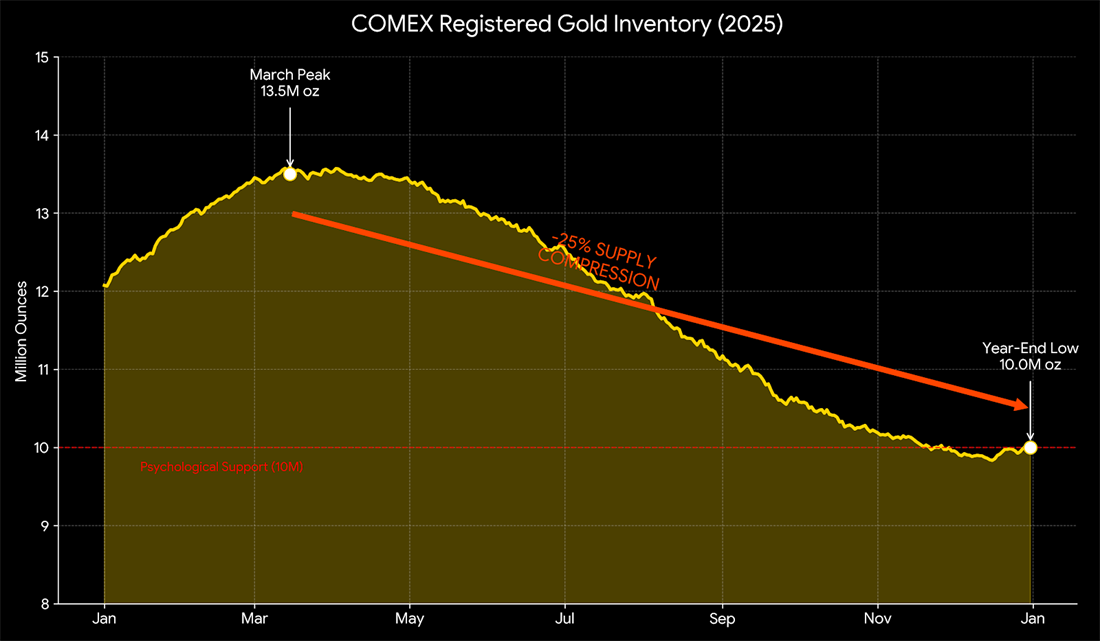

There are 90 paper gold claims for every real ounce in COMEX vaults. Ninety promises, one ounce of metal. It’s like musical chairs with 90 players and one chair. COMEX gold inventory dropped 25 percent last year alone as gold flows East to Shanghai, Mumbai, and Moscow. On March 31st, contract holders can demand delivery. When similar situations arose in the past, markets closed and rules changed. Paper holders got crushed while mining stock holders made fortunes. One stock sits at the center of this crisis.Get the full story on this opportunity now.

For the past decade, T-Mobile was in a heavy construction phase, spending billions buying spectrum and building towers to create a nationwide 5G network.

In financial terms, this is known as being capex‑heavy (capital expenditure–heavy). It requires large upfront cash outlays to secure future growth.

That era is effectively over. The towers are standing, the spectrum is deployed, and the network is live. T-Mobile has moved into what analysts call harvest mode — reaping the financial rewards of past investments without needing massive new infrastructure spending.

The numbers illustrate the shift. In third-quarter 2025 results, T-Mobile reported a 6% increase in core adjusted EBITDA, a key measure of operating profitability.

More importantly, management raised full-year 2025 adjusted free cash flow guidance to $17.8 billion–$18.0 billion. With infrastructure spending stabilizing around $10 billion annually, a greater share of incremental revenue flows to the bottom line. While many AI companies are burning cash to build data centers, T-Mobile is generating excess cash from a finished product.

Engineering Value: The $14 Billion Return Plan

Generating cash is just the first step. The real value for investors is how T-Mobile uses that cash. Rather than hoarding funds for acquisitions, T-Mobile is returning capital to shareholders. The company has authorized a $14 billion shareholder return program that runs through the end of 2026. Since late 2022, the company has returned a cumulative $41.8 billion to stockholders.

The primary engine of that return is share buybacks. In third-quarter 2025, T-Mobile repurchased roughly 10.2 million shares. Buybacks reduce shares outstanding, which boosts earnings per share even if net income is flat. A steady buyer like T-Mobile can also create a natural price floor, dampening volatility during market sell-offs.

Alongside buybacks, T-Mobile pays a quarterly cash dividend of $1.02 per share, with the next payout scheduled for March 12, 2026. A 2.06% yield may look modest next to some Treasury yields, but T-Mobile offers growth that bonds do not. The company recently increased its dividend by 16%. In an inflationary environment, a growing dividend preserves purchasing power better than a fixed bond payment, making T-Mobile a bond proxy with upside.

Capital Markets Day: The Next Trigger

Savvy investors appear to be positioning for a move higher. Market data from late January and early February 2026 shows an unusual surge in T-Mobile call option volume. Call options are bets that a stock will rise; when volume spikes without a clear headline, it often signals that smart money expects a positive catalyst.

That catalyst is likely the upcoming Capital Markets Day on Feb. 11, 2026, which coincides with the company’s fourth-quarter earnings report. While earnings recap the past, Capital Markets Day is about the future.

Investors expect CEO Srini Gopalan to unveil updated, potentially aggressive financial targets for 2026 and 2027. Many are betting the buyback king will authorize additional capital returns. If management lays out a credible path to sustained free cash flow growth, it could trigger a meaningful stock re-rating, validating the bullish activity seen in the options market.

Low Churn, High Value: The Loyalty Factor

Safety rarely comes cheap. T-Mobile trades at a price-to-earnings ratio of roughly 19x — a premium to some of its legacy competitors, which often trade at single-digit multiples. Skeptics may view that as expensive, but the premium is backed by superior fundamentals.

T-Mobile’s cost-efficient, harvest strategy has not degraded its product. On Jan. 15, 2026, J.D. Power awarded T-Mobile the highest network quality ranking in five of six U.S. regions. That third-party validation suggests the company’s network advantage is durable.

Equally important, the customer base is incredibly sticky. T-Mobile reported an industry-leading postpaid phone churn rate of just 0.89%. Churn measures the percentage of subscribers who cancel service; a sub-1% number is elite. Predictable revenue streams make future cash flows more reliable, and in a volatile market investors will pay a premium for that certainty.

Four Bars Building a Perfect Storm Shelter

In a jittery market, T-Mobile offers a rare sanctuary: the defensive stability of a utility combined with the shareholder-friendly returns of a mature cash-generating company.

While other sectors wrestle with high interest rates and unproven AI spending, T-Mobile has completed its network build-out and is returning significant cash to shareholders. With a growing dividend, steady buybacks, and a major strategic update arriving next week, T-Mobile lets investors remain in equities while capturing many of the safety characteristics of a bond. For those seeking shelter from the storm, “boring” is shaping up to be one of the more profitable trades on the board.

Thank you for subscribing to The Early Bird, MarketBeat’s 7:00 AM newsletter that covers stories that will impact the stock market each day.

This email message is a sponsored email from Huge Alerts, a third-party advertiser of The Early Bird and MarketBeat.

This message is a paid advertisement for BioStem Technologies Inc. (OTC: BSEM) from Sideways Frequency and Huge Alerts. American Consumer News, LLC dba MarketBeat receives a fixed fee for each subscriber that clicks on a link in this email, totaling up to $12,600. Other than the compensation received for this advertisement sent to subscribers, MarketBeat and its principals are not affiliated with either Sideways Frequency or Huge Alerts. MarketBeat and its principals do not own any of the stocks mentioned in this email or in the article that this email links to. Neither MarketBeat nor its principals are FINRA-registered broker-dealers or investment advisers. The content of this email should not be taken as advice, an endorsement, or a recommendation from MarketBeat to buy or sell any security. MarketBeat has not evaluated the accuracy of any claims made in this advertisement. MarketBeat recommends that investors do their own independent research and consult with a qualified investment professional before buying or selling any security. Investing is inherently risky. Past-performance is not indicative of future results. Please see the disclaimer regarding BioStem Technologies Inc. (OTC: BSEM) on Huge Alerts’ website for additional information about the relationship between Huge Alerts and BioStem Technologies Inc. (OTC: BSEM).

If you need assistance with your account, please don’t hesitate to email our South Dakota based support team at contact@marketbeat.com.

If you no longer wish to receive email from The Early Bird, you can unsubscribe.

Copyright 2006-2026 MarketBeat Media, LLC. All rights protected.

345 North Reid Place, Sixth Floor, Sioux Falls, S.D. 57103. United States..

Daily Bonus Content: Wall Street’s New Sports Prediction Trade (From The Tomorrow Investor)